![]() Andre Agassi became famous for being a professional tennis player, but his greatest legacy may be through his work in charitable and social causes. He now oversees both a charitable foundation and the Andre Agassi College Preparatory Academy, a tuition-free charter school for at-risk K-12 children. As both a tennis and education enthusiast, I’m a big fan. As part of their “Life’s Work” series, Harvard Business Review interviewed Agassi.

Andre Agassi became famous for being a professional tennis player, but his greatest legacy may be through his work in charitable and social causes. He now oversees both a charitable foundation and the Andre Agassi College Preparatory Academy, a tuition-free charter school for at-risk K-12 children. As both a tennis and education enthusiast, I’m a big fan. As part of their “Life’s Work” series, Harvard Business Review interviewed Agassi.

I especially liked this quote about his typical day in “retirement”, as my ideal schedule is starting to look the same. Maybe not work every morning, but at least some mornings. Hiking, sports, or some other outdoor activity otherwise.

At the C2 Montreal conference earlier this year, you said a typical day for you now involves working in the morning but finishing by 2:30 in the afternoon to pick up your kids in the carpool line.

I have the luxury of tweaking the balance now, of never missing a baseball game or a dance competition. If I’m feeling like I need a business outlet, I plan work. But yes, I engage much harder with my kids because they grow up fast. By the time you’re qualified for the job, you’re unemployed.

The whole point of financial freedom is to do whatever you want, whether that means zero work, only charitable work, part-time work, or even more. Consider this quote from the man who has spent thousands of hours editing Wikipedia (over a million times)… for free.

Everyone should do work that is not for money. I believe that when you have free time, you shouldn’t spend it idling. I’m able bodied; globally speaking (though not at all locally speaking), I’m rich. I have a lot of resources other people don’t have — an internet connection, free time, the ability to speak English — and it’s incumbent upon me to use them to make the world a better place.

But back to Agassi – here he is on taking ownership of your career. I would expand this to perhaps your savings and investments?

What do you regard as your biggest career mistake?

I wish I had taken ownership of the business side of my career years ago instead of trusting certain people. Nobody cares more, or represents you better, than you do yourself.

Finally, he explains his intensive approach to changing the lives of children.

What sets your school apart?

One difference is time on task. There are no shortcuts. We have longer school days—eight hours versus six. If you add that up, it’s 16 years of education versus 12 for district peers. There’s also an emphasis on accountability, which starts with the kids themselves. They know this is a privilege: There are 1,000 kids on the waiting list. So they take ownership. The teachers have annual contracts; there’s no business in the world that could succeed if employees who worked for three years got a job for life. The parents are accountable too. They need to acknowledge, accept, and embrace the objectives set for their children. They come in, they volunteer time, they sign off on homework assignments. You have to cover all the bases.

Update 2015. The Tennessee Promise program has welcomed 15,000 students in their first year of offering free community college tuition. The number of students attending community college full-time straight from high school grew 14%. This

Update 2015. The Tennessee Promise program has welcomed 15,000 students in their first year of offering free community college tuition. The number of students attending community college full-time straight from high school grew 14%. This

Many people want to take advantage of the tax benefits of 529 college savings accounts, but don’t want to deal with the volatility of stocks or bonds. Perhaps the beneficiary will need the funds soon, or you want the security of FDIC insurance. Many students are now adults saving for their own educations in a few years. In this case, consider the Virginia CollegeWealth 529 Savings Account and its following features:

Many people want to take advantage of the tax benefits of 529 college savings accounts, but don’t want to deal with the volatility of stocks or bonds. Perhaps the beneficiary will need the funds soon, or you want the security of FDIC insurance. Many students are now adults saving for their own educations in a few years. In this case, consider the Virginia CollegeWealth 529 Savings Account and its following features: I’m getting ready to put down a decent chunk of money into a 529 college savings plan, which means lots of research as there are a lot of options and nuances. A general plan for those without strong investment preferences would be to go with one of the age-based portfolios from a

I’m getting ready to put down a decent chunk of money into a 529 college savings plan, which means lots of research as there are a lot of options and nuances. A general plan for those without strong investment preferences would be to go with one of the age-based portfolios from a

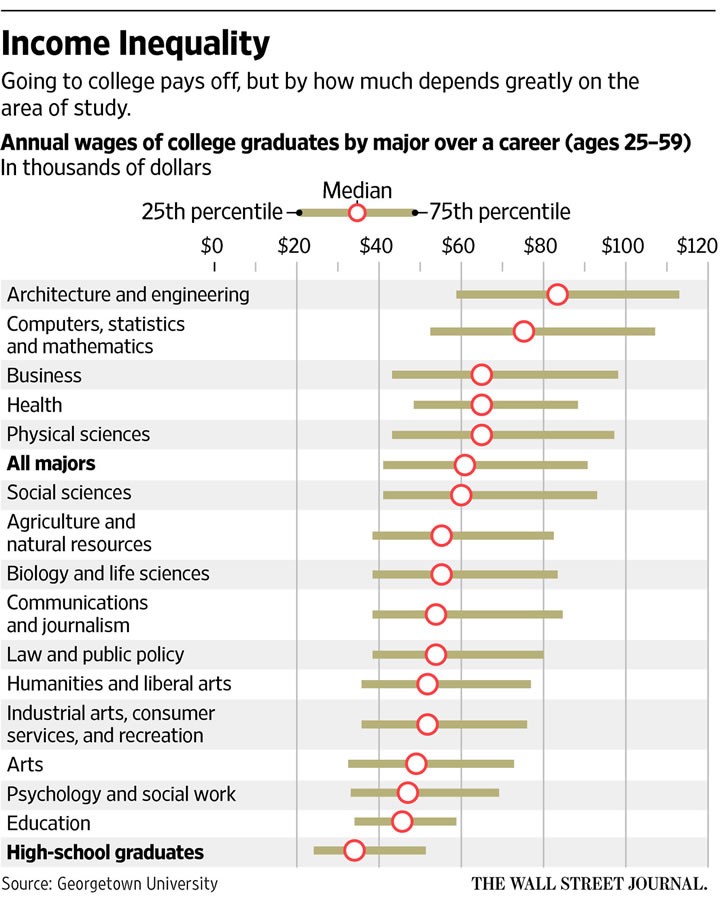

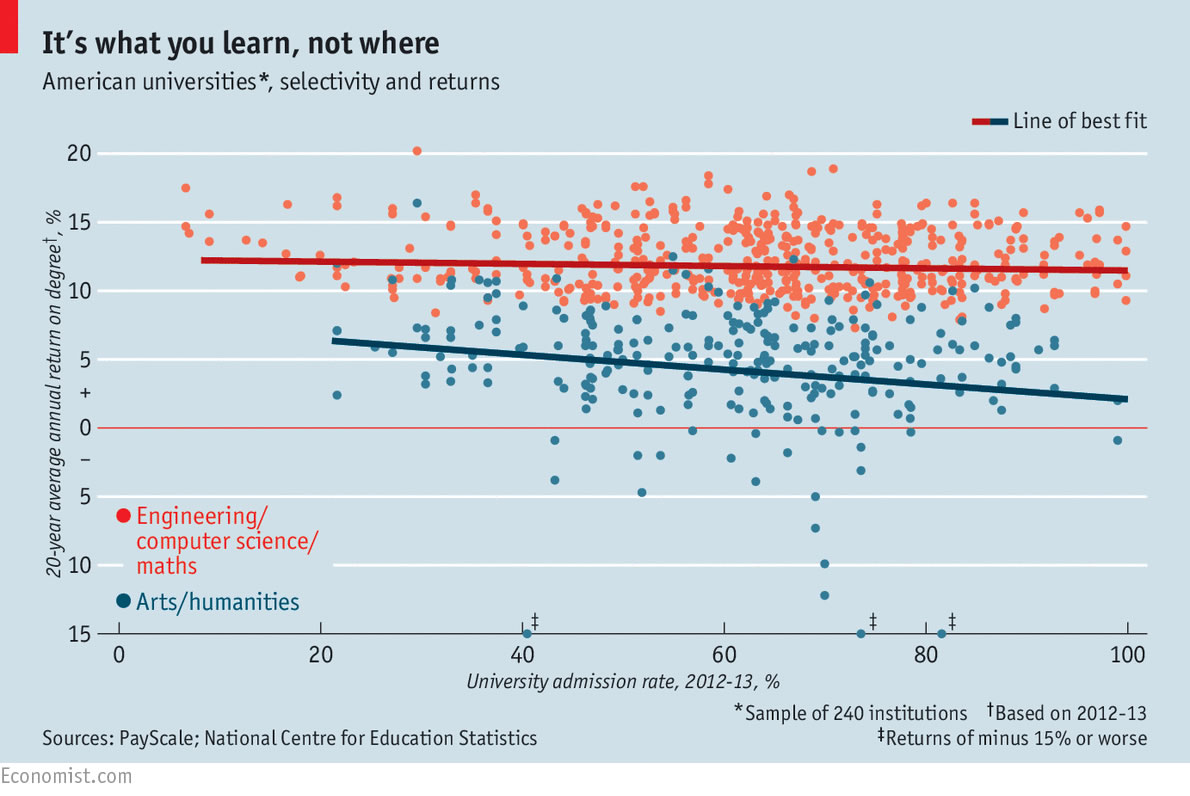

The new fall semester is underway, which means more college articles! Morgan Housel of Fool.com recently talked about how the

The new fall semester is underway, which means more college articles! Morgan Housel of Fool.com recently talked about how the  The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)