John Oliver of HBO’s Last Week Tonight did a humorous monologue on why credit reporting bureaus are awful. Appropriately, it was last week and I finally got around to watching the 18-minute video tonight. Here is the full video link, embedded below:

Here’s the condensed version:

- Your credit report can affect your ability to borrow (and thus buy a home), your ability to rent, the price you pay for all kinds of stuff, and even your ability to get a job. Sheesh, what else is there left?

- 1 in 20 credit reports have errors that are significant enough to hurt your chances at the rather important things I just listed above. That’s 10 million Americans.

- In an effort to show Equifax, Experian, and TransUnion how such errors can hurt both reputations and business, they created the three websites Equifacks.com, Experianne.com, and TramsOnion.com. (Warning: I left some of these unlinked because they may be considered NSFW.)

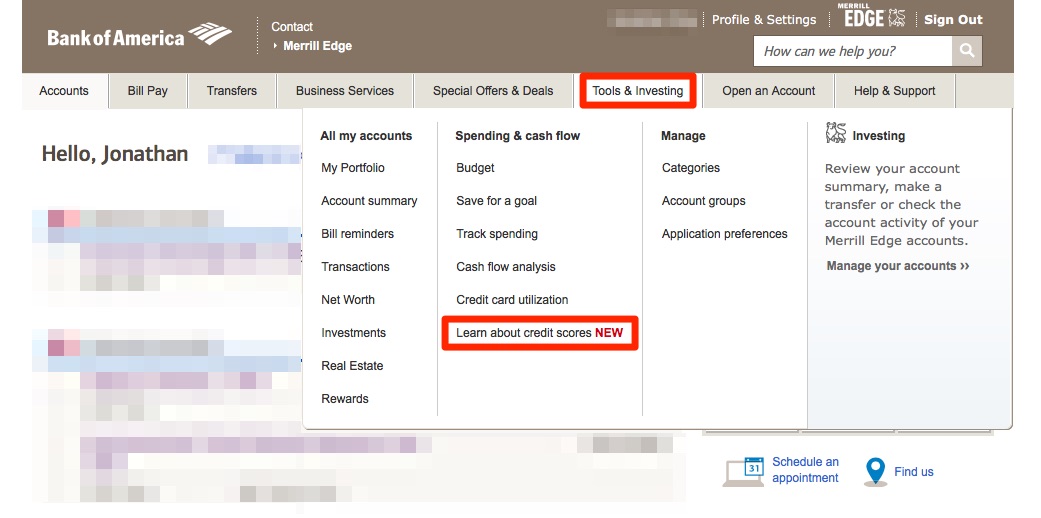

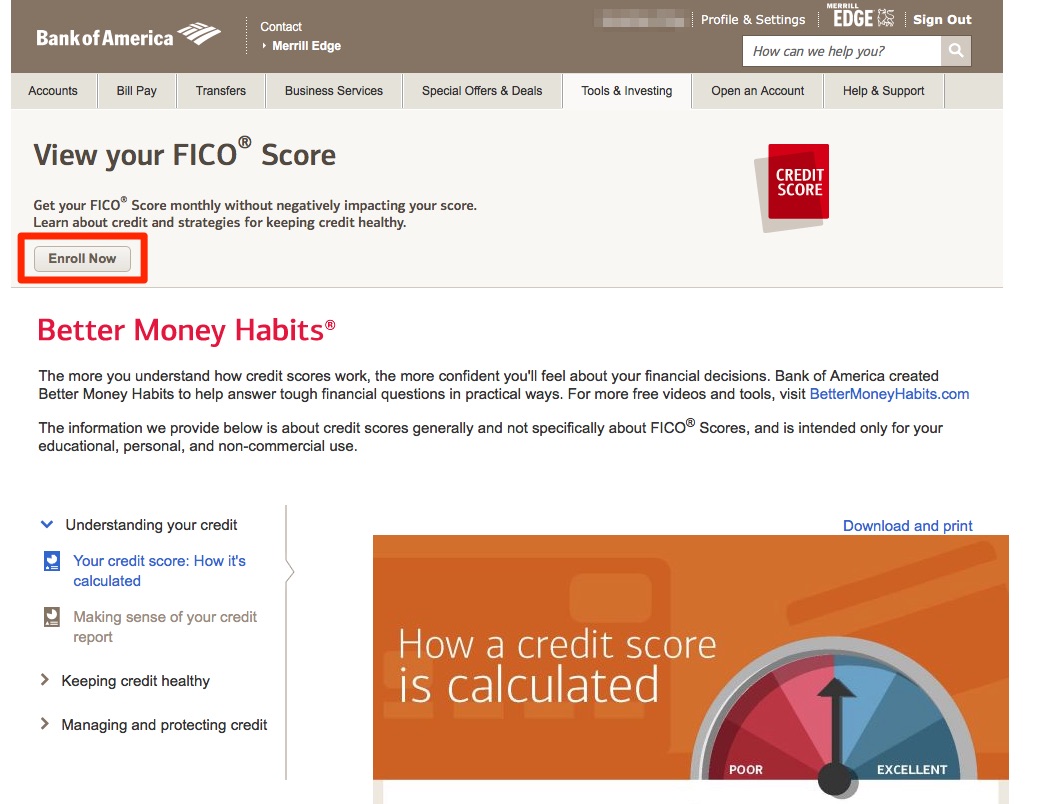

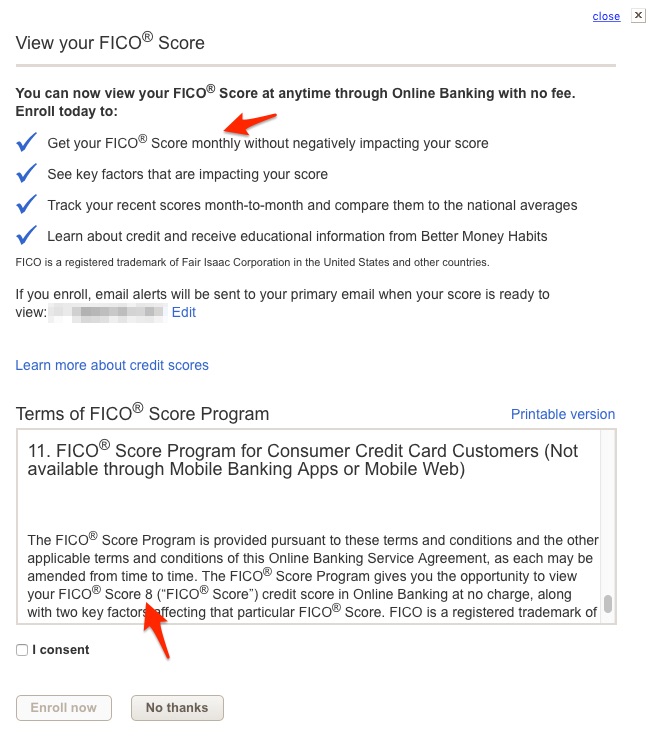

In general, I do not micromanage my credit score, but it is scary than an error outside your control could have such harmful effects on your day-to-day life. Perhaps this information will also motivate you to check your credit and consumer reports if you haven’t done so recently. There are also an increasing number of free and/or ad-supported sources of credit reports, credit monitoring, and credit scores. The bad news is that the error dispute process is still slow and complicated, and after you try patience and perseverance, you may need to lawyer up in order to get their attention.

We all know that personal income tax filings are due soon, but so are the first round of quarterly estimated taxes for 2016. Many of us with freelance or side-gig income must makes these payments in order to avoid a tax penalty at the end of the year.

We all know that personal income tax filings are due soon, but so are the first round of quarterly estimated taxes for 2016. Many of us with freelance or side-gig income must makes these payments in order to avoid a tax penalty at the end of the year.

Highlights of the new JetBlue Plus card:

Highlights of the new JetBlue Plus card:

It has been nearly a year since I picked up my

It has been nearly a year since I picked up my

Most travel cards offer an ongoing sign-up bonus, but it’s even better when you snag them during a bump-up – this time it is the Marriott Rewards® Premier Credit Card from Chase. Check out the highlights below, and remember that it is free and takes just a minute to add an authorized user:

Most travel cards offer an ongoing sign-up bonus, but it’s even better when you snag them during a bump-up – this time it is the Marriott Rewards® Premier Credit Card from Chase. Check out the highlights below, and remember that it is free and takes just a minute to add an authorized user:

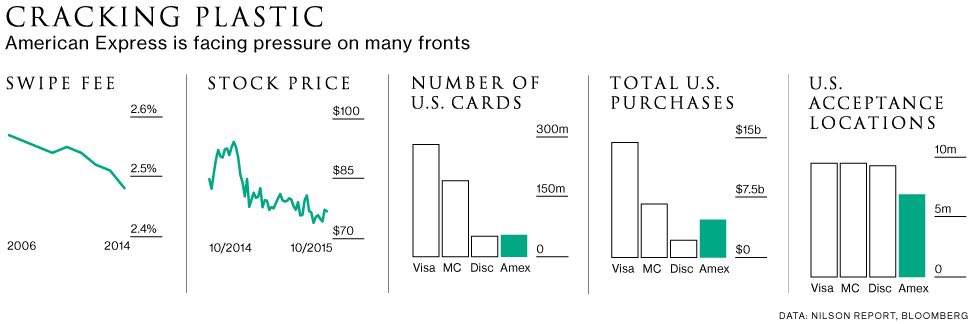

As you’ve probably heard, the Square IPO was completed last week. For a while, I didn’t understand how a company could have a $4 billion valuation when they basically offer a simplified merchant account. They let small businesses accept credit cards, which means they skim a tiny bit off the 2.75% they charge while most of it goes straight to the networks. (Add in their other expenses, and Square has never made a profit.) Wouldn’t you rather own Visa or American Express directly?

As you’ve probably heard, the Square IPO was completed last week. For a while, I didn’t understand how a company could have a $4 billion valuation when they basically offer a simplified merchant account. They let small businesses accept credit cards, which means they skim a tiny bit off the 2.75% they charge while most of it goes straight to the networks. (Add in their other expenses, and Square has never made a profit.) Wouldn’t you rather own Visa or American Express directly?

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)