Multiple sources are suggesting that increasing student loan debt levels will have a significant impact on future housing prices because people will delay their home purchases (or put them off entirely). Although that seems like a reasonable assumption, I haven’t actually seen any hard data on it.

In a recent Vanguard research paper titled No bubble to burst: U.S. student debt is not housing [pdf], they took data from the Federal Reserve’s 2010 Survey of Consumer Finances and U.S. Census Bureau and found that:

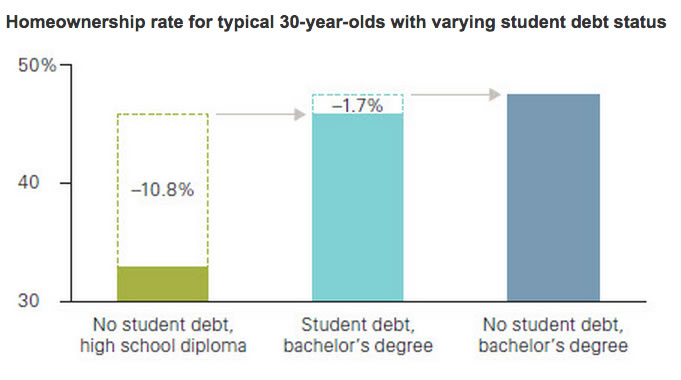

Although financing a bachelor’s degree with student debt decreases the likelihood of a typical 30-year-old college graduate purchasing a home by –1.7%, obtaining that degree also increases the likelihood of purchasing a home by 10.8%, relative to not attending college at all.

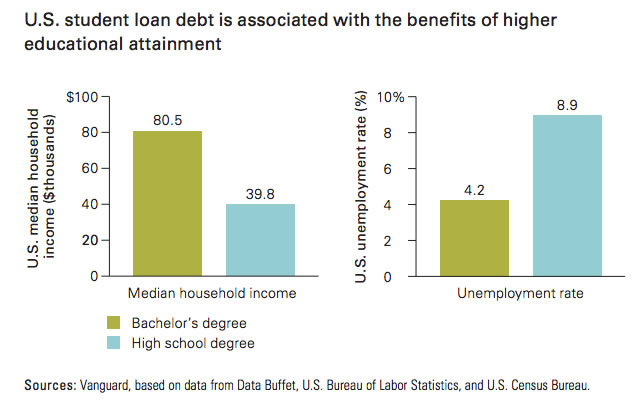

In the end, the conclusion seems to still be consistent with other findings. Getting that college degree is still “worth it” financially, even with the accompanying debt, at least on average. Your income is higher, you’re less likely to be unemployed, and you are more likely to own a home.

I suppose the primary thing to avoid is to not be above average on the debt. If you have to take on $120,000+ of debt just to get a 4-year degree, you’re probably going to the wrong school anyway. If the school really wanted you, they’d offer you a better aid package with grants and/or tuition waivers.

Fidelity Investments recently made a 40% reduction on the management fees for their direct-sold 529 Index Portfolios, with total expense ratios now ranging from 0.19-0.29%, down from 0.25-0.35%. Fidelity runs

Fidelity Investments recently made a 40% reduction on the management fees for their direct-sold 529 Index Portfolios, with total expense ratios now ranging from 0.19-0.29%, down from 0.25-0.35%. Fidelity runs  Right now, freshmen are moving into dorms all around the country and parents are scrambling to pay the bills. I’ve written about how many students

Right now, freshmen are moving into dorms all around the country and parents are scrambling to pay the bills. I’ve written about how many students  The Georgia Institute of Technology and Udacity.com are partnering together to offer an accredited master of science degree in computer science (

The Georgia Institute of Technology and Udacity.com are partnering together to offer an accredited master of science degree in computer science (

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)