Thinking about 529 plans and like playing around with interactive calculators? This Vanguard tool helps you visualize how much you’ll need to save for college and how changing up a specific factor would affect your results. It adjusts for age, contributions, investment returns, tuition inflation, and even looks up the current cost of your favorite university. A formal report is spit out with lots of charts, just like a financial advisor might create for you. Here’s a sample screenshot:

Thinking about 529 plans and like playing around with interactive calculators? This Vanguard tool helps you visualize how much you’ll need to save for college and how changing up a specific factor would affect your results. It adjusts for age, contributions, investment returns, tuition inflation, and even looks up the current cost of your favorite university. A formal report is spit out with lots of charts, just like a financial advisor might create for you. Here’s a sample screenshot:

Tuition inflation is something that I think is hard to predict. However, I couldn’t think of anything better than accepting the default assumptions that investment return will only barely outpace tuition inflation.

If you’d rather have a quick, simple scenario, check out this Vanguard article on the power of automatic savings. If you put away $130 a month automatically every month for 18 years, at a 6% return you’d end up with $50,000. Putting away $50 a month reliably would get you to $20,000.

Nearly half of your final amount would be due to investment growth, which thanks to the 529 plan can be tax-free when used towards qualified educational expenses.

I’m still in the camp that retirement should be prioritized over college savings, but I definitely understand the parental instinct to provide the best educational opportunity possible. I’m still pondering the idea of targeting funding college with 1/3rd savings, 1/3rd spending from current income, and 1/3rd grants/scholarships/loans.

Finally, here is another set of handy Vanguard tools, a 529 Plan Interactive Comparison Map and Tax Deduction Calculator.

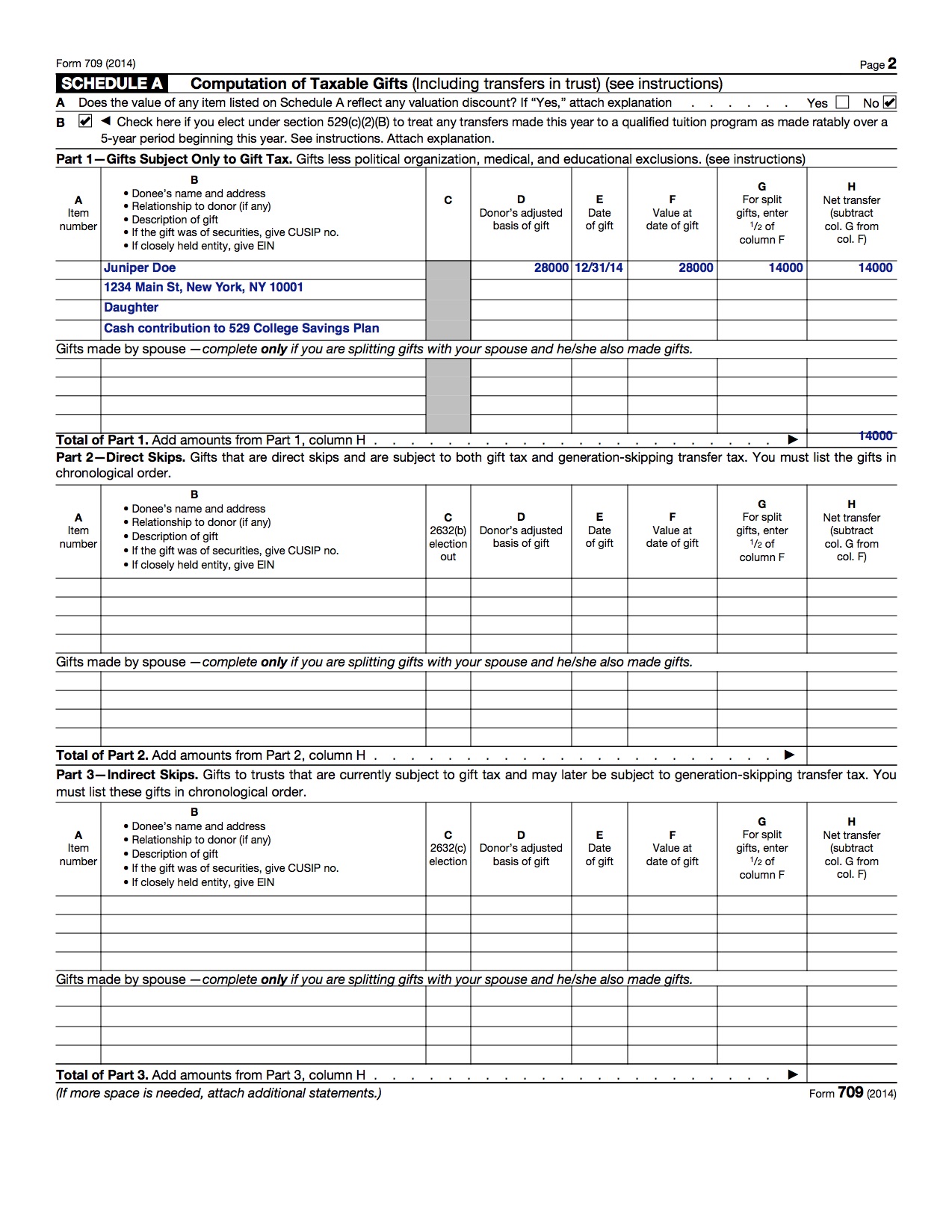

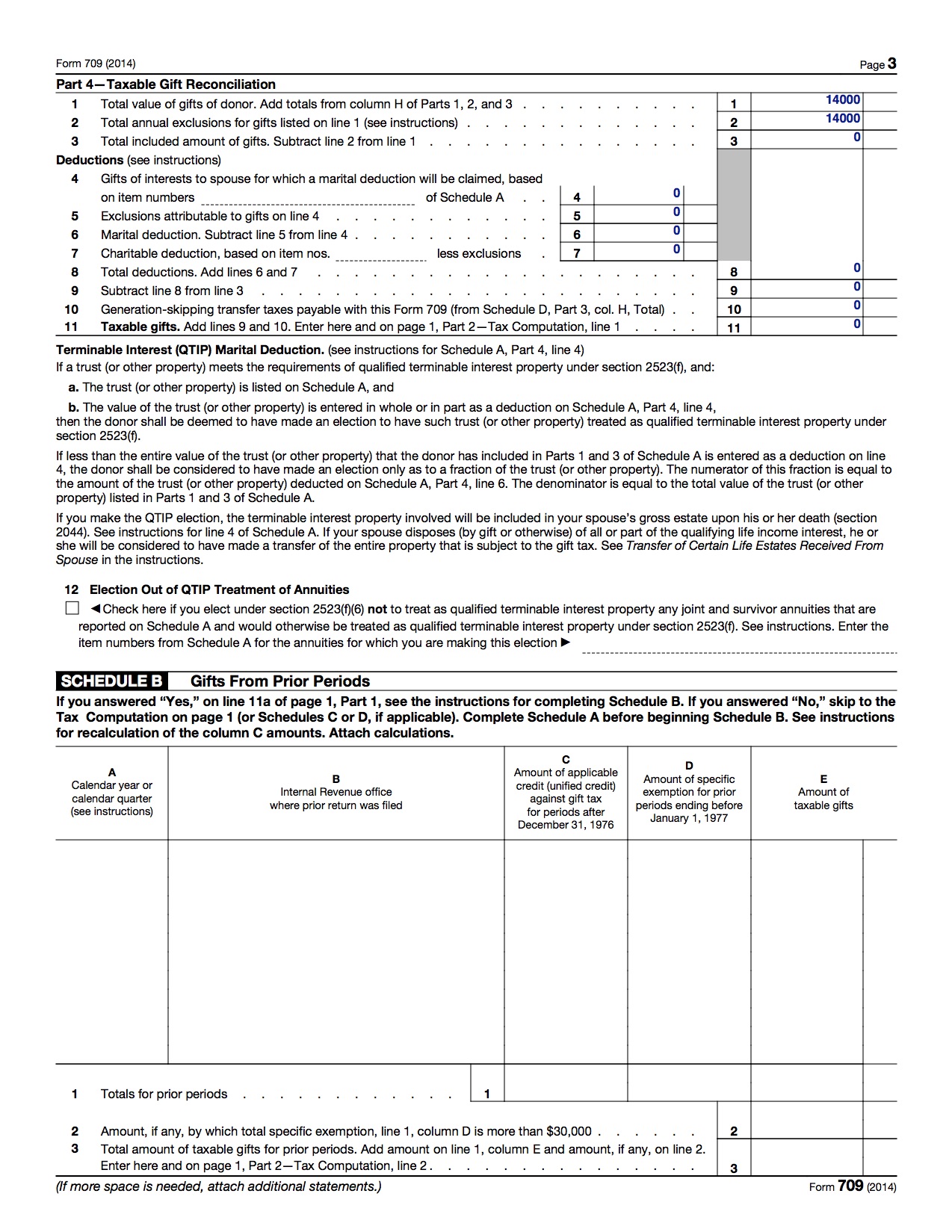

Updated. Let’s say you are fortunate enough to be able to make a large contribution to a 529 college savings plan, perhaps for your children or grandchildren. You read from multiple sources that you are able to contribute up to $75,000 at once for a single person or up to $150,000 as a married couple (2018), all without triggering any gift taxes or affecting your lifetime gift tax exemptions. (From 2013-2017, these numbers were $70k/$140k). What you are doing is “superfunding” or “front-loading” with 5 years of contributions, with no further contributions the next four years.

Updated. Let’s say you are fortunate enough to be able to make a large contribution to a 529 college savings plan, perhaps for your children or grandchildren. You read from multiple sources that you are able to contribute up to $75,000 at once for a single person or up to $150,000 as a married couple (2018), all without triggering any gift taxes or affecting your lifetime gift tax exemptions. (From 2013-2017, these numbers were $70k/$140k). What you are doing is “superfunding” or “front-loading” with 5 years of contributions, with no further contributions the next four years.

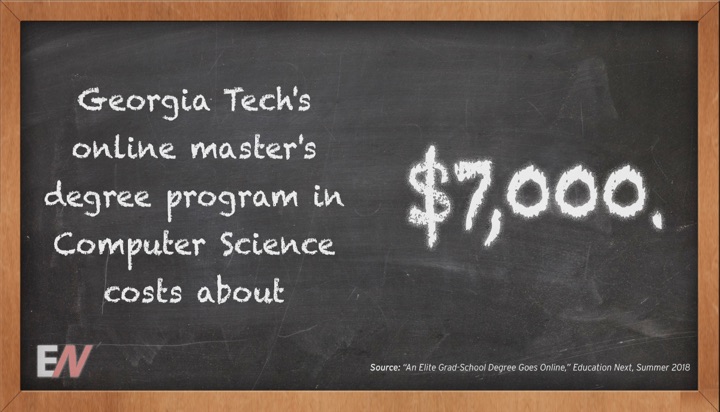

If you are interested in online college education, definitely read

If you are interested in online college education, definitely read

A lot of financial articles are all about optimizing or finding the “best”. The best bank account, best credit card, best mutual fund, etc. However, this CurrentAffairs.org article

A lot of financial articles are all about optimizing or finding the “best”. The best bank account, best credit card, best mutual fund, etc. However, this CurrentAffairs.org article

Investment research firm Morningstar has released their annual 529 College Savings Plans Research Paper and Industry Survey. While the full survey appears restricted to paid premium members, they did release their top-rated plans for 2017. This is still useful as while there are currently over 60 different 529 plan options nationwide, the majority are mediocre and can quickly be dismissed.

Investment research firm Morningstar has released their annual 529 College Savings Plans Research Paper and Industry Survey. While the full survey appears restricted to paid premium members, they did release their top-rated plans for 2017. This is still useful as while there are currently over 60 different 529 plan options nationwide, the majority are mediocre and can quickly be dismissed. The

The  The American Enterprise Institute used newly-released

The American Enterprise Institute used newly-released

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)