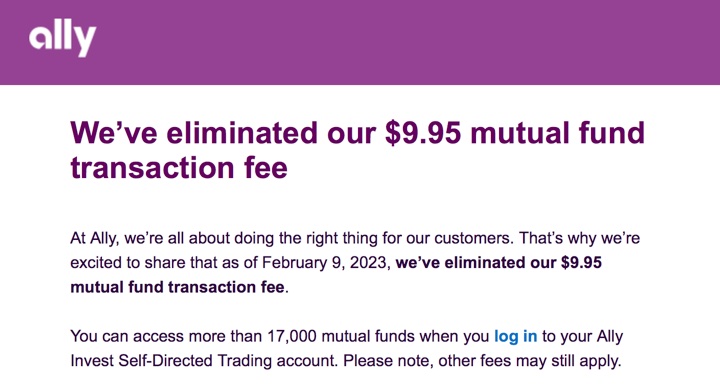

Ally Invest is the self-directed brokerage arm of Ally Financial, and you may have an account from previous TradeKing and/or Zecco mergers. Ally Invest just removed their $9.95 mutual fund transaction fee, including for money market funds:

At Ally, we’re all about doing the right thing for our customers. That’s why we’re excited to share that as of February 9, 2023, we’ve eliminated our $9.95 mutual fund transaction fee.

You can access more than 17,000 mutual funds when you log in to your Ally Invest Self-Directed Trading account. Please note, other fees may still apply.

First of all, the default cash sweep for Ally Invest pays zero interest. In addition, this change may be of interest to customers who also use Ally Bank, given that their online savings account only pays 3.40% APY (as of 2/15/23). Meanwhile, here are the 7-day SEC yields (as of 2/14/23) of top money market funds:

- Vanguard Cash Reserves Federal Money Market Fund Admiral Shares (VMRXX) – 4.51% ($3,000 min)

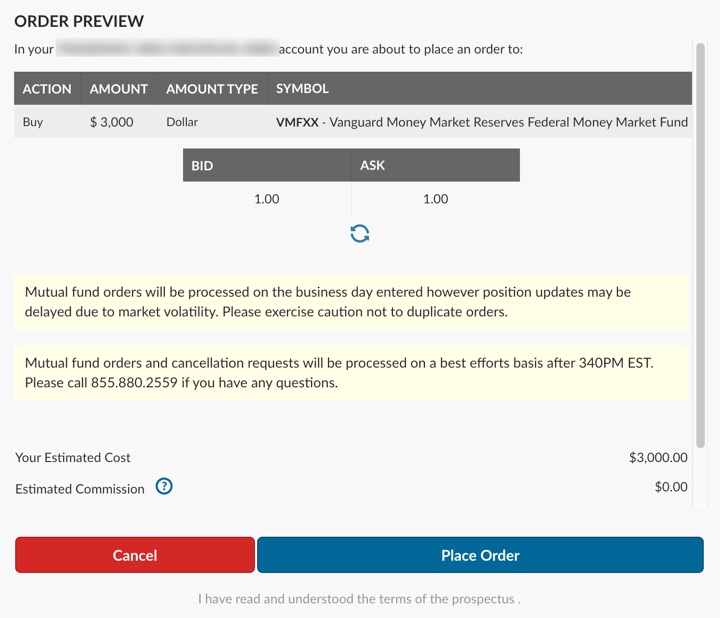

- Vanguard Federal Money Market Fund (VMFXX) – 4.50% ($3,000 min)

- Vanguard Municipal Money Market Fund (VMSXX) – 3.43% ($3,000 min)

- Gabelli U.S. Treasury Money Market Fund (GABXX) – 4.43% ($10,000 min)

- Fidelity Government Money Market Fund (SPAXX) – 4.19% ($100 min*)

* The Fidelity fund does not have a minimum itself, but Ally has a $100 minimum order size for online mutual fund orders.

I have gone into my Ally Invest account and manually tested all of the money market mutual funds listed above, and it let me put in the order at the minimum amounts shown. Ally Invest also does not charge a short-term redemption fee. I was able to make an instant transfer of funds from my Ally Bank deposit accounts to my Ally Invest brokerage account. Therefore, if you have an Ally Bank account and don’t want to look too far elsewhere, you may consider this option to increase the yield on your cash holdings.

Here’s my monthly roundup of the best interest rates on cash as of February 2023, roughly sorted from shortest to longest maturities. We all need some safe assets for cash reserves or portfolio stability, and there are often lesser-known opportunities available to individual investors. Check out my

Here’s my monthly roundup of the best interest rates on cash as of February 2023, roughly sorted from shortest to longest maturities. We all need some safe assets for cash reserves or portfolio stability, and there are often lesser-known opportunities available to individual investors. Check out my

Capital One 360 has a new special

Capital One 360 has a new special  Primis Bank is relatively unknown, but is sure to gather some new deposits with their

Primis Bank is relatively unknown, but is sure to gather some new deposits with their

New customer referral offer. If you don’t have a Marcus account yet, if you open with a

New customer referral offer. If you don’t have a Marcus account yet, if you open with a  Investing app Public just announced a

Investing app Public just announced a  As inflation spiked, so did interest in purchasing inflation-linked

As inflation spiked, so did interest in purchasing inflation-linked  The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)