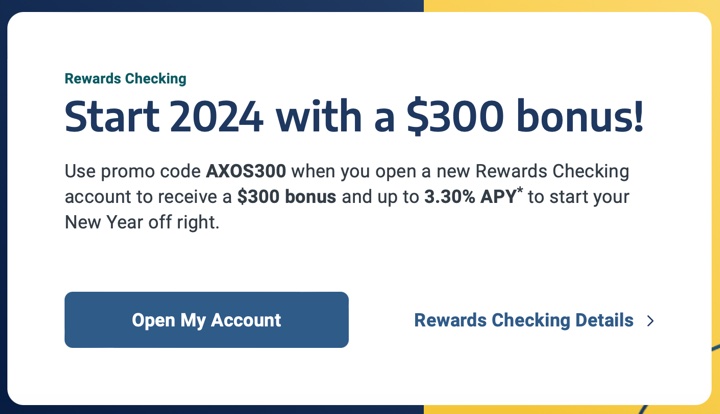

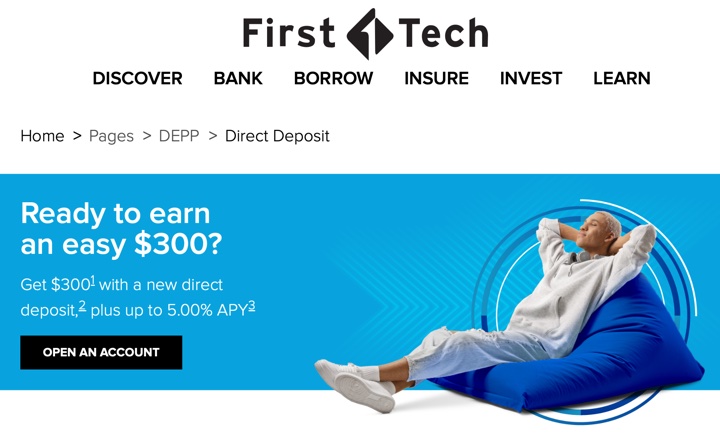

Updated with new offer. Axos Bank has a $300 bonus with relatively straightforward requirements using promo code FREEDOM300. You must open a new Cashback Checking account by 7/31/2024 and fund within 30 days of account opening. Set up direct deposit of $1,000+ each calendar month, and that will earn you $100 per month for 3 months ($300 total). Historically, they have been pretty flexible on what is considered direct deposit.

The fine print:

To be eligible to earn all or a portion of the cash incentive as part of the “FREEDOM300″ $300 promotion, an Axos Bank CashBack Checking account that includes the promotional code ” FREEDOM300″ must be opened between November 1, 2023, at 12 a.m. PST and July 31, 2024, at 11:59 p.m. PST. Axos Bank reserves the right to limit each primary account holder to one (1) checking account promotional offer per year, and customers who have held primary ownership of an Axos Bank or Axos Bank for Nationwide checking account at any time in the past 12 months may be disqualified from the “FREEDOM300” offer. Promotional terms and conditions are subject to change or removal without notice. Bonus cash may be taxable and reported on IRS Form 1099-MISC. Consult your tax advisor. After meeting the initial requirements mentioned above, the amount of cash bonus earned will depend on meeting the additional requirements outlined below:

To earn up to a $300 bonus, you must be approved for your new Axos Bank CashBack Checking account, fund it within 30 days of account opening, and have qualifying direct deposits that total at least $1,000.00 each calendar month. A cash bonus of up to $300 can be earned in the following manner during the first four (4) statement cycles. A statement cycle is a calendar month consisting of the days your account was open during that month. A maximum of three (3) payouts of $100 for each calendar month that the CashBack Checking account is receiving the direct deposit requirement, the bonus can be earned during the first four (4) statement cycles, and the bonus will be deposited into your Axos Bank CashBack Checking account within 10 business days following the end of the statement cycle in which the direct deposit requirement was met. Your Axos Bank CashBack Checking account must be open and in good standing at the time the bonus is paid to be eligible to receive the bonus, and your Axos Bank CashBack Checking account must remain open for 120 days, or an early closure fee of up to $300 may apply, equal to the amount of the total bonus earned up to $300.

I’ve done a few Axos Bank bonuses in the past (too recent for me to qualify for this), and the good news is that they do pay out reliably in my experience.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)