Thanks to the discovery of free eBook rentals at the library, I finally read Blink: The Power of Thinking Without Thinking by Malcolm Gladwell over the weekend. It’s a short book and an easy read, which probably helped create its great popularity.

Thanks to the discovery of free eBook rentals at the library, I finally read Blink: The Power of Thinking Without Thinking by Malcolm Gladwell over the weekend. It’s a short book and an easy read, which probably helped create its great popularity.

The book is primarily about the power of your “adaptive unconscious” to make quick and often-accurate decisions. By doing what Gladwell terms “thin-slicing”, the mind extracts the pertinent information out of a ton of available data. An expert on antiques spotting a fake within seconds, a researcher who has seen hundreds of couples being able to predict divorce, a veteran military commander winning a war game against a sophisticated algorithm overwhelmed with data, or someone who has studied facial expressions for years being able to spot hidden emotions. While interesting, I viewed much of this as an expected result of experts being experts.

However, in the end it also exposes how the unconscious can make bad decisions, full of prejudices and tendencies that you aren’t even aware of. Even if you think you are making decisions completely objectively, unless you truly strip out all the other variables then you can’t be sure. Although there is little mention of personal finance topics here, I would say this cautious side is where the book applies to money.

Other books like Your Money and Your Brain and Predictably Irrational have shown that a lot of our instinctual and/or unconscious tendencies towards money actually hurt us financially. We repeatedly find ourselves in speculative bubbles, our mind does quick relative calculations when it shouldn’t and we get used to a better lifestyle too quickly. Being aware of these hidden tendencies can help us become more successful.

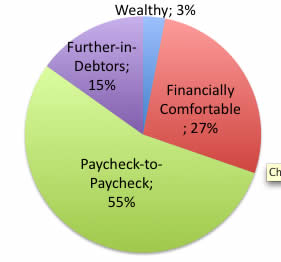

I ran across

I ran across  You may be familiar with

You may be familiar with

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work){kind=link}