College savings plans tend to have promotions mostly on May 29th, aka “529 Day”, but some are also offering bonuses during this Black Friday/Cyber Week/Year-End Holiday period. Now is also a good time to remember 529 plans can accept outside contributions, which mean you can easily contribute directly to someone else’s 529 plan, or request that people consider gifts that go directly to your child’s 529 plan. Most have easy links to share with friends and family.

Here’s a list of what I could find, please let me know if you find more. I’m listing the state, but you do not have to be a resident of that state to open a 529 account there. You can have multiple 529s from different states, and often you can get the bonus once for each child. However, you may need to be a resident to qualify for a specific bonus, or there may be an age restriction on the beneficiary, etc.

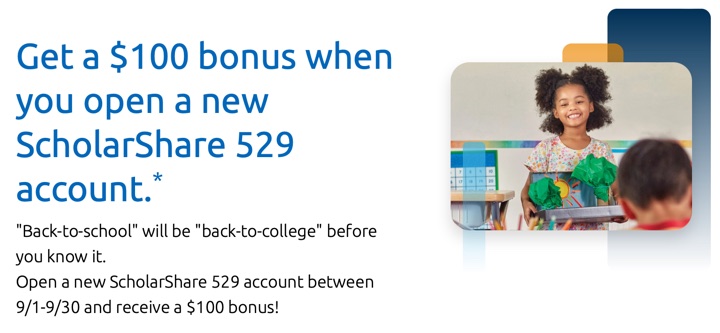

- California – CA Scholarshare 529 Bonus: $50 Target gift card. Ends 12/13.

- Florida – Florida Prepaid 529 Bonus: $100 Amazon gift card. Ends 12/9.

- Oklahoma – Oklahoma 529 Bonus: $50/$100. Ends 12/13.

- Pennsylvania – PA 529 Bonus: $100 Guaranteed Match. Ends 12/31. Note: All PA children born after January 1, 2019, have a $100 investment available for them in a Keystone Scholars account. You must activate to claim.

- Wisconsin – Edvest 529 Bonus: $100. Ends 12/13.

529 plans can now pay for K-12 tuition and other educational expenses beyond college tuition and room/board. Check your own state rules, though. Finally, opening a plan and making any contribution also starts the 15-year clock on potential future 529-to-Roth IRA rollovers.

Photo is modified from Pawel Czerwinski on Unsplash

Updated for 2023. 5/29 is “National 529 College Savings Plan Day” and every year a few state plan offer promotions and/or giveaways. Most offers end by May 31st. Some offers require in-state residency, but some don’t. 529 plans can now also pay for K-12 tuition and other educational expenses beyond college tuition and room/board.

Updated for 2023. 5/29 is “National 529 College Savings Plan Day” and every year a few state plan offer promotions and/or giveaways. Most offers end by May 31st. Some offers require in-state residency, but some don’t. 529 plans can now also pay for K-12 tuition and other educational expenses beyond college tuition and room/board.  One of the concerns about contributing to 529 plan for college savings is that you won’t end up using all the money and end up being hit with additional taxes (at ordinary income rates) and penalties on an non-qualified withdrawal. The funds potentially would have been better off simply invested in a taxable brokerage account (and long-term capital gains rates).

One of the concerns about contributing to 529 plan for college savings is that you won’t end up using all the money and end up being hit with additional taxes (at ordinary income rates) and penalties on an non-qualified withdrawal. The funds potentially would have been better off simply invested in a taxable brokerage account (and long-term capital gains rates).

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)