If you don’t understand why having a fiduciary requirement matters in terms of financial advice, read this Bloomberg article about student-loan servicer Navient. Learn about the sad behavior of a company that services the student loans of over 12 million people.

If you don’t understand why having a fiduciary requirement matters in terms of financial advice, read this Bloomberg article about student-loan servicer Navient. Learn about the sad behavior of a company that services the student loans of over 12 million people.

Here’s what Navient CEO Jack Remondi says in public:

At Navient, our priority is to help each of our 12 million customers successfully manage their loans in a way that works for their individual circumstances.

Helping our customers navigate the path to financial success is everything we stand for.

Here’s what Navient supposedly did:

In January, the CFPB sued Navient in a Pennsylvania federal court, alleging the company “systematically” cheated student debtors by taking shortcuts to minimize its own costs. Navient illegally steered struggling borrowers facing long-term hardship into payment plans that temporarily postponed bills, the government alleged, rather than helping them enroll in plans that cap payments relative to their earnings.

Why? Because Navient makes more money when you apply for temporary forberance as opposed to income-based repayment.

In July 2013, when Navient was the servicing arm of Sallie Mae, Remondi said in an earnings call that “it’s very expensive work, for example, to enroll a borrower into something like an income-based repayment program … which we are doing. But we don’t actually get paid for outperformance in that side of the equation.”

How much more did borrowers pay? From the CFPB press release:

From January 2010 to March 2015, the company added up to $4 billion in interest charges to the principal balances of borrowers who were enrolled in multiple, consecutive forbearances. The Bureau believes that a large portion of these charges could have been avoided had Navient followed the law.

Here’s Navient’s quiet response in court:

Instead of “No, we didn’t do that horrible thing!”, it was “So? Why would you expect otherwise?”

Borrowers can’t reasonably rely on America’s largest student loan servicer to counsel them about their many options, Navient said on March 24 in a motion to dismiss the case, because its primary role is, after all, to collect their payments.

“There is no expectation that the servicer will act in the interest of the consumer,” Navient said in response to the litigation filed Jan. 18 by the U.S. Consumer Financial Protection Bureau.

Navient does not have a fiduciary duty to the borrower. As a result, even if Navient says they will act in your interest, they don’t have to actually act in your interest. This is an important lesson.

If you have student loan debt, don’t trust your servicer. Apparently, their advice is (allowed to be?) heavily biased. Do your own research on student loan repayment options. There are many options that cap your payments based on income and some even include debt forgiveness options.

In terms of the bigger picture, don’t blindly trust anything in the financial industry. If they want your money and they aren’t a fiduciary then they have no legal requirement to act in your best interest. They can sell you horrible things and it is perfectly legal. If I was ever to let anyone else manage my hard-earned money, it would have to be in a fiduciary relationship. That’s just a minimum to even be considered.

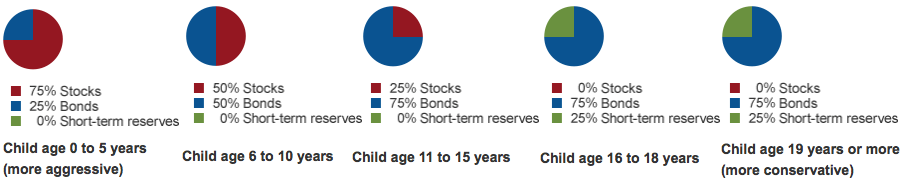

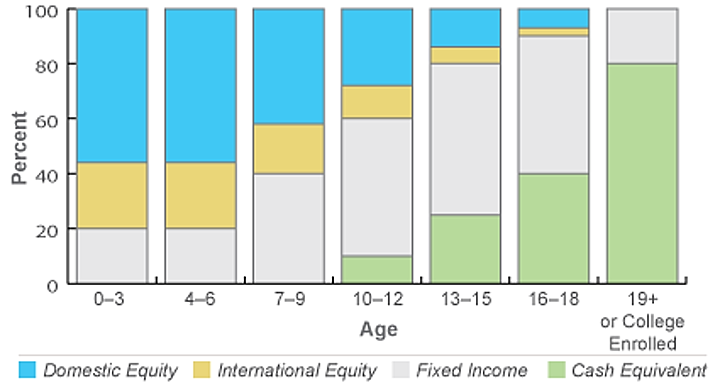

Investment research firm Morningstar has released their annual 529 College Savings Plans Research Paper and Industry Survey. While the full survey appears restricted to paid premium members, they did release their

Investment research firm Morningstar has released their annual 529 College Savings Plans Research Paper and Industry Survey. While the full survey appears restricted to paid premium members, they did release their  I’m always fascinated by the potential power of cheap, accessible education. Back in 2013, I wrote about how Georgia Tech planned to offer an

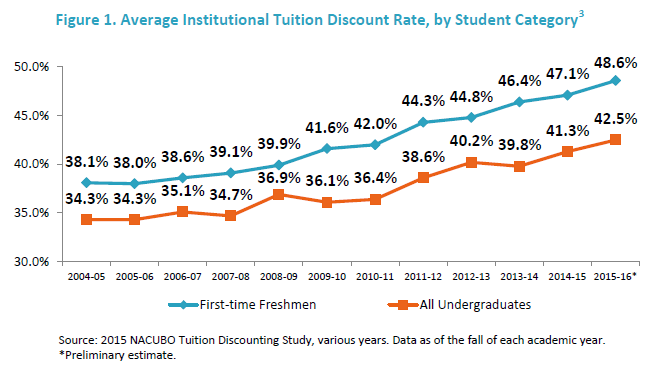

I’m always fascinated by the potential power of cheap, accessible education. Back in 2013, I wrote about how Georgia Tech planned to offer an  The National Association of College and University Business Officers (NACUBO) recently released their 2015 Tuition Discounting Study. While the average quoted “sticker price” tuition went up again as expected, so did the “tuition discount rate”.

The National Association of College and University Business Officers (NACUBO) recently released their 2015 Tuition Discounting Study. While the average quoted “sticker price” tuition went up again as expected, so did the “tuition discount rate”.

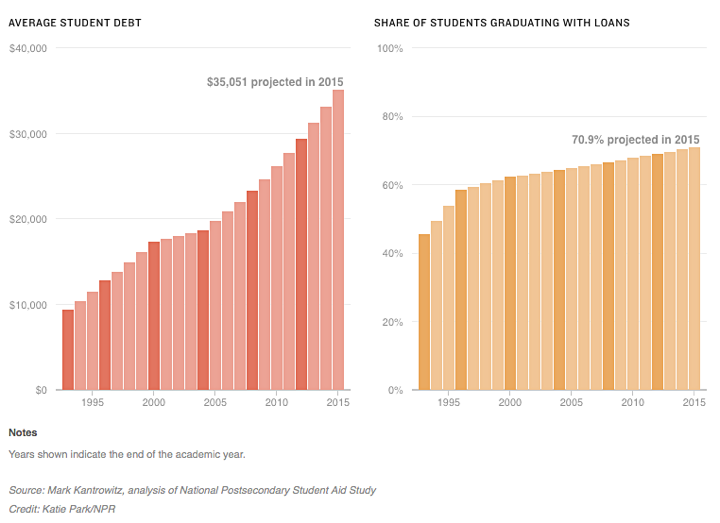

Sometimes I get questions about dealing with student loan debt, but I no longer feel well-qualified to answer. I graduated in 2000 with roughly $30,000 in student loan debt myself, but I never participated in any government-backed repayment plan, nor did I refinance it into a lower interest loan. Roughly 70% of students are graduating with debt today as opposed to 60% in 2000, according to this

Sometimes I get questions about dealing with student loan debt, but I no longer feel well-qualified to answer. I graduated in 2000 with roughly $30,000 in student loan debt myself, but I never participated in any government-backed repayment plan, nor did I refinance it into a lower interest loan. Roughly 70% of students are graduating with debt today as opposed to 60% in 2000, according to this

The government just passed the Protecting Americans from Tax Hikes (PATH) Act of 2015, which had a few notable provisions for 529 college savings plan participants. Some of them need to be taken advantage of quickly.

The government just passed the Protecting Americans from Tax Hikes (PATH) Act of 2015, which had a few notable provisions for 529 college savings plan participants. Some of them need to be taken advantage of quickly.

I’m finally getting around to setting up 529 college savings plans for my kids. It remains my opinion that you should make sure your retirement savings are on track before worrying about college savings. The government let me borrow over $50,000 in student loans for college, but they won’t let me do that again for retirement.

I’m finally getting around to setting up 529 college savings plans for my kids. It remains my opinion that you should make sure your retirement savings are on track before worrying about college savings. The government let me borrow over $50,000 in student loans for college, but they won’t let me do that again for retirement. The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)