What’s in my wallet? Besides trying to land at least $500 on new sign-ups, which cards do I end up using on a regular basis? Apparently, the last time I answered this question was in 2006, more than a decade ago?! Let’s see if I have made any improvements since then. These are the cards that work best for my spending patterns and redemption preferences.

All-around cash back rewards card.

- 2006: MBNA/Fidelity Investments 529 College Rewards Card. I still have this card, although it is in sock drawer mode now. This Fidelity-branded card went from being issued by MBNA, to FIA Cardservices (subsidiary of Bank of America), now to Elan Financial services. The 2% rewards did help me rack up over $8,000 in tax-deferred college savings (including appreciation from investments).

- 2016: BankAmericard Travel Rewards Card. After moving over $100,000 of existing index funds from Vanguard and qualifying for their Platinum Honors tier, this enabled me to earn 2.625% cash back on all my purchases – redeemed as a statement credit offsetting any travel purchase. That’s a 31% improvement on 2% rewards. If you don’t have $100k in assets to move over, 2% is still double the 1% many cards give on all purchases – I have the Citi Double Cash card as backup.

Category-specific rewards credit card.

- 2006: Citi Dividend Platinum Select Mastercard. This card is no longer available to new applicants, which is probably why the 5% categories got rather stale. I’m a bit embarrassed to admit that I stopped using it so long that Citi closed it due to inactivity. Whoops! It was one of my older cards, but not a big loss as I have so many other cards to contribute to my “average age of accounts” stat.

- 2016: Chase Freedom Visa and Discover It Card. This quarter, the Chase Freedom is giving 5% cash back at Costco, Sam’s Club, Walgreens, and CVS ($1,500 total). The Discover It card is giving me 5% cash back at Amazon.com. Overall, I think recent competition has made the 5% categories more useful. Note that Chase Freedem technically earns Ultimate Rewards points, which can provide even higher value when redeemed for points/miles (see below).

Points or miles rewards card.

- 2006: Starwood Preferred Guest American Express Card. Still a good card overall (we’ll see how the merger changes things). If you redeem in 20,000 point increments, it will provide 1.25 miles per dollar spent for a variety of airline programs. However, I don’t travel as much as I used to, and even at a 2 cents per mile valuation, that’s only 2.5% back on value (more than 2%, but less than the 2.625% above). SPG does not transfer 1:1 to United. I don’t travel for business much these days so I can’t rack up SPG points for hotel stays as quickly anymore, and I also don’t need this card to keep my stash of SPG points active and useful.

- 2016: Chase Sapphire Preferred card. This card gives 2 Ultimate Rewards points per dollar spent on travel and dining out. Ultimate Rewards points transfer 1:1 to both United and Hyatt, for some solid redemption value. If you value at 2 cents per UR points, that’s 4% back value. I also need this card to keep all of my Ultimate Rewards stash active and available to transfer to the various airline and hotel partners. (I also earn UR points elsewhere from Chase Freedom, Ink business card, and their shopping portal.) If you haven’t had 5 new credit cards in the last 24 months, you should check out the Chase Sapphire Reserve card as well.

ATM Debit card.

- 2006: Bank of America ATM card. I still have this account, but got tired of how BofA pays no interest and charges you money to initiate a transfer out. If I have to use a online bank as a transfer hub all the time, I’m just going to make that hub my primary account.

- 2016: Ally Bank ATM card. These days, it’s a lot easier to do all of your banking at an online bank with no branches. Mobile deposit with smartphone camera is much easier than scanner. ATM rebates allow me to use any ATM, and up to $10 per statement cycle in rebates is enough for me (Allpoint ATM network is free and doesn’t count towards limit). 1% APY on savings account, which serves as free overdraft source for checking. Their app is solid, I can easily imitate interbank funds transfers (and I can login with just my thumbprint).

So the overall theme of what goes in my wallet has stayed the same, but the players have around changed a bit.

The Delta American Express card line-up has some

The Delta American Express card line-up has some

Marriott completed its acquisition of Starwood Hotels last week, and has already started the merging process for their loyalty rewards programs. Both programs will essentially be run separately for a while, but you can now match status and exchange points. The new name is Marriott International, although a full merger will not be completed until sometime in 2018. Here’s a quick summary of your options:

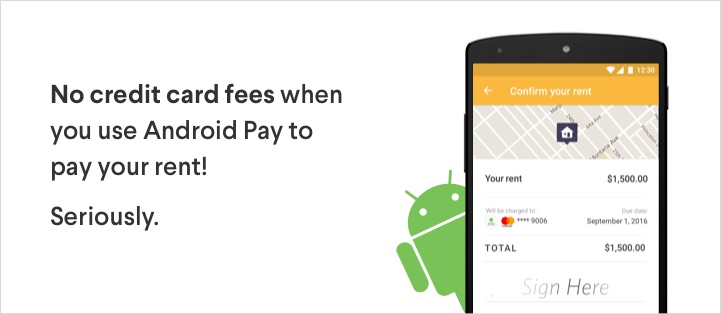

Marriott completed its acquisition of Starwood Hotels last week, and has already started the merging process for their loyalty rewards programs. Both programs will essentially be run separately for a while, but you can now match status and exchange points. The new name is Marriott International, although a full merger will not be completed until sometime in 2018. Here’s a quick summary of your options: With a new promotion by RadPad and Android Pay, you can pay your rent with a credit card (Visa, Mastercard, American Express) and earn points/miles/cash rewards through the end of 2016. Your landlord will simply receive a check on your behalf from RadPad.

With a new promotion by RadPad and Android Pay, you can pay your rent with a credit card (Visa, Mastercard, American Express) and earn points/miles/cash rewards through the end of 2016. Your landlord will simply receive a check on your behalf from RadPad.

If you have an Ally Bank savings or checking account, you’ve likely been pitched their new

If you have an Ally Bank savings or checking account, you’ve likely been pitched their new

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)