Whenever I feel overwhelmed by the amount of noise coming at me through my computer screens, I read a book. When the new books on my desk don’t impress, I find an old book. That is how I came to buy a used, first edition of Bogle on Mutual Funds last year from Amazon for a penny + $3.99 shipping. John Bogle is best known as the founder of Vanguard who brought index funds to retail investors and changed the entire industry. Since most people just know him as the Index Fund Guy, I feel that he is under constant pressure to stay “on message” and only promote buy-and-hold passive investing.

But you know what? Even though many would prefer the world to be black and white, it isn’t. For a very long time, Bogle also ran and owned low-cost actively-managed funds like the Vanguard Wellington and Wellesley funds. To this day, a big chunk of Vanguard assets are actively-managed. Even recently, he has expressed skepticism about the trend towards holding more non-US international stocks.

When you read the circa-1993 material in Bogle on Mutual Funds, I feel like you get more of the “grey” Bogle. There is advice on how to pick a good stock mutual fund, even amongst actively-managed funds. There are some practical considerations for picking amongst asset classes. Of course, the main takeaways are still there:

- Index funds are a great invention for long-term investors.

- Low costs are very, very important.

- Low portfolio turnover and minimizing taxes are very important.

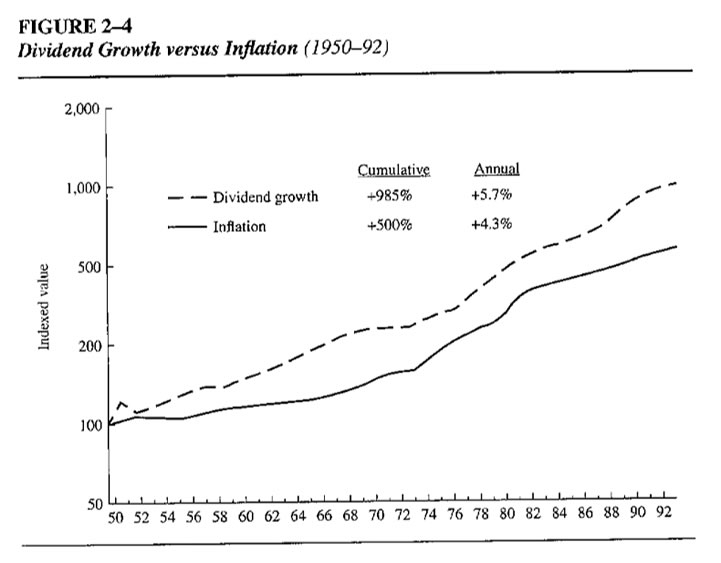

But the book also includes a lot of little nuggets like comparing dividend yield relative to interest rates. First, here is a chart from the book showing how S&P 500 dividends have grown steadily with inflation. Meanwhile, the yield from a bond may start out higher, but would remain be constant until maturity.

Unfortunately, defining what constitutes too high a price for dividends is a fallible exercise, one that must take into account not only the average historical valuations for stocks but the current valuations for other investment alternatives as well. History suggests that stocks are relatively expensive when the price paid for $1 of dividends is above $30 (i.e., a yield of 3.3%) and relatively cheap when the price paid is less than $20 (a yield of 5%). However, stocks may well be attractive at a yield of, say, 3.5% if there are compelling reasons to assume that their dividends will increase rapidly or if yields on other classes of financial assets are relatively unattractive.

In the example shown in Figure 2-5, buying a portfolio of stocks at a 3% yield rather than a bond at a 7% yield might not be a sensible investment, especially considering the incremental risk incurred in holding stocks. When stocks yield 4.5% and bonds yield 6%, that may be quite another story.

As of mid-2015, the S&P 500 dividend yield is ~2% and 30-year Treasury bonds are ~3%. The relative difference between the stock yield and the bond yield only 1%, even less than the 1.5% gap that he calls “quite another story”. This would suggest that (long-term) the S&P 500 is expensive historically, but still attractive relatively when compared to bonds at this point.

Anyhow, I bring this up is because Bogle on Mutual funds has just been republished as part of the “Wiley Investment Classics” series. (#TBT = Throwback Thursday.) It’s a great book and you could buy it to have it in Kindle format or to support Bogle, but you can also buy a used, 1st edition hardcover for $4 shipped. (Or borrow it from a library, but this is going in my permanent collection.) Unfortunately it is not a “revised” edition where the charts are updated or there is new investment commentary based on current market conditions. The only difference that I could find between my 1993 version and my 2015 review copy is a new 17-page introduction which mostly talks about the history of the book itself.

If you’re going to buy something new, I’d recommend their other Bogle classic – John Bogle on Investing: The First 50 Years – which is a compilation of his best speeches over the years going back all the way to his 1951 undergraduate senior thesis. I haven’t read that one yet, but I really enjoyed a similar compilation of Charlie Munger speeches.

Another thing I’ve been getting into this summer is grilling over 100% natural hardwood charcoal. My gateway drug was Alton Brown’s

Another thing I’ve been getting into this summer is grilling over 100% natural hardwood charcoal. My gateway drug was Alton Brown’s

I believe that entrepreneurialism is, like many things, a combination of talent and learned skill. Some people will take to it naturally, but a great many more can become successful and independent business people with the proper inspiration and guidance. I plan to help and encourage my daughters to set up their own micro-businesses once they are teenagers, whether it is coding apps or starting a booth at the farmer’s market. Some things you can’t learn from a book.

I believe that entrepreneurialism is, like many things, a combination of talent and learned skill. Some people will take to it naturally, but a great many more can become successful and independent business people with the proper inspiration and guidance. I plan to help and encourage my daughters to set up their own micro-businesses once they are teenagers, whether it is coding apps or starting a booth at the farmer’s market. Some things you can’t learn from a book.  While

While  Wouldn’t a Netflix for books be neat? You could borrow all the books that you wanted to read and then return them when you’re done. Oh wait, they already invented it and called it a library.

Wouldn’t a Netflix for books be neat? You could borrow all the books that you wanted to read and then return them when you’re done. Oh wait, they already invented it and called it a library. The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)