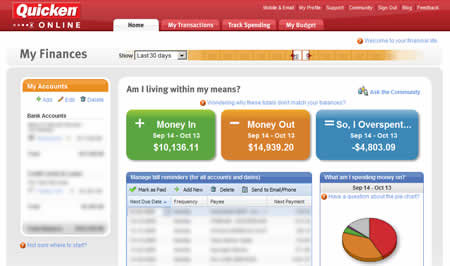

Quicken Online is now free. It used to cost $3 per month ($36/year). This established brand name is now directly competing with other free online account aggregation services like Mint, Geezeo, Wesabe, and Yodlee MoneyCenter. I guess they decided it would be better to give this product away for free as well, in the hopes that they can sell you TurboTax or the desktop Quicken later on. 😉 I signed up; here is a screenshot:

Quicken Online is now free. It used to cost $3 per month ($36/year). This established brand name is now directly competing with other free online account aggregation services like Mint, Geezeo, Wesabe, and Yodlee MoneyCenter. I guess they decided it would be better to give this product away for free as well, in the hopes that they can sell you TurboTax or the desktop Quicken later on. 😉 I signed up; here is a screenshot:

Although I keep meaning to do a more in-depth review of all these services, I have not done so yet because after trying each of these services briefly I always end up going back to my trusted Yodlee MoneyCenter. I have been disappointed in how they all (including Yodlee) unsuccessfully attempt to categorize my purchases, and I am unwilling to keep manually correcting them.

I prefer the simple “snapshot” feel of Yodlee, where I can see all my balances and investments at a glance, along with recent transactions. I can even keep track of my frequent flier miles and other rewards points. Each day I log in, acknowledge any changes, and am done within 5 minutes. “Get in, get out, get on with your life”.

Other more personal (and lame) reasons include sheer habit, as I have been using Yodlee since 2004. Finally, I have a lot of accounts, and the idea of having to re-enter all those passwords again is not appealing at all.

All of these sites take your logins and passwords, and essentially pretend to be you and scrape the pertinent information off each webpage using a script. Yodlee actually sells its account aggregation services to Mint. Geezeo uses CashEdge. Quicken Online and Wesabe have their own systems. Be aware that in many cases you are giving them limited power of attorney to do this. It’s all in the terms and conditions! Many people wisely are very skeptical of handing over all their passwords to a third party. I have previously posted a modest defense of my use of Yodlee here.

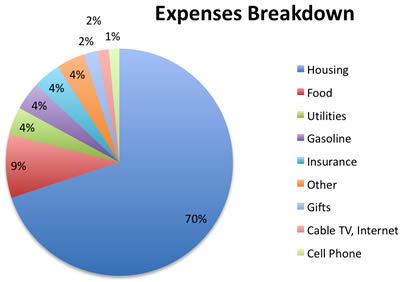

You may be expecting a review of the new online service

You may be expecting a review of the new online service  Last month one of our credit card statements spanned two pages because we had eaten out so often. Not only is it more expensive, I’m pretty sure it’s less healthy. So now we’re trying to limit ourselves to 2-3 times a week (minus the cafeteria at work), and making one of our outings to a new restaurant that we haven’t tried before.

Last month one of our credit card statements spanned two pages because we had eaten out so often. Not only is it more expensive, I’m pretty sure it’s less healthy. So now we’re trying to limit ourselves to 2-3 times a week (minus the cafeteria at work), and making one of our outings to a new restaurant that we haven’t tried before.  One possible solution to relieve such stress that we are currently trying out is the Adult Allowance, where each person is given a certain amount of money that they can spend with no questions asked. I’ve seen it in a few places, including Him and Her over at Make Love Not Debt. No rolling your eyes, no passive-aggressive sighs, no exasperated “Why would anyone buy that?”. Actually, one annoying question from me is “Why didn’t you let me spend 10 minutes researching the best deal for your XXX purchase?” The idea of paying more than needed may cause me physical pain, but why should I let that ruin her purchase?

One possible solution to relieve such stress that we are currently trying out is the Adult Allowance, where each person is given a certain amount of money that they can spend with no questions asked. I’ve seen it in a few places, including Him and Her over at Make Love Not Debt. No rolling your eyes, no passive-aggressive sighs, no exasperated “Why would anyone buy that?”. Actually, one annoying question from me is “Why didn’t you let me spend 10 minutes researching the best deal for your XXX purchase?” The idea of paying more than needed may cause me physical pain, but why should I let that ruin her purchase?

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)