Update April 2017. It appears that the same people behind the website mentioned below have created another nearly-identical website. Even if you opted-out last time, all of your sensitive personal information is up again on this website. You must opt-out again by clicking on “Privacy” at the bottom and then the “record removal link” (alternatively, try this) and then following the directions. This one allows reverse address and phone lookups as well.

Original post:

If you don’t like the idea of anyone being able to look up your address history and the names of all your relatives, you may want to enter your name into this website. Depending on the information it has gathered on your from public records, it may list personal information about you such as:

- Your current and past addresses.

- Names and birth years of your parents, siblings, cousins, and in-laws.

- All of their current and past addresses.

- Any variations of your name ever used.

While all of this information is technically in the public domain, I don’t know of any other website that has it organized in such an accessible manner that is both free and does not require any registration. The website was so detailed that it included addresses that even I had forgotten about, as well as name of relatives that I barely know (which is the intended upside, I suppose). I’m more worried about the downside.

The good news is that the website will delete your information upon request. First, you may want to save whatever information they collected about you into a PDF. Next, I would try visiting this opt-out link directly and following the directions carefully. Alternatively, you can follow the opt-out instructions in this Time article. It only takes a minute, and my name record was removed within 48 hours as promised. Found via Bogleheads.

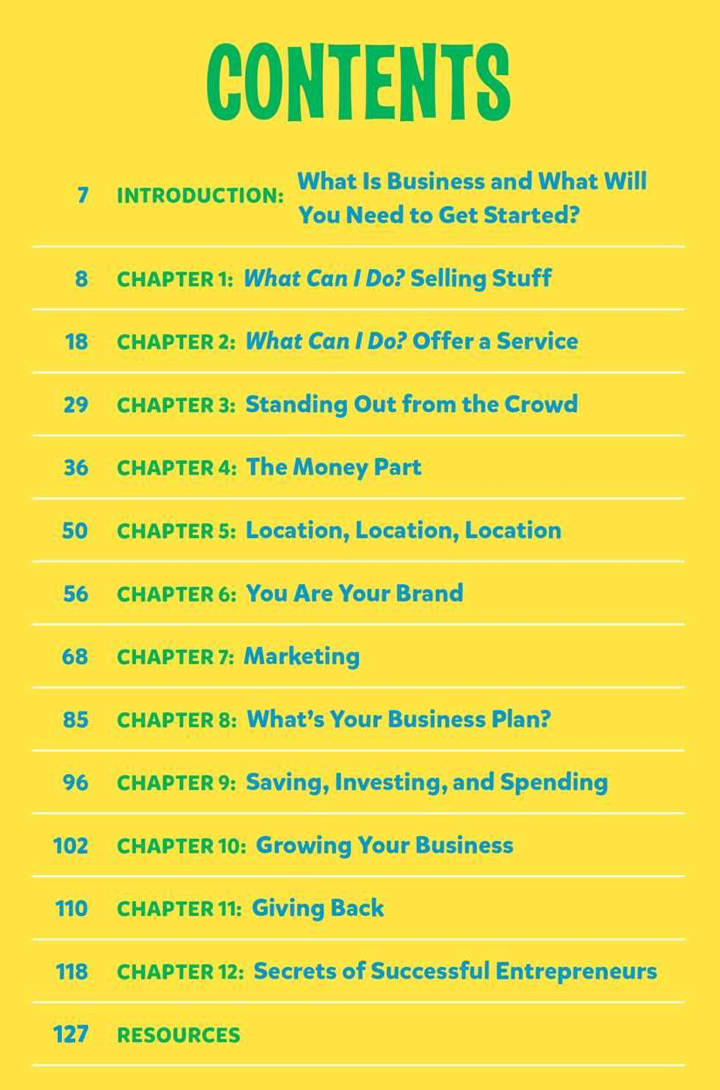

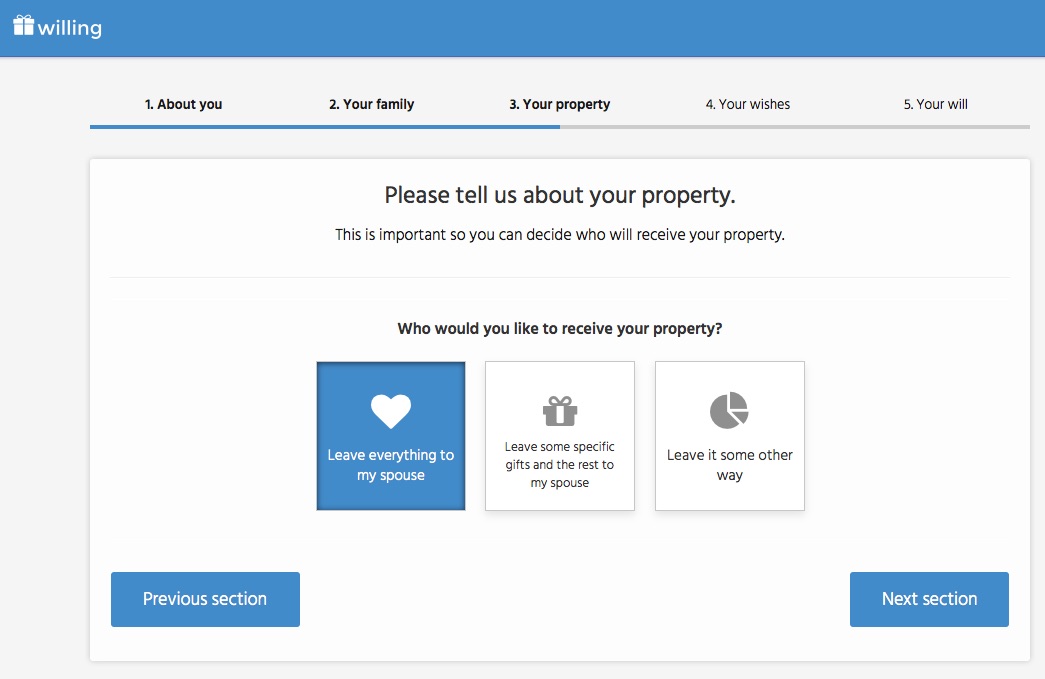

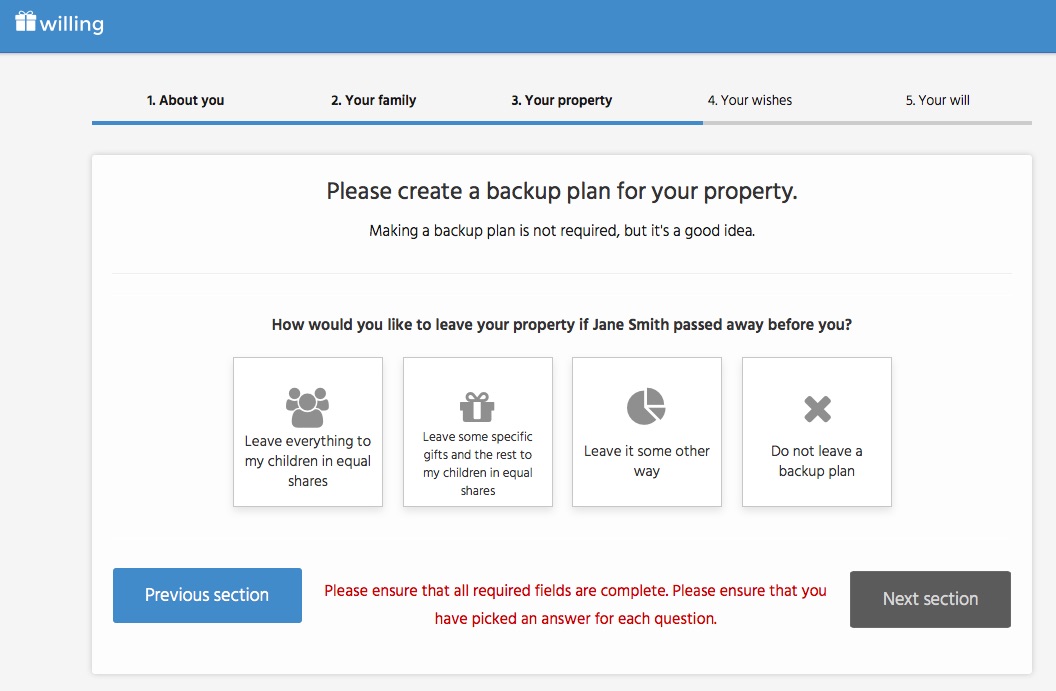

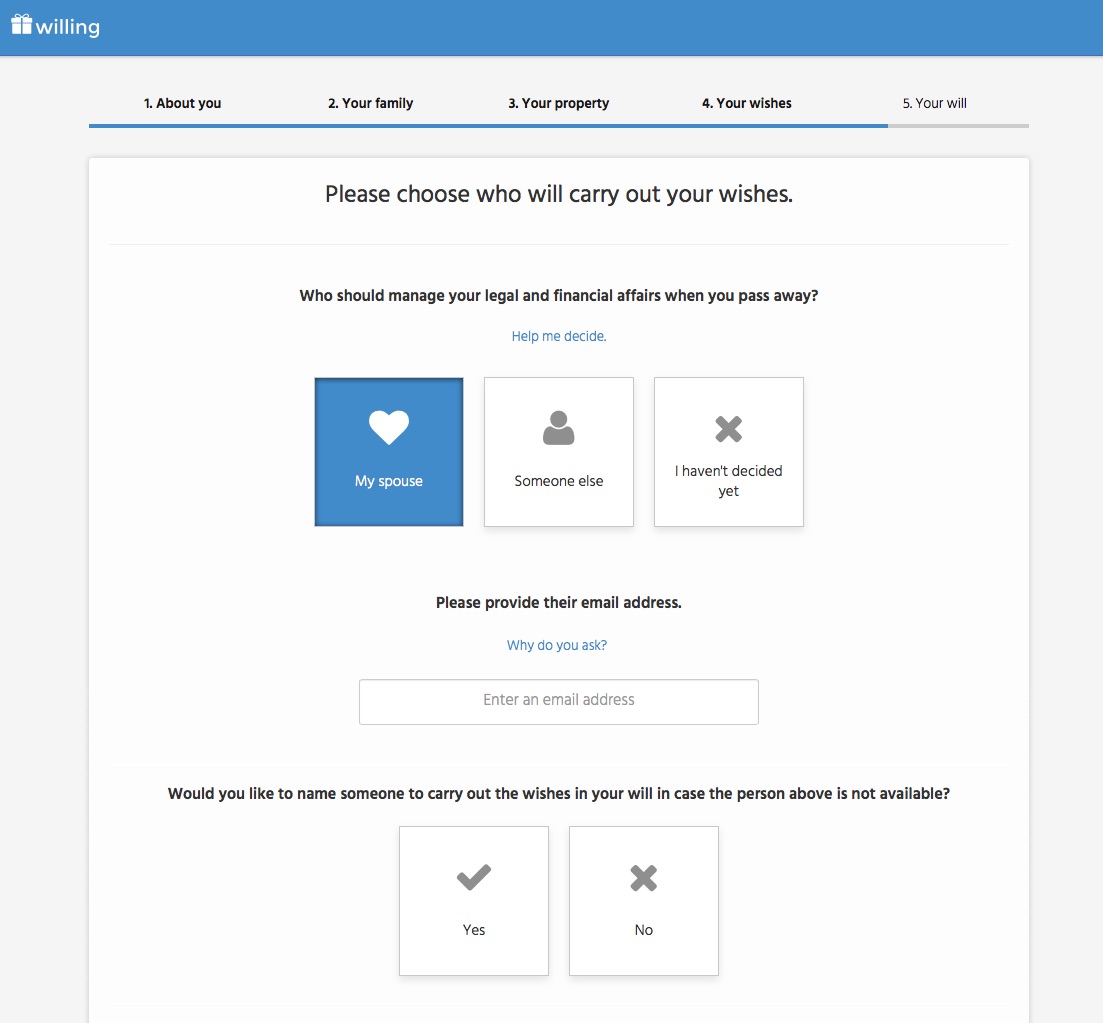

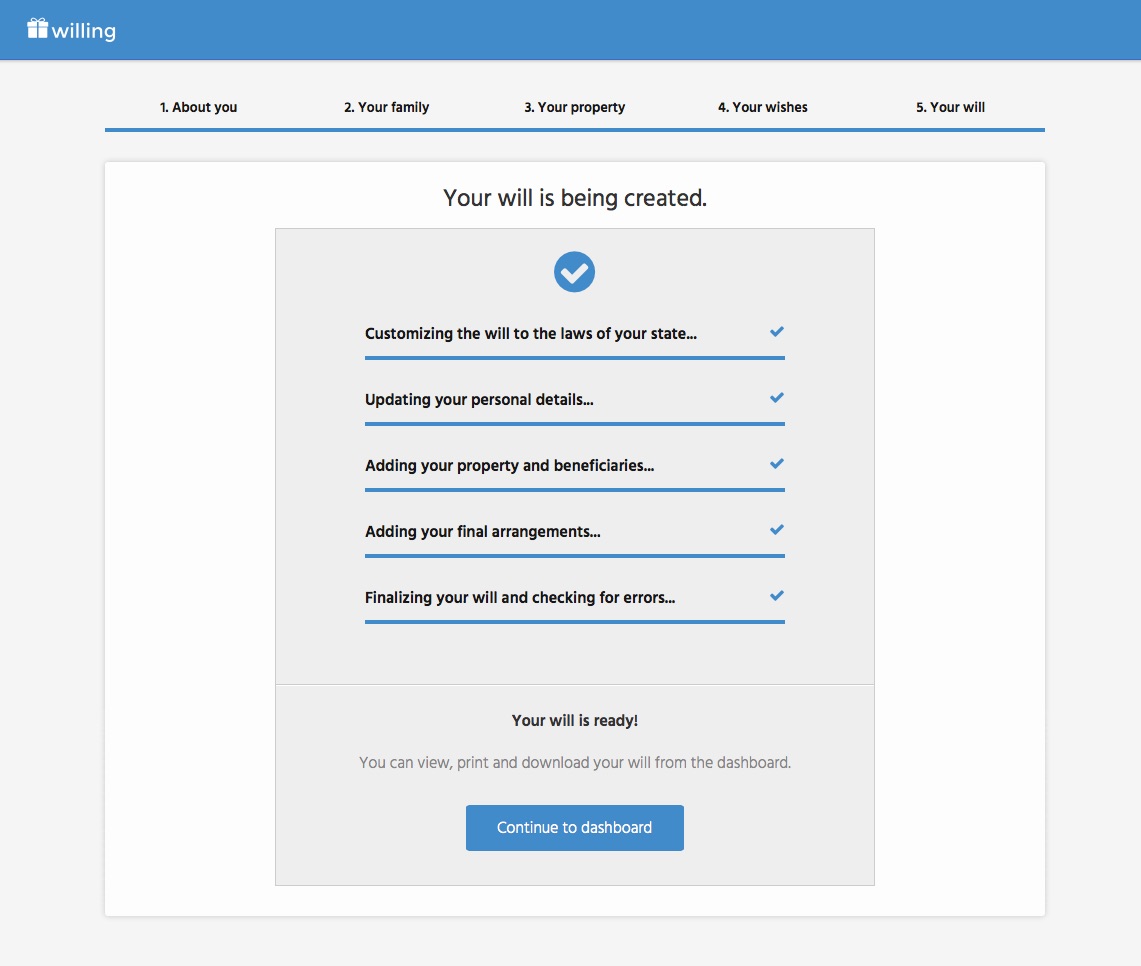

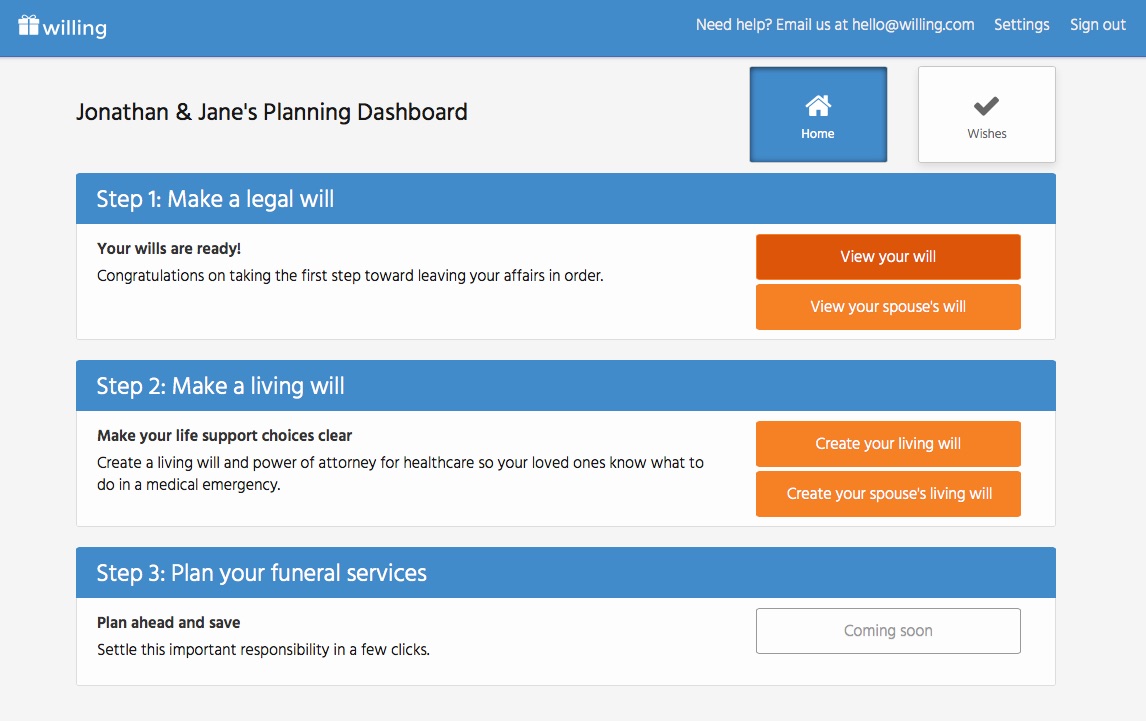

If one of your New Year’s Resolutions is to create an estate plan for you and your loved ones, here’s a good starter kit. The American Red Cross has a free Estate Planning Guide and Workbook which comes in both electronic fillable PDF form or a paper workbook format if you give them your address. It is roughly 50 pages and includes blanks to store your asset and beneficiary information, make future edits when needed, and print multiple copies to share with your attorney and family members. The guide will help you to:

If one of your New Year’s Resolutions is to create an estate plan for you and your loved ones, here’s a good starter kit. The American Red Cross has a free Estate Planning Guide and Workbook which comes in both electronic fillable PDF form or a paper workbook format if you give them your address. It is roughly 50 pages and includes blanks to store your asset and beneficiary information, make future edits when needed, and print multiple copies to share with your attorney and family members. The guide will help you to:

Do you let your kids create the memories of Trick-or-Treating but not the subsequent cavities from actually eating all that candy? A nationwide network of over 2,500 dentists will buy back your Halloween candy (usually for $1 per pound, up to 5 pounds) at

Do you let your kids create the memories of Trick-or-Treating but not the subsequent cavities from actually eating all that candy? A nationwide network of over 2,500 dentists will buy back your Halloween candy (usually for $1 per pound, up to 5 pounds) at  The NY Times has a new essay called

The NY Times has a new essay called

We are currently planning a 4-week European trip with our young children (age 1 and 3). The most common reactions are “Cool. Wait, you’re not bringing the kids, are you?” followed by “You’re nuts.” At first, we didn’t think it could be done either. It does take a lot of additional planning for car seats, cribs, kid-friendly itineraries, and so on.

We are currently planning a 4-week European trip with our young children (age 1 and 3). The most common reactions are “Cool. Wait, you’re not bringing the kids, are you?” followed by “You’re nuts.” At first, we didn’t think it could be done either. It does take a lot of additional planning for car seats, cribs, kid-friendly itineraries, and so on.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)