If you’ve already hard about the guy who had the worst time ever cancelling his AOL account… and recorded the entire conversation, then skip the rest of this post. Otherwise, turn down the volume in your office cubicle and watch this:

[Read more…]

And You Thought You Had A Hard Time Cancelling!

Posted on June 23, 2006 // 22 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.Last updated: October 5, 2006

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Best ATM or Credit Card For Foreign Travel?

Posted on June 2, 2006 // 70 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.Just because you’re overseas on vacation, doesn’t mean you shouldn’t still pay attention to fees. Visa and Mastercard charge a standard 1% “conversion” fee on all foreign transactions (even if they are in US dollars!.) Many major credit card issuers charge you up to another 3% on top of that. Why? Because they can.

But by selected the best credit card in your arsenal, you can minimize the damage. Flyertalk has a great resource listing all the card issuers and the rates they charge. Don’t forget to also take into account the cashback program of your specific card, as you’ll still earn it on foreign purchases.

[Read more…]

Last updated: April 27, 2015

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

What’s a Hard Credit Check, And Why They’re Valuable

Posted on May 30, 2006 // 58 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.I talk a lot about “hard” and “soft” credit pulls. I don’t think I’ve ever actually seen these terms used by FICO officials, so it may be kind of confusing. Money geek slang, who knew? A credit check, also known as credit pull or credit inquiry, is (logically) when a third party wants to examine at your credit history.

A “soft” pull is one that does not affect your credit score. You can get 1,000 of these and it won’t matter as they are not visible to other people checking your credit. These are often done without your knowledge as long as they have a “permissible purpose by law”, and may include:

[Read more…]

Last updated: November 23, 2008

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Credit Score Myths – Don’t Cancel Old Accounts

Posted on May 25, 2006 // 28 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.Credit scores remain all the rage, but there are a lot of misconceptions out there. Four common ones are outlined in this MSN Money article titled ‘4 Credit-Scoring Myths‘. What’s the first myth? That closing credit cards will help your score.

No, no, no. For the umpteenth time: Closing accounts can never help your credit score, and may hurt it… It?s true that having too many open accounts can hurt your score. But once you?ve opened the accounts, you?ve done the damage. You can?t repair it by shutting the account, and you may actually make things worse… The credit score looks at the difference between your available credit and what you?re using. Shut down accounts, and your total available credit shrinks, making your balances loom larger, which typically hurts your score.

Last updated: September 28, 2011

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Drive A Lot? Use the Citi Driver’s Edge MasterCard

Posted on May 23, 2006 // 20 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.I’ve realized that I am in the minority when it comes to driving. I put on maybe 6,000 miles a year. Many people log over 20,000 miles on their car every year! If you are one of these road warriors, I just got e-mailed about the Citi Driver’s Edge Platinum Select MasterCard (Thanks JW). It looks great in multiple ways:

» You get rewards just for driving. You?ll earn $1 in Drive Rebates for every 100 miles you drive?up to $500 in Drive Rebates a year. Drive 20,000 miles a year? That’s $200 a year just for driving! To track miles and get rebates you just mail in your receipt whenever you get an oil change or other receipt.

» 6% cashback on gas for the first year. Obviously driving a lot = $$$ for gas. Assume you get 20 miles per gallon. Driving 20,000 miles, that’s 1,000 gallons. At $3 a gallon, that’s $3,000. Times 6%, that’s another $180 cashback on gas alone.

» You also get 6% back at supermarkets and drugstores for the first year (3% after that). That beats out the Citi Dividend Card (which I have) for the first year. You earn 1% on everything else. Here is Citi’s example chart of how this could add up:

» There is a cap of $1,000 per year, which is significantly higher than the $300 or the Dividend card as well and allows you to rack up more cash.

Come to think of it, this is not a bad card just to keep around. If you drive 10,000 miles in a year, that’s still $100 a year just for

driving. There is also no annual fee. What other card does that?

Rebates do expire if you don’t make a purchase in a year or if you don’t redeem within 5 years. Not too harsh. It’s all spelled out in the fine print on the application, so be sure to save a copy.

There is also a 0% APR balance transfer offer with this card, and as such is for people with good credit. But do not use it if you want to get these rebates. Remember, all payments go towards the balance at lowest interest rate.

What’s the catch?

The DriveRebates are redeemable as straight cash only towards car expenses. But that’s any car expenses – buying a car, leasing a car, oil changes, new tires, repairs, etc.

But, they can also be converted to ThankYou points. Each $1 in Driver?s Edge rebates is equivalent to 100 ThankYou Points, or put another way $100 in rebates can be converted to a $100 Gift Card at Target, Chevron, Gap, etc. Note: If you have student loans, you can still get straight cash towards those.

I think the easiest way to cash in on these points is just to get gas cards. Sure, you won’t be able to get 6% back anymore by buying with this credit card, but even after accounting for that you’re still getting 5.64% back which is still very good.

Hmmm…

As I write this, I’m convincing myself more and more to apply for this card. Even if I only drive 6,000 miles a year, that’s $60 – which will basically pay for all my oil changes and tires every year.

Update: I applied for this card myself, going to redeem for either gas or a set of tires.

Last updated: October 27, 2011

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Free Equifax Credit Alerts via PayPal

Posted on May 12, 2006 // 9 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.Equifax and PayPal have teamed up to provide a basic credit monitoring service that is free to anyone. I say it’s free to anyone because after you click on the sign-up link, there is no verification that you actually use PayPal when signing up. In fact, I already had an Equifax login from my free government-mandated credit reports, so I just used that and it grabbed all my info automatically. Two types of alerts are included:

- Upon an Equifax credit inquiry, or a

- Balance change over a chosen percentage or dollar amount.

I signed up a few days ago, and got my first balance alert today. It doesn’t tell you which credit card triggered the alert, which is a bummer. Still, not bad for free and now I’ll know when my Equifax credit is pulled.

Last updated: August 5, 2006

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Are Credit Card CashBack Rebates Taxable?

Posted on May 5, 2006 // 13 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.Hmm… the media seems to be addressing all my questions today. This Wall Street Journal column addresses the taxation of credit card rebates:

The IRS hasn’t issued any specific public guidance on whether cash-back card rebates are subject to income tax, says an agency spokesman. But the IRS did issue a private-letter ruling in 2002 that said certain card rebates aren’t included in a taxpayer’s gross income. Although a private-letter ruling applies only to the taxpayer that applied for it, such rulings are considered to be a gauge of the agency’s thinking on a particular issue. Tax advisers say rebates are generally considered to be a reduction in purchase price, and not likely to be taxed. Rebates on purchases made for business or investment may have more complex treatment, so consult a tax adviser.

In short, the IRS hasn’t said anything specific either way, but has ruled in specific cases that they are not taxable. Although certainly not concrete, this is still reassuring as I personally have never reported any of my cashback as income.

I would estimate I pull in well over $1,000 a year in free money from credit cards, with my 2 to 5% back on all my purchases as well as signing up for $100 to $250 in upfront incentives. The great thing is that anyone with decent credit can get in on these offers. Article via Boston Gal’s Open Wallet.

Last updated: April 10, 2013

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Deconstructing My 3 Free Credit Reports

Posted on March 26, 2006 // 15 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.For some reason, I felt like I should check all of my credit reports today. I think it was because I knew my new landlord had run our credit, and I also haven’t checked them in a while. Remember, the government mandates that everyone gets 1 free credit report (but not score) every year from each of the 3 credit bureaus at AnnualCreditReport.com. You can get all three at once, or space it out. I requested all three so I could compare them all side-by-side.

Besides, if I want my credit report again I can always go to sites like Credit.com and get one free with a trial subscription. I’ll have to cancel within 30 days or get charged something, but you get the credit report instantly, so why wait 30 days? I usually cancel the same or very next day! Another bonus is that you can also get your credit score for free as well, which is usually $8 everywhere else.

[Read more…]

Last updated: March 14, 2014

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

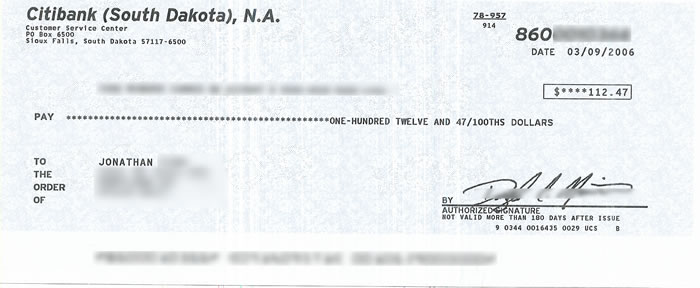

Citibank Doesn’t Hate Me.

Posted on March 21, 2006 // 18 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.I guess Citibank doesn’t hate me as much as I thought they did. I just received my cashback check for $112.47, right on time:

You gotta love getting over $100 in free money just for pumping gas and buying groceries!

Last updated: August 5, 2006

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Citibank Must Hate Me.

Posted on March 8, 2006 // 31 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.I noticed that I was over $100 in rebates for my Citi Dividend Platinum Card, so I just requested a nice fat check for $112.47. More free money!

I honestly think that, second to deadbeats, I may be the most unprofitable customer that Citibank has. I use their no-fee 0% balance transfer offers with glee, I take their $100 sign-up bonuses and run, and I only use their 5% cash back card for the stuff that gives me 5% cash back (gas, groceries, and some gift cards) and nothing else. I’m well over the $1,000 mark in free money from them, and I’m still going!

Last updated: March 13, 2014

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

More Credit Card Debt, Here I Come!

Posted on February 26, 2006 // 42 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.I’ve decided to continue my somewhat controversial practice of borrowing cash from credit cards and profiting by earning interest off of it. As I’ve already got my $100 gift card from my Citi Professional Card with ThankYou Network, I’m going to use the no balance transfer fee 0% APR offer also included with it to take out $9,000 free for 9 months. I figure I can put it in a bank account earning at least 4.5% APR, so that would be about $300 profit pre-tax. This will join the $20,000 in borrowed money that I already have out.

For those interested, please see the following posts which detail how I go about doing this, see my very detailed series on How To Make Money From 0% APR Balance Transfers.

Please read through those posts and the comments before yelling at me! =) Your concerns are most likely already voiced, and my response already jotted down. I’ve been doing this for years and I’ve heard it all. Yes, there are some dangers. Here’s a good rule of thumb: If you’ve missed a credit card payment deadline within the last year, doing this may not be a good idea. The simple truth is that I have personally decided that it is worth the risk for me. Why do I bother? Moola. Dough. Bling. A quick and dirty example:

If you have good credit, you can borrow $30,000 for 12 months with no fees (use one of the offers listed above). $30,000 x 4.5% = $1,350. Even after taxes, I’m looking at over a grand of free money. As usual it took me way less time to request my check than it did to write this post.

Last updated: April 29, 2014

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Citi mtvU Card – 5% Back At Restaurants and Amazon.com

Posted on February 20, 2006 // 9 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.I forgot about this card – The Citi mtvU Platinum Select Visa Card is a credit cards for college students, that offers an interested array of perks. Like the Citi Professional Card, it is part of the Citi ThankYou Network. The card gives you 5 ThankYou Points for every dollar you spend at restaurants, bookstores, record stores, movie theaters and video rental stores. But guess what is considered a bookstore, no matter what you buy? Amazon.com! This is the same as 5% back in gift cards or 5% cash back towards your student loans.

The only problem is that there are reports that they verify if you are a student. Some get asked, many slip by. If you are a student, you also get some points for having good grades: “250 to 2,000 ThankYou Points? twice a year for a good GPA. 25 ThankYou Points? a month for paying your bill on time and not going over your credit limit.” So get a 4.0 and pay your bills and get $43 for free every year! There’s no annual fee and even no minimum income or cosigner requirement. I bet anyone under 25 gets approved for this automatically. I’m over but hey, I’m a student now 😉

Last updated: January 28, 2013

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)