Update December 2021: Follow-up that I eventually did receive my 90,000 Drop points (see screenshot) but I did have to contact Drop support and send them a screenshot of my account opening e-mail for proof as it didn’t track on its own. Sometime in November 2021, Drop added the restriction “No stacked deals available. Promotion codes found outside of Drop are not eligible for points.” Therefore, stacking is no longer available today, but if you applied through Drop back in September/October 2021 when there was no such restriction, I would encourage you to do the same.

The Drop app itself has also been earning an easy trickle of points via Target and Amazon purchases that I would have made anyway by linking a payment card (plus linking a card gets you 1,000 points a month free), and plan on cashing out again at 100,000 points for $100 in Amazon gift cards.

The Lili referral bonus is still up to $100 and is a more reliable bonus that pays out quickly, with no submission of business docs required. The terms have changed slightly, now requiring a $250 direct deposit instead of a $250 debit card spend. Details below.

Original full review:

Lili is a new banking app that has the core features of popular consumer fintech apps like Chime, but adds features focused on freelancers and independent contractors (sell on Etsy, find projects on Upwork, etc). Highlights:

- Banking. No minimum balance and no monthly fees. Access your direct deposit up to 2 days early. No ATM fees within the 38,000+ ATM MoneyPass network. Free debit card.

- Free freelancer features. App helps you easily mark business expenses, find tax deductions, set aside tax withholding. Deposit cash at 90,000 retail locations including Walmart, CVS, Walgreens, and 7-11.

- Paid freelancer features with Lily Pro at $5/month. This premium paid tier includes $200 in fee-free overdrafts, 1% APY interest on savings, cashback rewards on the debit card, and the ability to create and send unlimited invoices.

- $100 referral bonus for new users. Details below.

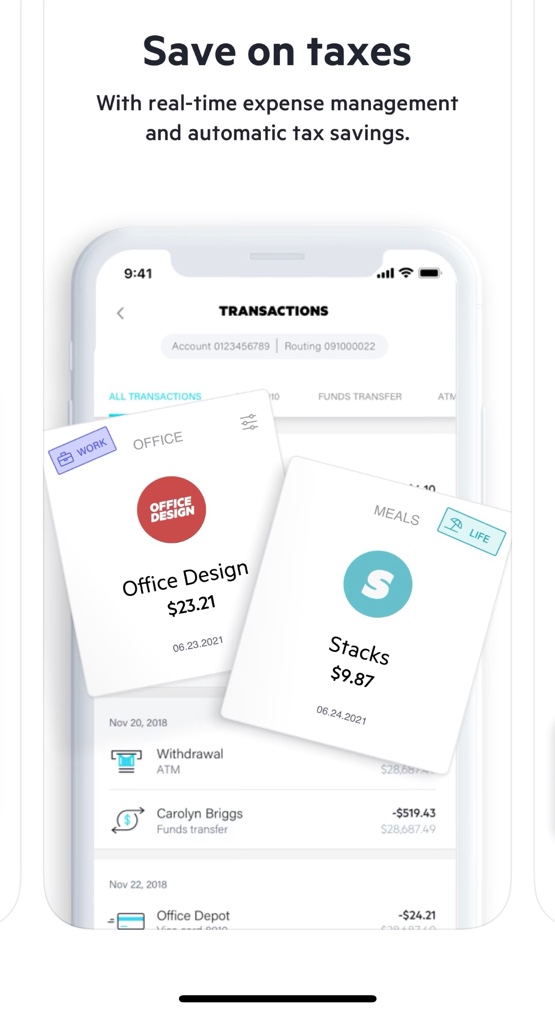

My experience. Thankfully, this account doesn’t hassle you for a bunch of uploaded business verification documents, as it is focused on freelancers. After opening an account, my tip is to double-check your SSN on the application before submitting. If you mistype it, they won’t give you a chance to try again and you’ll have to reach them by phone to correct the situation, which wastes a lot of time. Otherwise, it would have been quite fast. This app does offer special appeal to solo-entrepreneurs (I prefer that term to “side-hustlers”) looking for some help marking business expenses and tracking them to minimize taxes.

After you make a purchase on the debit card, the app will almost instantly ask you if it is a work or “life” expense. You can easily attach a photo receipt if it is a work expense for your records. Incoming deposits can be marked so that you put aside some money for taxes.

I was also interested in the 1% APY savings account, but it requires the Lily Pro subscription at $5 a month. If you maintain high cash balances, this still might be a good trade-off since most other online banks are only at 0.50% APY or so currently. In addition, invoice software can cost $5 a month on its own, so if you can use both features, this can be a good combo.

$100 referral bonus details. If you open a Lili account through a Lili referral link, use JenPing as the referral code, and receive a single qualifying direct deposit of at least $250 within the first 45 days, you will receive a $100 bonus.

As noted in my Turning Small Deals into a $100,000 Nest Egg post, you can motivate yourself by treating these bonuses as a way to max out your annual IRA contribution. $6,000 annual limit = $500 per month = $125 per week. With this bonus, I am now over the $5,000 mark in the MMB Free IRA Contribution 2021 Challenge.

Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.

Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.

Blockfi credit card. The new

Blockfi credit card. The new

Hanscom Federal Credit Union (HFCU) has hiked back up the rate on their

Hanscom Federal Credit Union (HFCU) has hiked back up the rate on their

The

The

Porte is another banking fintech app, this time with the notable feature of 3.00% APY on up to $15,000 on their attached high-yield savings account. To enable access to this account, you must have a one-time occurrence of $1,000+ of direct deposits within one month. There doesn’t appear to be any ongoing requirements after that.* This makes it a more simple setup than the 3% APY accounts of

Porte is another banking fintech app, this time with the notable feature of 3.00% APY on up to $15,000 on their attached high-yield savings account. To enable access to this account, you must have a one-time occurrence of $1,000+ of direct deposits within one month. There doesn’t appear to be any ongoing requirements after that.* This makes it a more simple setup than the 3% APY accounts of

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)