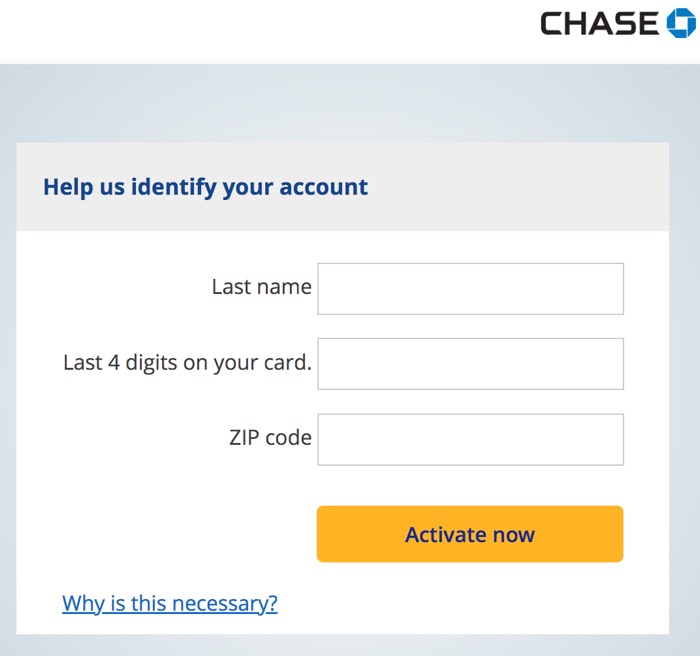

New quarter, new offers. A quick 2024 Q2 reminder that you can discover targeted offers for your Chase-issued credit card at Chase.com/mybonus. This includes both their in-house cards like Sapphire or Freedom Flex and their co-branded cards like United, IHG, Hyatt, Southwest, Amazon, etc. For some reason, these are often offers that they don’t tell you about otherwise by email or snail mail.

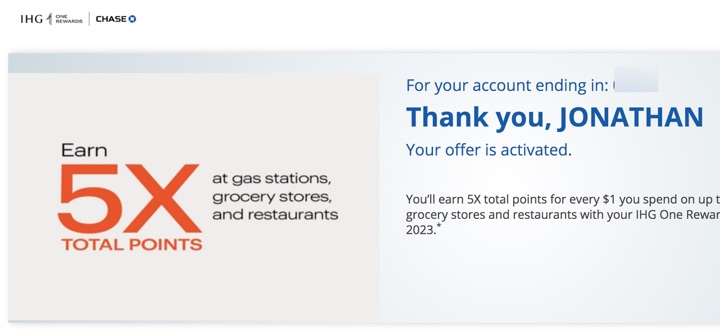

Selected folks are getting 5X points on Gas Stations, Groceries, and Home Improvement Stores:

Many others are being offered a $25/$35 discount on annual subscriptions of MAX (formerly HBO Max) streaming service.

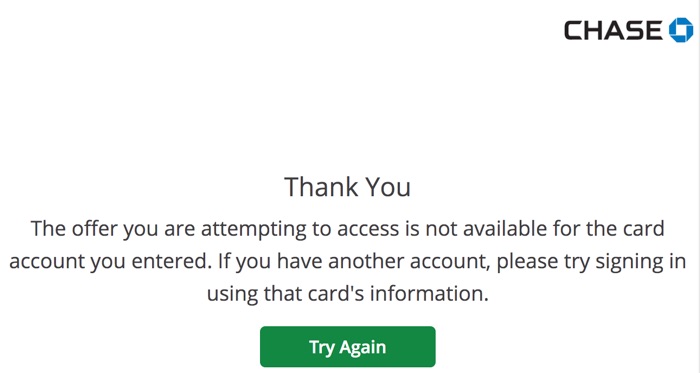

You may also simply get a message that your card can’t be found or that you weren’t targeted:

In some cases, you may be able to stack on top of your existing rewards, for example the current 5% cash back categories of the Chase Freedom and Freedom Flex.

New limited-time offer. The

New limited-time offer. The

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)