I was catching up on some blog reading and caught an old post from Plonkee about the different ways that couples can manage their finances. The three different methods were categorized as communist, socialist, or capitalist. Rather controversial, eh? Don’t get too excited folks, just read on:

I was catching up on some blog reading and caught an old post from Plonkee about the different ways that couples can manage their finances. The three different methods were categorized as communist, socialist, or capitalist. Rather controversial, eh? Don’t get too excited folks, just read on:

Communist: One Big Pot

According to Wikipedia, communism is a social structure in which classes are abolished and property is commonly controlled. Thus, no matter what each person earns, all their income is deposited into one central joint account, from which all expenses are paid from as well. All assets including property, investments, and cash are owned together.

Socialist: Earn More, Pay More

Under this structure, common shared expenses such as rent and utilities are paid via a joint account. Let’s say one person makes $75k and the other person makes $25k. Then if the monthly shared expenses are $1,000 per month, they would pay $750 and $250 respectively. The contribution is proportional to income.

Separate expenses such as entertainment, gifts, or clothing are paid for out of personal accounts. This allows each person to retain some individual control of their money.

Capitalist: You Pay Yours, and I’ll Pay Mine

Finally, we have the option where purely shared expenses are simply split straight down the middle. Differing income levels don’t change anything; If you make more then you keep more. Everything else is paid directly by each individual. Theoretically, each person is thus incentivized to keep their own expenses down, as nobody else helps to pay for it. There is “my money” and “your money”. This is often how platonic roommates manage their finances.

Just Call Me Karl

Although I usually don’t align myself as communist, I must admit that that is mostly how we manage our money as a married couple. It’s also helpful that we both work and earn comparable incomes (a least for now). We do add in a small “adult allowance” fund where we can spend money on whatever with no questions asked. Besides that, while we definitely don’t always agree on things, I think the combination of open communication and the passage of time has gotten us relatively comfortable with the “one pot” setup.

Now, I don’t think any one type is necessary better than the other, and know couples of each persuasion. I do have one question for the capitalist-types, though: What about retirement? Do you split that too? What happens if one person doesn’t invest adequately in retirement?

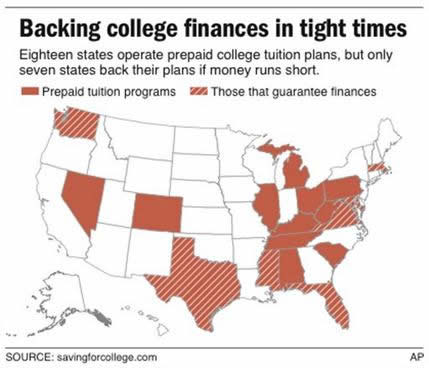

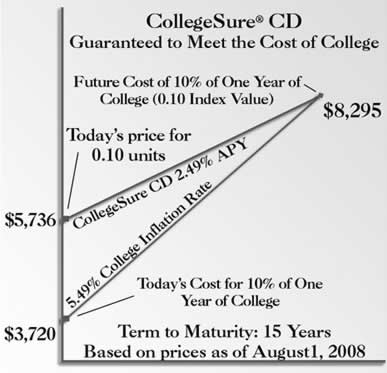

On December 1st, Fidelity Investments made significant reductions to the management fees on the 529 college savings plans that they manage. From this AP article:

On December 1st, Fidelity Investments made significant reductions to the management fees on the 529 college savings plans that they manage. From this AP article:

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)