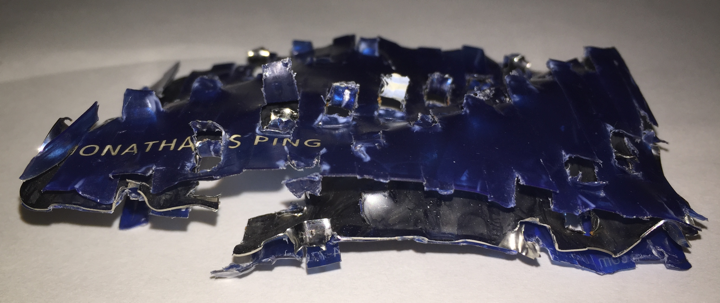

Every credit card is getting a smart chip these days, which means a lot of expired cards. My shredder is rated for 12 sheets of paper at a time, and up until recently handled every credit card, CD, and DVD sent its way. But not the Chase Sapphire Preferred credit card. I knew it had a little extra heft due to some sort of metal (aluminum?) sandwiched between layers of plastic, but that fact somehow didn’t register in my shredding fervor… until I heard an awful crunching noise:

Every credit card is getting a smart chip these days, which means a lot of expired cards. My shredder is rated for 12 sheets of paper at a time, and up until recently handled every credit card, CD, and DVD sent its way. But not the Chase Sapphire Preferred credit card. I knew it had a little extra heft due to some sort of metal (aluminum?) sandwiched between layers of plastic, but that fact somehow didn’t register in my shredding fervor… until I heard an awful crunching noise:

The results: The numbers on the back of the card are still visible, and the magnetic strip may still be readable. My shredder still works, although it has been making some funny noises. Not sure what to do with it now, perhaps industrial-grade shredder could finish the job? Now you know why Chase has started sending folks a prepaid mailer to send back your card when they replace it. 🙂

Bank of America is the issuer behind many different credit cards, but only a few of them carry the “BankAmericard” co-branding. I have written up reviews of the

Bank of America is the issuer behind many different credit cards, but only a few of them carry the “BankAmericard” co-branding. I have written up reviews of the

I’ve written about American Express gift cards several times in the past, mostly when they had a promotion waiving both their purchase fees and shipping fees. In such cases, they were a cheap and efficient way to “time-shift” your purchases if you needed to meet a spending threshold soon to obtain a sign-up bonus, or if you needed some miles sooner for a reward.

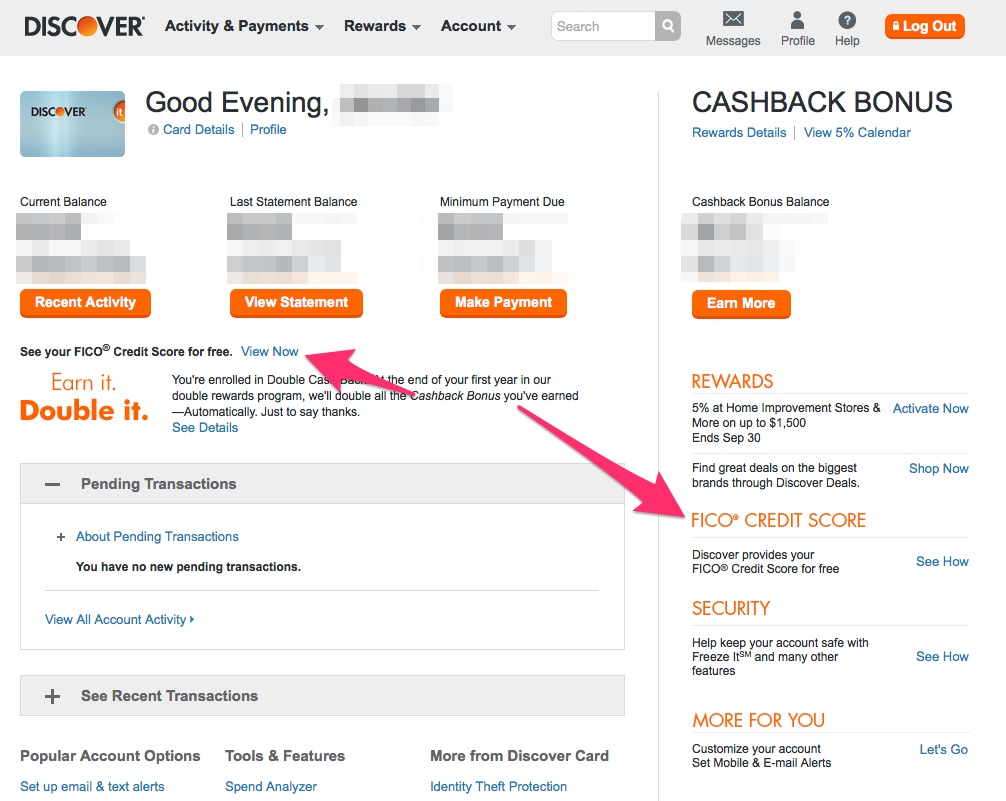

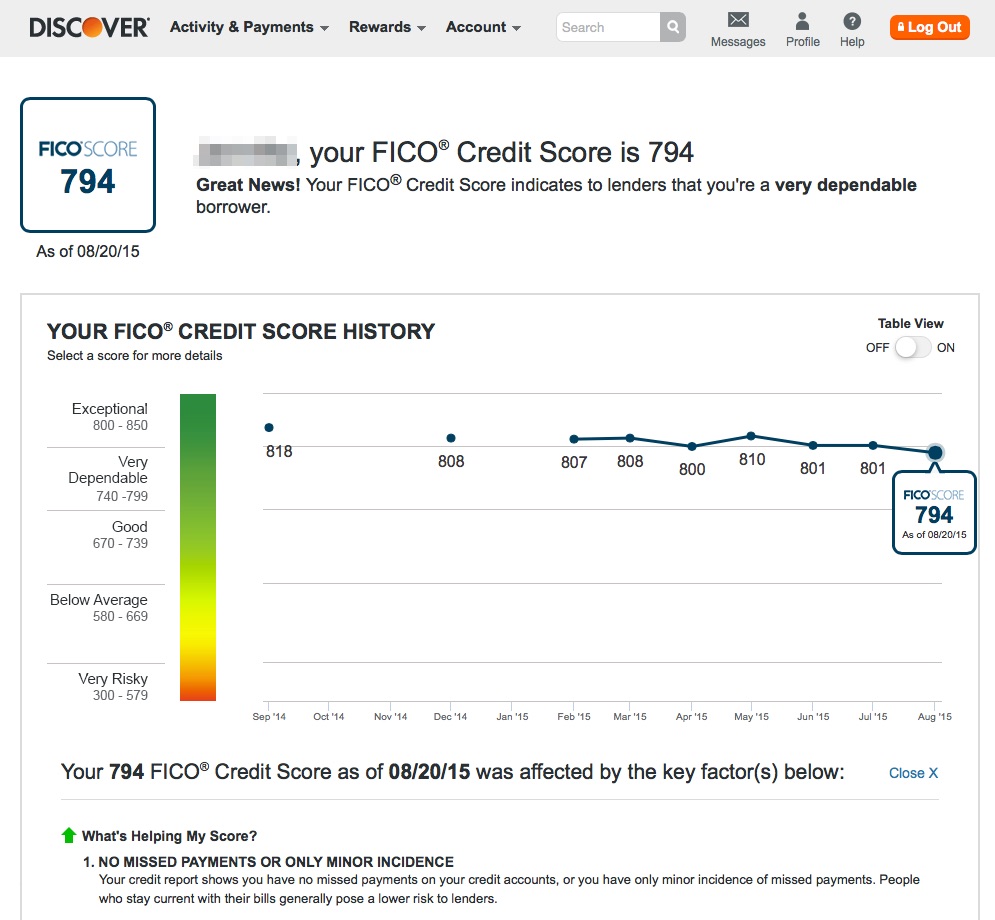

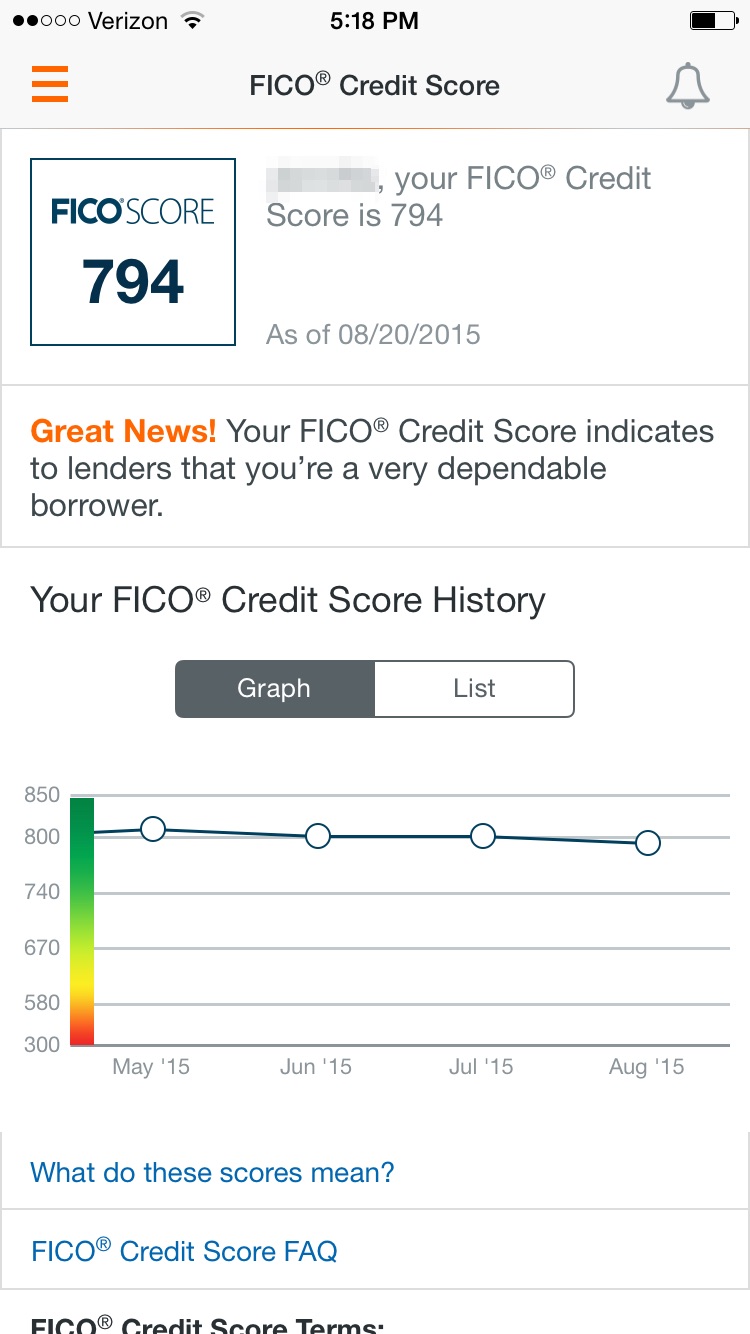

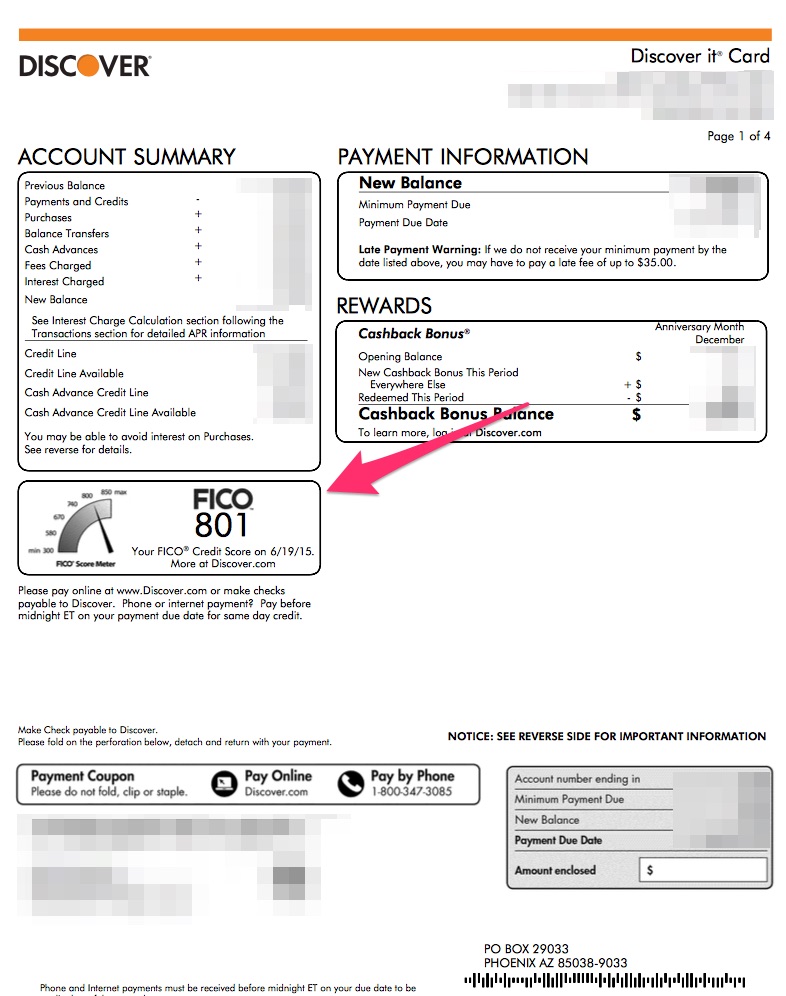

I’ve written about American Express gift cards several times in the past, mostly when they had a promotion waiving both their purchase fees and shipping fees. In such cases, they were a cheap and efficient way to “time-shift” your purchases if you needed to meet a spending threshold soon to obtain a sign-up bonus, or if you needed some miles sooner for a reward. Discover credit cards will work with Apple Pay starting on September 16th, 2015. But the big news is that per this

Discover credit cards will work with Apple Pay starting on September 16th, 2015. But the big news is that per this  One of my long-time favorite credit cards is a grandfathered Fidelity College Rewards MasterCard that gives me 2% flat cash back on all purchases. I’m not sure exactly when I first applied for this card, but it was in the early 2000s. The current Fidelity line-up as of September 2015 is still pretty good (if you have a Fidelity account):

One of my long-time favorite credit cards is a grandfathered Fidelity College Rewards MasterCard that gives me 2% flat cash back on all purchases. I’m not sure exactly when I first applied for this card, but it was in the early 2000s. The current Fidelity line-up as of September 2015 is still pretty good (if you have a Fidelity account): This post provides updated information and instructions regarding the free FICO score that is available to select Chase credit card holders.

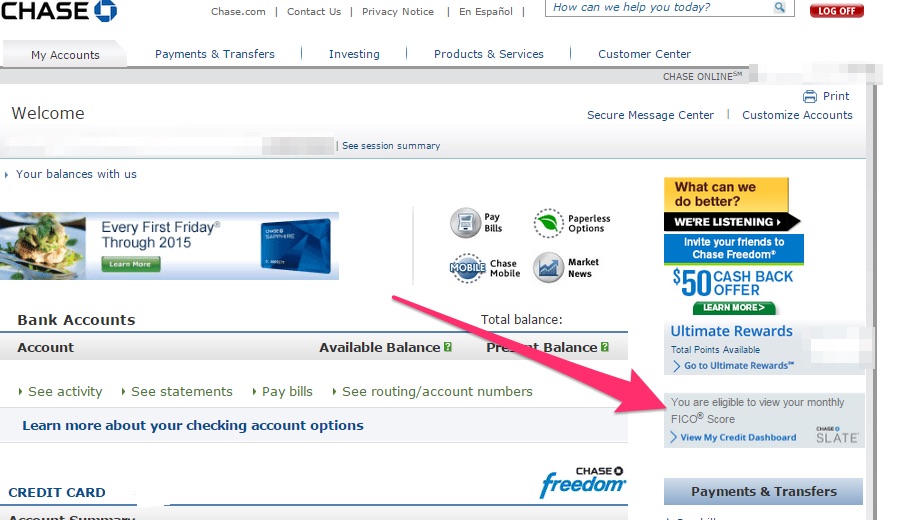

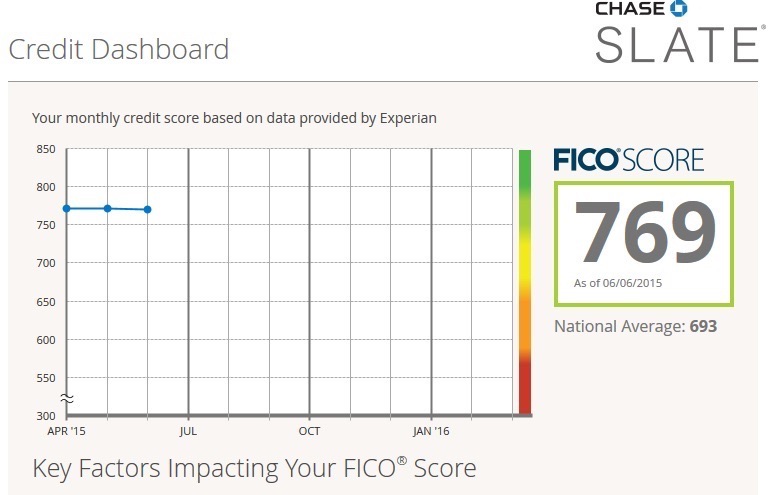

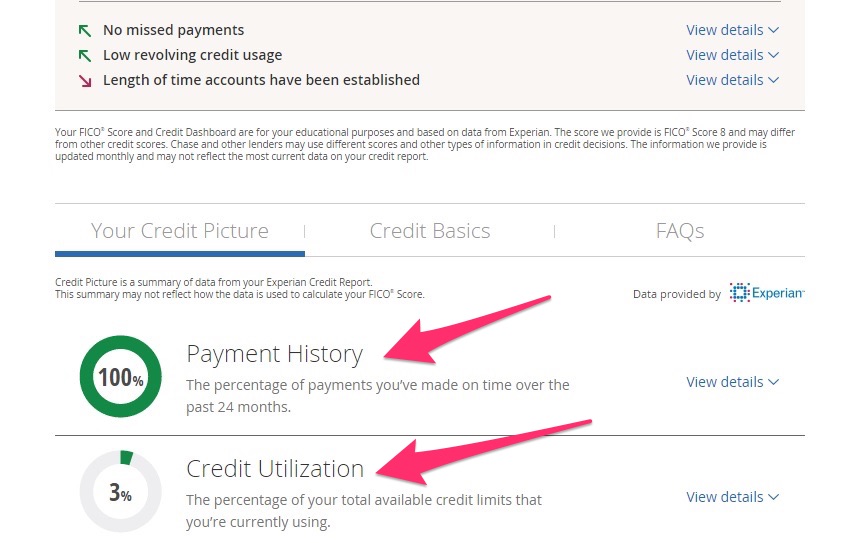

This post provides updated information and instructions regarding the free FICO score that is available to select Chase credit card holders.

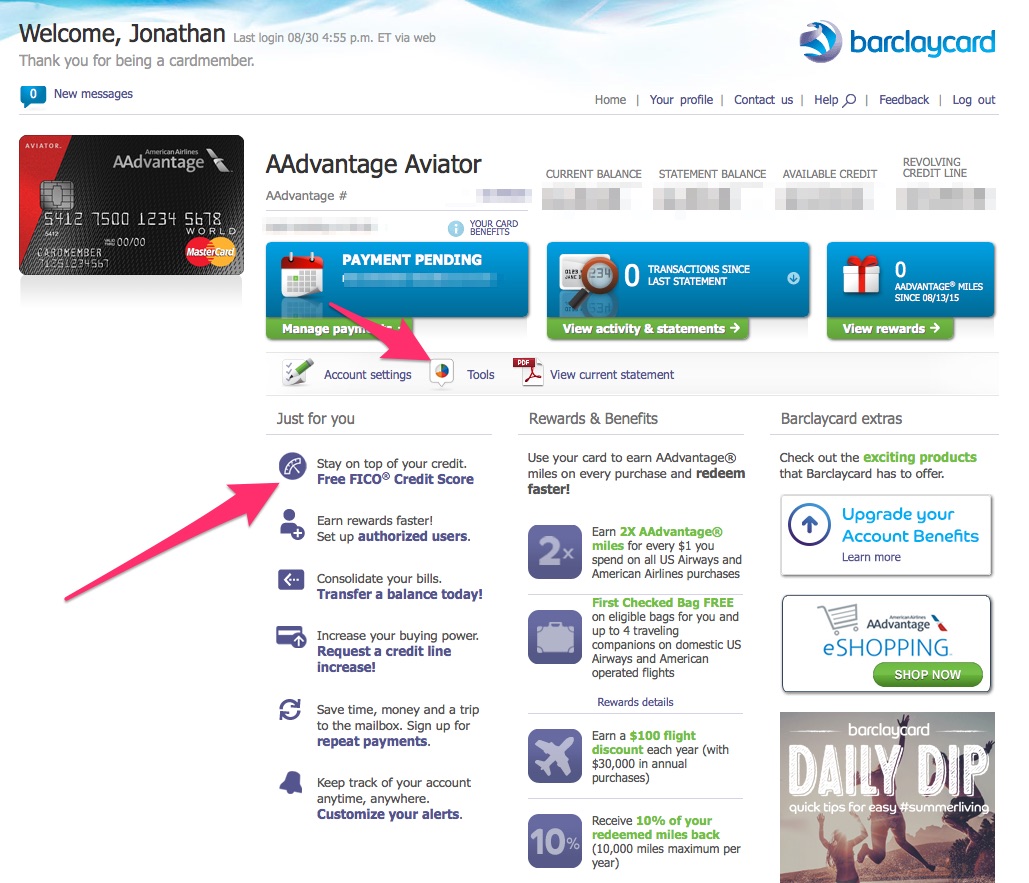

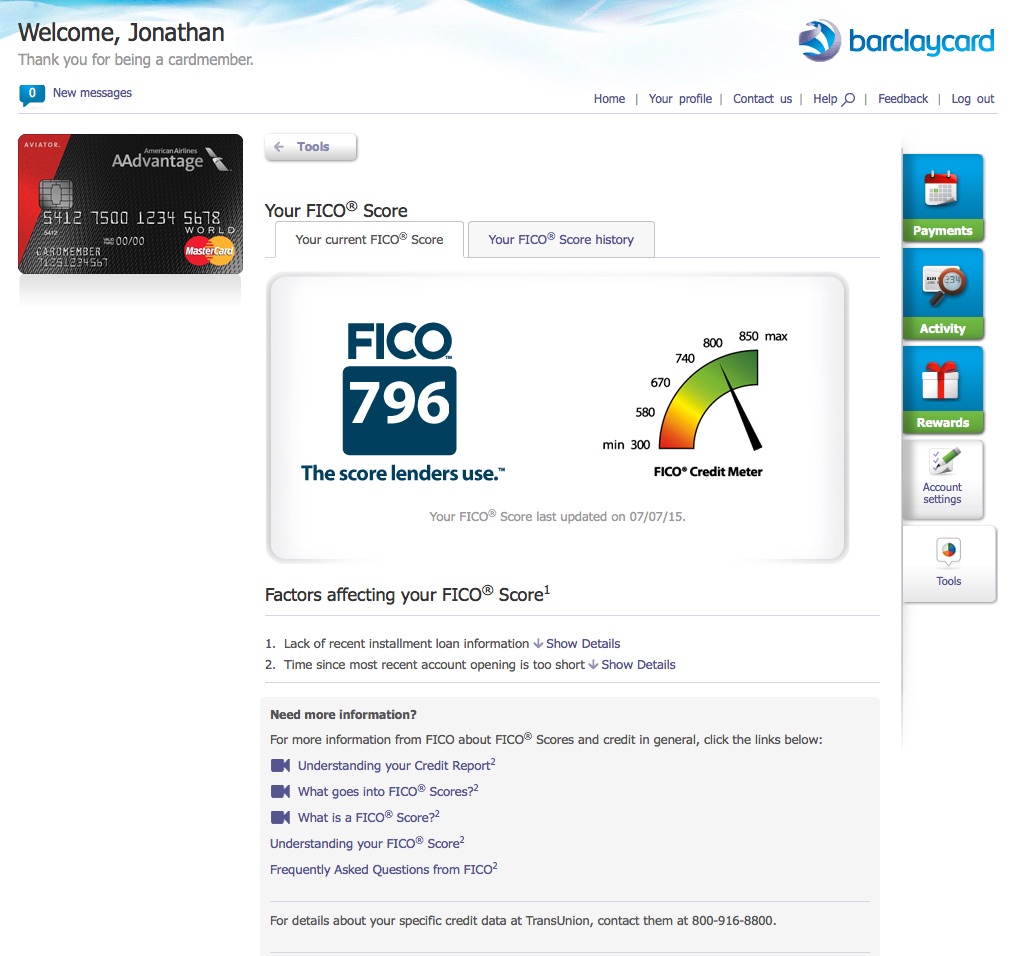

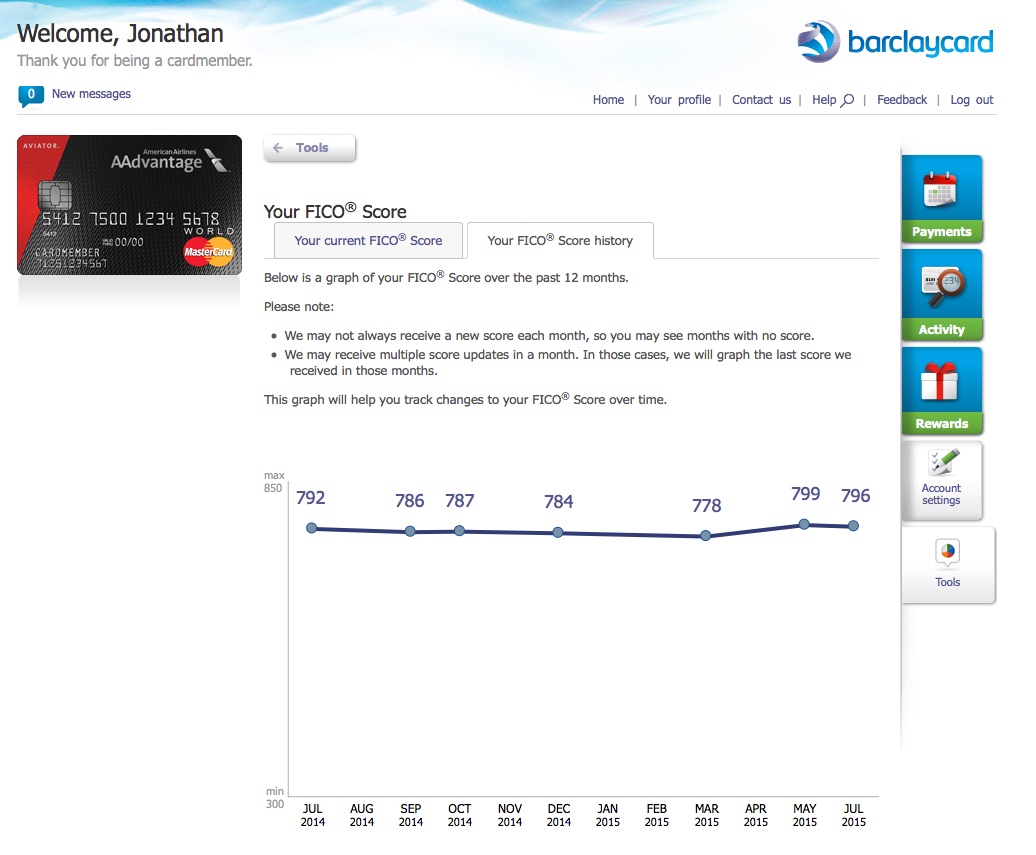

This post provides updated information and instructions regarding the free FICO score that is available to Barclaycard US credit card holders.

This post provides updated information and instructions regarding the free FICO score that is available to Barclaycard US credit card holders.

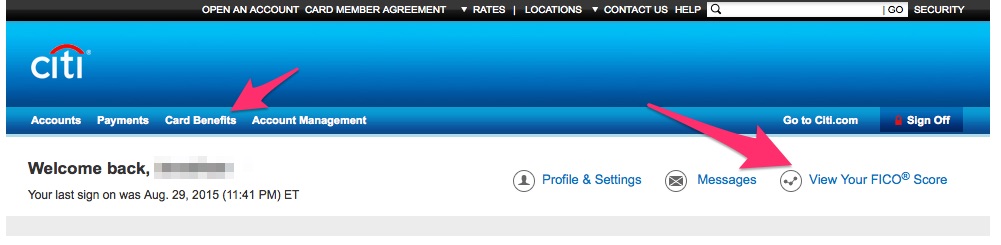

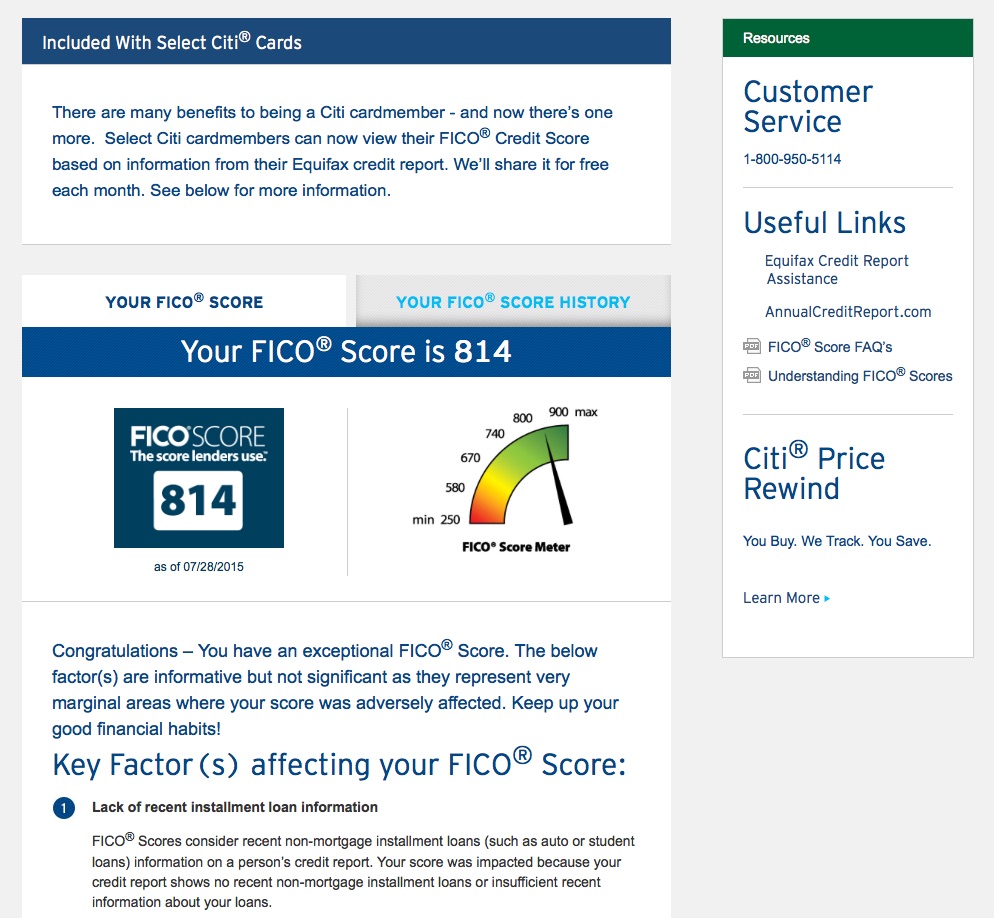

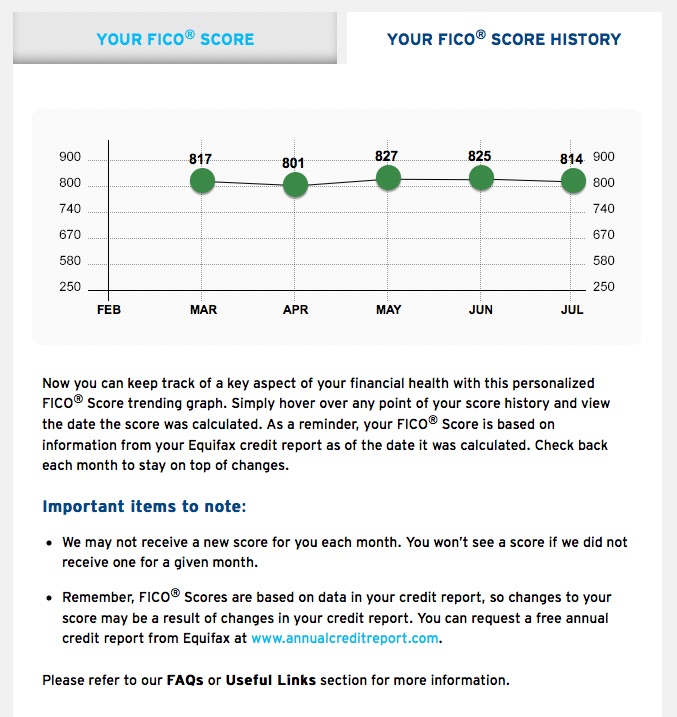

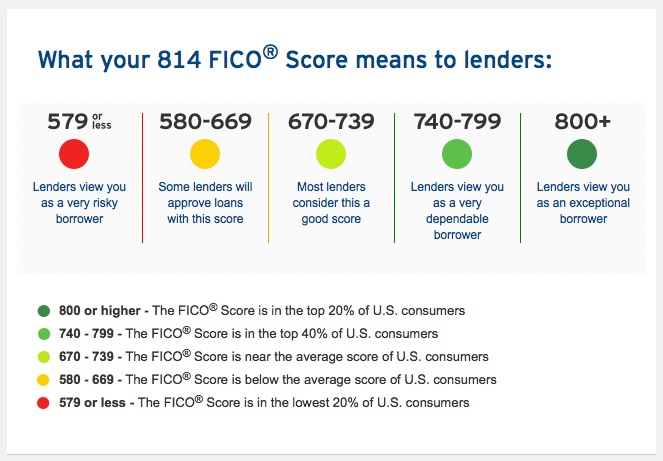

This post provides updated information and instructions regarding the free FICO score that is available to Citibank credit card holders.

This post provides updated information and instructions regarding the free FICO score that is available to Citibank credit card holders.

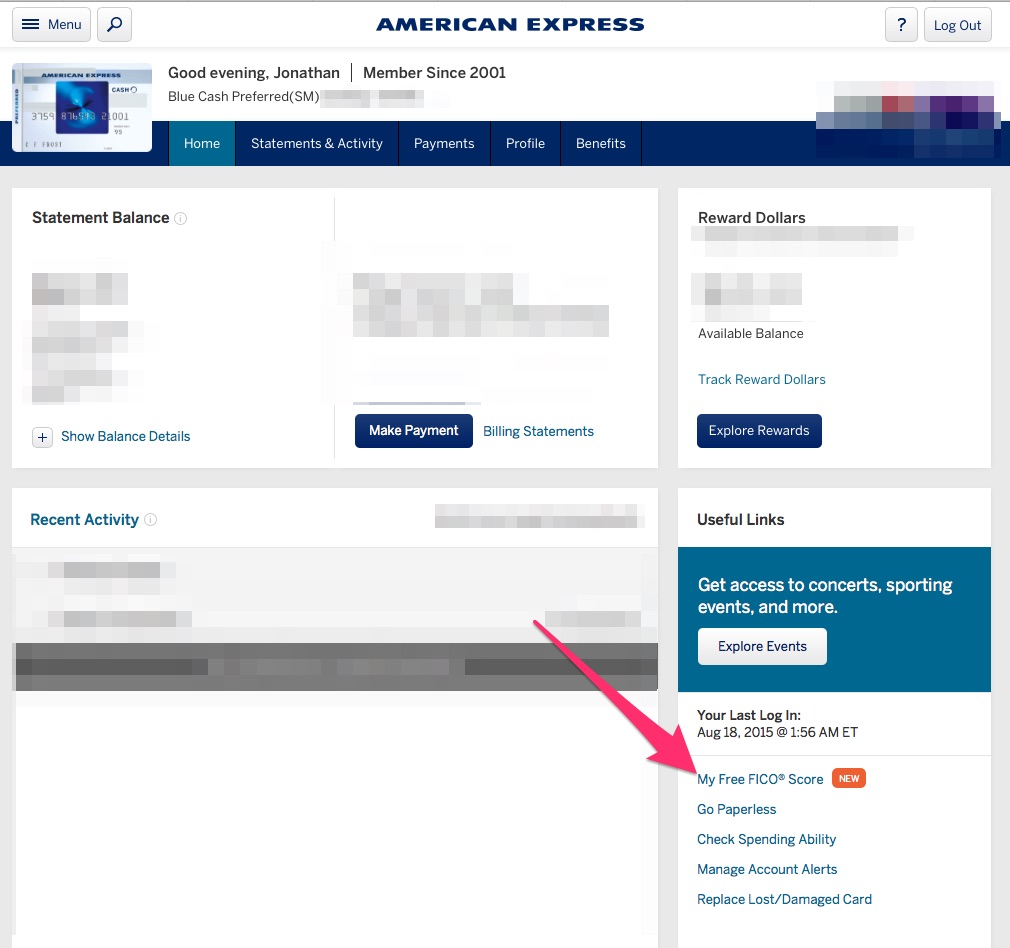

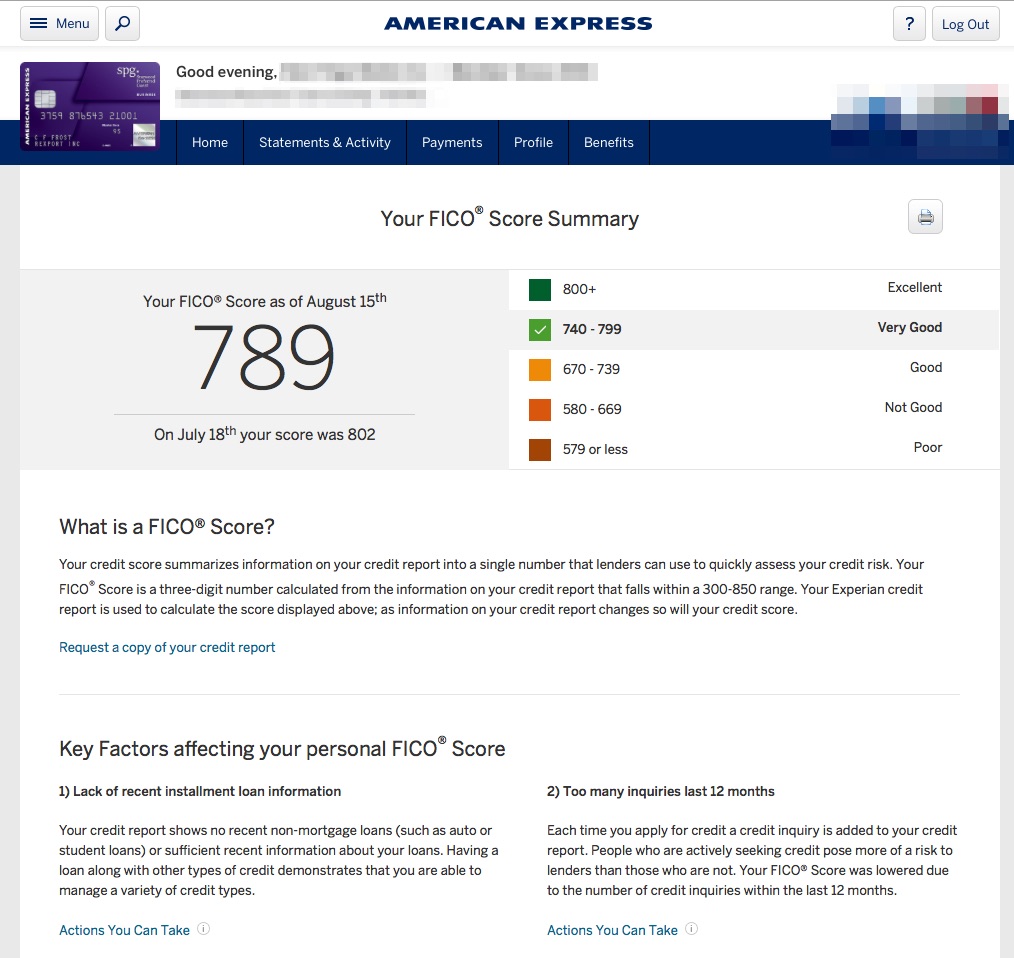

This post provides updated information and instructions regarding the free FICO score that is available to American Express credit card holders.

This post provides updated information and instructions regarding the free FICO score that is available to American Express credit card holders.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)