Bonus improved from 40k to 50k miles for limited time. American Airlines and US Airways have announced new details about their upcoming merger. As expected, the two frequent flier programs will merge and all the miles will become American AAdvantage miles in 2015. (US Airways Dividend miles will convert at a 1:1 ratio.) Along with that, they have updated both the Citi American Airlines card and Barclaycard US Airways card slightly.

Here are the updated features of the US Airways Premier World MasterCard®. I got the bonus myself (unfortunately at only 40k miles) and have posted details on that below as well.

- Earn 50,000 bonus miles after your first purchase and payment of the $89 annual fee

- First checked bag free on eligible bags for you and up to four companions on domestic US Airways operated flights only.

- One companion certificate good for up to 2 guests to travel with you on a US Airways operated flight at $99 each, plus taxes and fees.

- Priority boarding Zone 2 on US Airways operated flights only.

- Redeem miles for award travel on US Airways and American Airlines booked through usairways.com or US Airways Reservations

- Earn miles on every purchase with 2 miles for every $1 you spend on US Airways and American Airlines purchases and 1 mile for every $1 on purchases everywhere else

- New! Receive a 25% savings on eligible US Airways and American Airlines in-flight purchases

- Please see terms and conditions for complete details

Again, the unique thing about this card is that American Airlines and US Airways are merging and these bonus miles will become American miles. You can already book reward flights on American with US Airways miles. That also means this Barclaycard-issued card will no longer be accepting applications and you won’t be able to get its sign-up bonus or other unique perks ever again. It is reported that this card will eventually convert essentially into a Barclaycard American Airlines card. So these are miles I didn’t want to leave on the table.

Note that 50,000 mile bonus does not require any minimum purchase amount and that there is an $89 annual fee that is not waived for the first year. 50,000 miles for example is more than enough for a roundtrip from the US to Hawaii or even two roundtrips within the continental US, so that is worth it for me. The US Airways companion certificate is also a unique feature which would be awesome if it eventually applied to American flights (though it probably won’t).

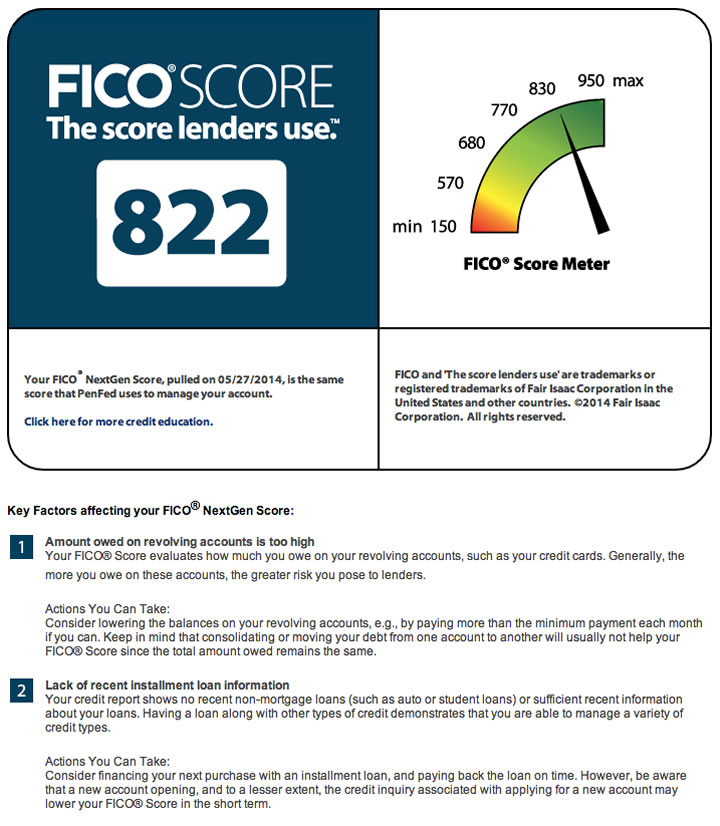

My bonus experience. Applied on 7/14. Approved on 7/21. First statement closed on 8/12, in which I charged $10 and also paid the $89 annual fee. I read some stories about other people making only a single purchase (the minimum technically required) but having to call in about the bonus. Thus, I put on another 4 small charges during the second statement period which ended 9/12 totaling about $49. My 40,000 bonus miles posted 9/13, one day after the closing of my second statement period. Here is a screenshot:

The card is issued by Barclaycard, which means you also get a free FICO score every couple months.

The October 2014 issue of Money Magazine features their annual rankings of the “Best Credit Cards”. Here’s a condensed list of their top picks for various categories. I’ve written about most of them, and in those cases I’m linking to that post which provides more details. Otherwise, I’m linking directly to the card page and including a few highlights about the card.

The October 2014 issue of Money Magazine features their annual rankings of the “Best Credit Cards”. Here’s a condensed list of their top picks for various categories. I’ve written about most of them, and in those cases I’m linking to that post which provides more details. Otherwise, I’m linking directly to the card page and including a few highlights about the card.

Home Depot has admitted they were recently hacked and customer information was compromised and stolen. If you have shopped at any Home Depot store after April 1, 2014, you are eligible for one free year of identity protection and credit monitoring at homedepot.allclearid.com (press release).

Home Depot has admitted they were recently hacked and customer information was compromised and stolen. If you have shopped at any Home Depot store after April 1, 2014, you are eligible for one free year of identity protection and credit monitoring at homedepot.allclearid.com (press release).  A couple of readers have asked me about the BankAmericard Better Balance Rewards credit card. It definitely has a unique rewards structure

A couple of readers have asked me about the BankAmericard Better Balance Rewards credit card. It definitely has a unique rewards structure

Update: This LTO is now EXPIRED

Update: This LTO is now EXPIRED The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)