After rediscovering the young adult versions of fitting personal finance advice on an index card, I decided to go back and read the book The Index Card: Why Personal Finance Doesn’t Have to Be Complicated by Helaine Olen and Harold Pollack. (I was able to find it via library eBook.)

I noticed that the book version of the “index card” was slightly different. The original card had 9 items, but two of them were merged away into each other (401k/IRAs) and (Pay Attention to Fees/Buy Index Funds). I bolded the new additions below. (You can see all chapters on the Amazon page.)

- Strive to Save 10 to 20 Percent of Your Income

- Pay Your Credit Card Balance in Full Every Month

- Max Out Your 401(k) and Other Tax-Advantaged Savings Accounts

- Never Buy or Sell Individual Stocks

- Buy Inexpensive, Well-Diversified Indexed Mutual Funds and ETFs

- Make Your Financial Advisor Commit To a Fiduciary Standard

- Buy a Home When You Are Financially Ready

- Insurance – Make Sure You’re Protected

- Do What You Can To Support the Social Safety Net

- Remember The Index Card

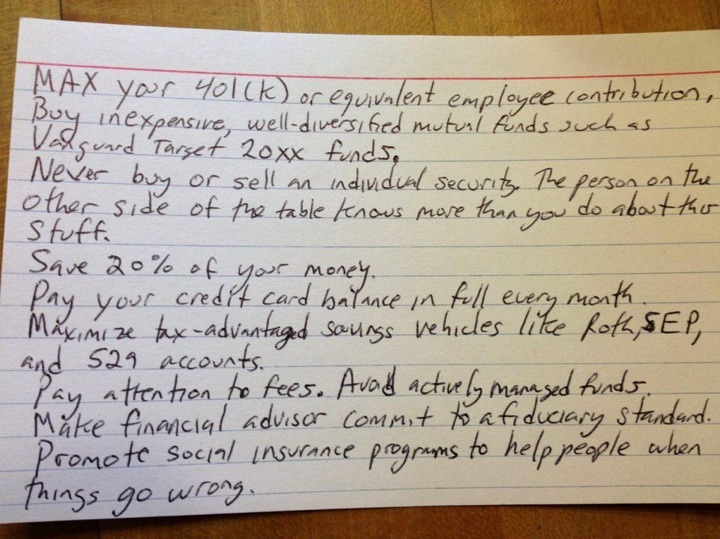

Here again is the original:

Here are my notes on the newly-addressed topics of home-buying and insurance.

Home-buying. This will always be a hard topic because it mixes in emotion, personal history, peer pressure, and all that fuzzy stuff. If you want to own a home, you need to make sure the purchase won’t blow up your overall financial picture. Nothing really surprising, but still good advice.

- Get your debt under control first.

- Save up as close to a 20% down payment as you can.

- Stick with a 15 or 30 year fixed-rate mortgage.

- Prioritize what you really want and need in a home. Stay within your budget.

- Location, location, location.

Insurance. There are low-probability events that can destroy decades of hard work, and that’s why humans invented insurance to spread the risk. Here are their cut-to-the-chase bullet points:

- Emergency fund – Maintain one!

- Life insurance – If you’re young(ish), just buy 30-year level term insurance.

- Property insurance – Raise your deductible as high as you can handle.

- Health insurance – Always sure you stay in-network.

- Liability insurance – Coverage for at least twice your net worth.

I’m glad that this book still retained its “quick-and-dirty” nature. No single rule will cover every scenario, but it’s good to have a clear and concise collection of the big points along with just enough explanation that you understand the basic reasoning behind it.

The

The

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)