One common recommendation for new parents is to save time wherever you can. So tonight, for the very first time, I have signed up for the AutoPay feature for my most heavily-used American Express card to have it pay the credit card bill in full each month by withdrawing money from my bank account automatically. I don’t have to do anything.

One common recommendation for new parents is to save time wherever you can. So tonight, for the very first time, I have signed up for the AutoPay feature for my most heavily-used American Express card to have it pay the credit card bill in full each month by withdrawing money from my bank account automatically. I don’t have to do anything.

Usually, I don’t like giving any vendors the right to suck money (“pull”) from my checking account. It feel invasive, somehow. I prefer to use my bank’s online BillPay feature to send (“push”) money after I get my paper bill and verify all the charges are legit. I also like to see my electric bill to monitor our power usage, and the water bill to make sure there aren’t any leaks, etc.

However, with a newborn I can potentially imagine forgetting to pay a bill, so maybe automation is a good idea. I have never had any problem disputing a wrong charge with AmEx, and I have an checking to savings overdraft buffer at Ally Bank so I won’t be dinged with overdraft fees. If it works out, after looking around it appears that almost every bill that I have can be set to AutoPay. What you do think?

One of my overall goals for 2012 is to make this site more of a permanent resource for information. As part of this, I want to create an “Expense Reduction Guide” that will provide an organized way to find ways to maximize personal value and make your spending efficient.

One of my overall goals for 2012 is to make this site more of a permanent resource for information. As part of this, I want to create an “Expense Reduction Guide” that will provide an organized way to find ways to maximize personal value and make your spending efficient. Last month, I

Last month, I

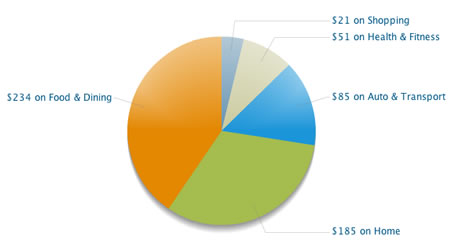

Next, you should sign up for the online aggregator tool Mint.com. I also like versions of Yodlee, but it looks like their development has slowed significantly. To start, all you need is your e-mail address and the login details for your credit card website.

Next, you should sign up for the online aggregator tool Mint.com. I also like versions of Yodlee, but it looks like their development has slowed significantly. To start, all you need is your e-mail address and the login details for your credit card website.

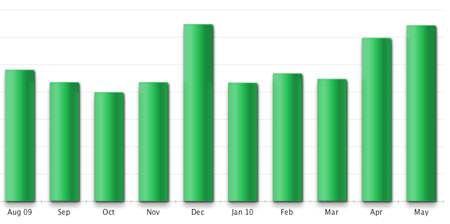

You may be familiar with

You may be familiar with

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)