Here is a new Amazon/AmEx promotion that promises “$20 off at Amazon after you make a single purchase of $50 or more using your American Express card”. However, the promotion has a lot of fine print to note:

Here is a new Amazon/AmEx promotion that promises “$20 off at Amazon after you make a single purchase of $50 or more using your American Express card”. However, the promotion has a lot of fine print to note:

- You must purchase products “sold by Amazon.com” or “sold by Amazon Digital Services LLC” by 7/22/20. Amazon e-gift cards do not qualify.

- You must spend $50+ on a single purchase using “any eligible American Express Consumer Card”.

I don’t see any notice that you qualify for the promotion at Checkout.Update: I tried again and when I do the proper things, I see a tiny “Qualifying offers: Promotion applied” message under my Order Total at Checkout. After the order actually ships, you will receive a confirmation e-mail with the promo credit.- The $20 promotional credit can only be used at the Amazon Moments store, which are “curated 4-Star & Above items”.

- Promotional credit must be redeemed by August 22, 2020.

- Offer limited to one per customer and account only.

This is one of those promotions where if I need to buy $50 of stuff, I’ll definitely try to qualify by using my consumer American Express card and checking out by the deadline, but I won’t go out of my way. (They should more clearly define what is an “eligible” American Express Consumer card.) I’m not quite sure of the point of this “curation” when it consists of a long list of 1,000+ items in every category. Who is going to shop Amazon this way?

My two “keeper” consumer American Express cards are the Blue Cash Preferred from AmEx (6% cash back on US supermarkets, up to $6,000 annually) and the Amex EveryDay Card (keeps my Membership Rewards points active with no annual fee, helps qualify for various Amazon promotions).

The

The

While not exactly a fun exercise, do you know where you’d turn for some extra cash in an extended emergency? Morningstar has

While not exactly a fun exercise, do you know where you’d turn for some extra cash in an extended emergency? Morningstar has

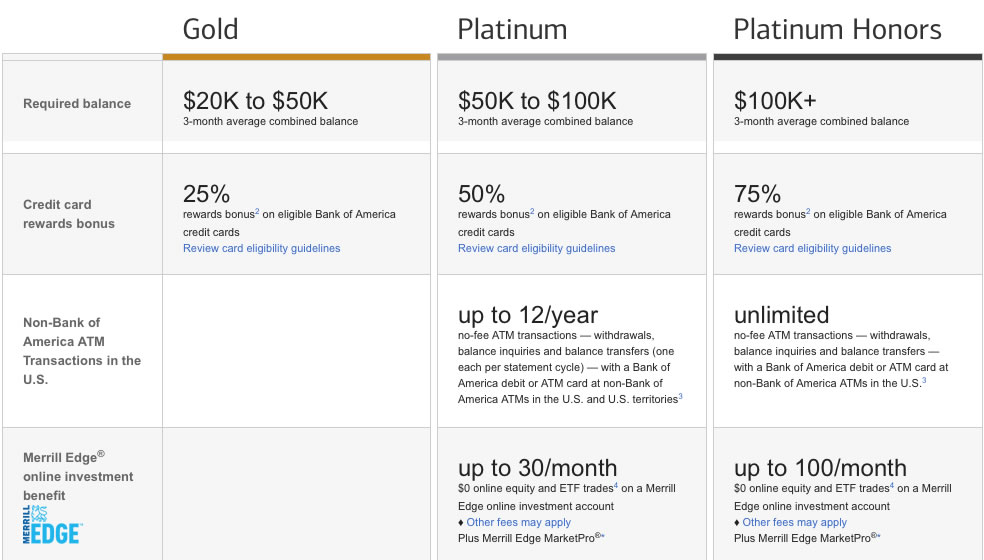

Bank of America is running their

Bank of America is running their

Bank of America is running their

Bank of America is running their  New bonus. Chase has a new

New bonus. Chase has a new  Today, Walmart launched their new

Today, Walmart launched their new  Equifax has reached a settlement with the Federal Trade Commission, the Consumer Financial Protection Bureau, and 48 out of 50 states over their huge data breach that was discovered in 2017. You can find full details at

Equifax has reached a settlement with the Federal Trade Commission, the Consumer Financial Protection Bureau, and 48 out of 50 states over their huge data breach that was discovered in 2017. You can find full details at  The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)