I just wanted to take a moment and thank you for reading My Money Blog. I am grateful for your time and attention and hope that I provided something of value in exchange. I hope that your year has been bountiful and that you have enjoyed both success in your finances and the other critical components of wellness – healthy mind, healthy body, and healthy relationships. I hope that you find time this holiday period to appreciate all the hard work you and your family put forth this year. I forgot to budget for a fancy Christmas card graphic, so here are some artfully-decorated cookies from my kids:

(I might have eaten a jelly bean. Shhh.)

Some close friends of ours are having their first baby at the same time that our third (and last!) kid is turning 2. That means we’ll be passing along a bunch of stuff and also recommendations. Sometimes I read these buying guides and wonder if the author actually tried it past a 5-minute trial run. We got a lot of items that sounded cool but ended up collecting dust. Other stuff we didn’t think would be useful but quickly became daily essentials through 3 babies over 6 years.

Some close friends of ours are having their first baby at the same time that our third (and last!) kid is turning 2. That means we’ll be passing along a bunch of stuff and also recommendations. Sometimes I read these buying guides and wonder if the author actually tried it past a 5-minute trial run. We got a lot of items that sounded cool but ended up collecting dust. Other stuff we didn’t think would be useful but quickly became daily essentials through 3 babies over 6 years.

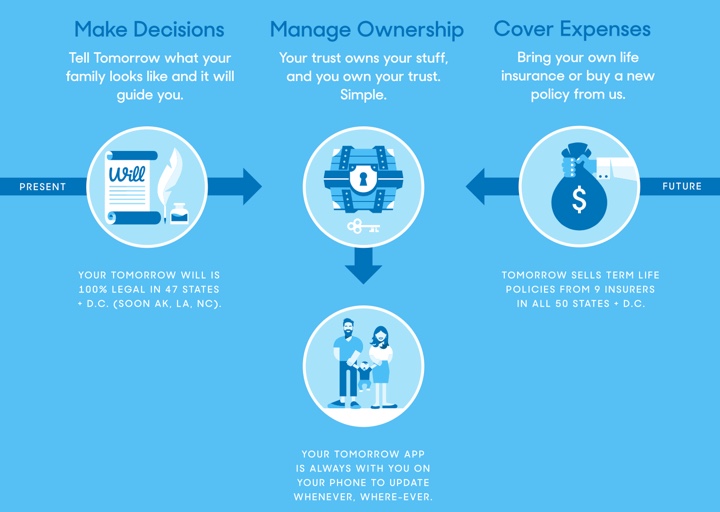

People don’t like talking about money. That’s why I started this site. You know what people like talking about even less? Death.

People don’t like talking about money. That’s why I started this site. You know what people like talking about even less? Death. I’m turning 40 years old this summer. This number has always been a psychological marker for me. I’ve always wanted to be financially secure and have started a family by age 40. According to this

I’m turning 40 years old this summer. This number has always been a psychological marker for me. I’ve always wanted to be financially secure and have started a family by age 40. According to this

We’re in the midst of an extended Spring Break vacation, so posting will be light for the next two weeks. I have some pre-written content scheduled, but the comment moderation may be delayed.

We’re in the midst of an extended Spring Break vacation, so posting will be light for the next two weeks. I have some pre-written content scheduled, but the comment moderation may be delayed. While reading the

While reading the  It’s kind of sad when you hear the term “Black Friday Week” more often than Thanksgiving. I would like to interrupt the flow of deals to briefly connect personal finance and Thanksgiving in a different way. Seth Godin has put together something called the

It’s kind of sad when you hear the term “Black Friday Week” more often than Thanksgiving. I would like to interrupt the flow of deals to briefly connect personal finance and Thanksgiving in a different way. Seth Godin has put together something called the

The newly-launched

The newly-launched

I’ve been told that my blog isn’t personal enough. Father’s Day seemed like an appropriate time to share how our efforts towards financial freedom have altered our day-to-day lives.

I’ve been told that my blog isn’t personal enough. Father’s Day seemed like an appropriate time to share how our efforts towards financial freedom have altered our day-to-day lives.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)