A financial topic that nearly everyone has an opinion on is car ownership. Do you buy new and drive it into the ground? Do you buy slightly used after the early depreciation hit? Do you buy a cheaper 10-year-old car, drive it for a while, sell it for not much less, and repeat?

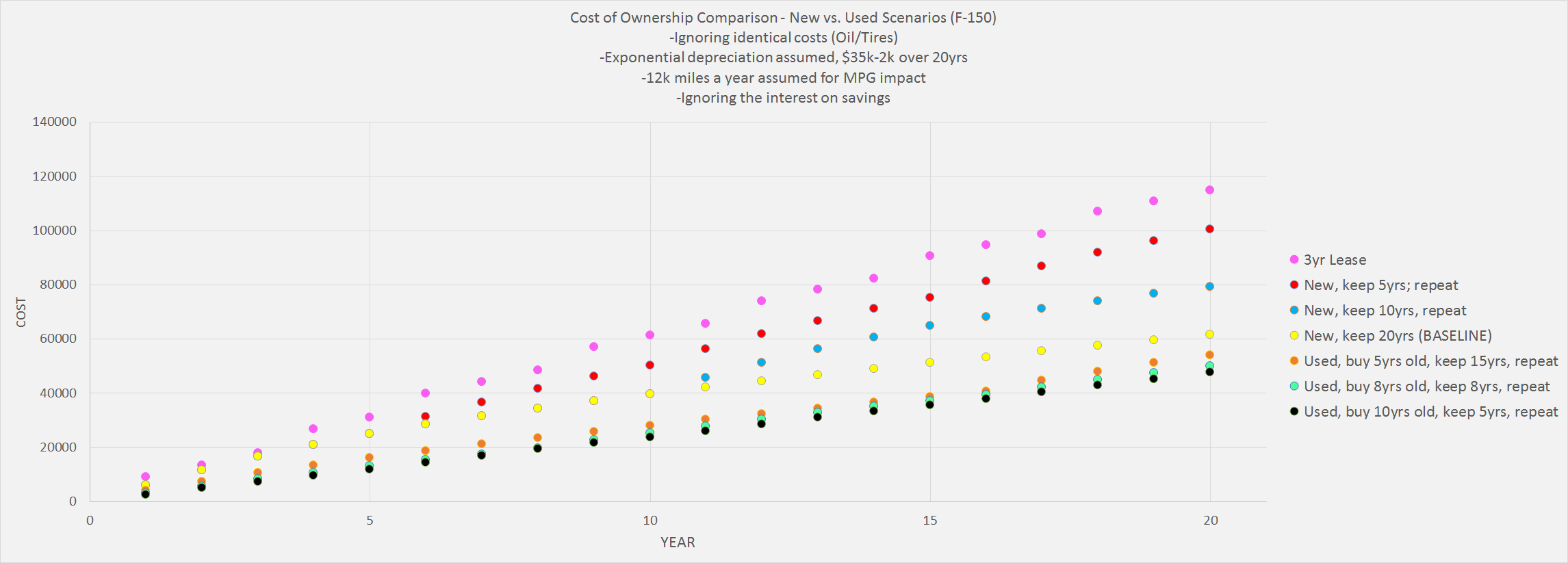

Reddit user nmtxinsc2 put together an interesting car cost comparison of the total cost of ownership for these options and more. Here is the final graphic, which you should click to enlarge:

Assumptions. These are not based on average or historical car values, but from a theoretical cost model for a single car. A quick overview:

- Car Value. New price $32,000. Value depreciates exponentially down to $2,000 after 20 year lifespan. The historical depreciation behavior of a Ford F-150 is a general benchmark.

- Maintenance. From $0 to $800 over lifespan.

- Insurance. From $742 to $300 over lifespan.

- Fuel efficiency. MPG goes from 25 to 16 over lifespan. 12,000 miles a year at $2.50 a gallon.

Don’t agree? You can download the source spreadsheet and adjust any of the assumptions yourself.

Observations. It’s not surprising that leasing a brand-new car every 3 years is the most expensive, or that buying a 10-year used car and keeping it for a while is the least expensive. However, it may interest you that the calculations show that, for example:

- You would save ~$68,000 over 20 years if you Buy 10-year-old Used Car/Keep 5 years instead of always doing 3-year New Leases.

- You would save ~$20,000 over 20 years if you Buy New/Keep 10 years instead of Buy new/Keep 5 years.

- You would save ~$8,000 over 20 years if you Buy 5-year-old Used Car/Keep 15 years instead of Buy New/Keep 20 years.

My own thoughts on managing car costs. I like reading about models and statistics like this. However, my rule of thumb on affordability is more simple and behaviorally-based. If you want to achieve early retirement, you should only pay cash for cars. In my opinion, car debt and credit card debt are equally harmful to your financial health. In fact, auto loans may be worse – many can garnish your wages even after the car is repossessed. Financing obscures the real cost. When you’re faced with writing a huge check for $20,000 or whatever, your decision-making clarity is greatly improved.

I enjoyed reading this NYT article

I enjoyed reading this NYT article

The

The

Ting Mobile has a free

Ting Mobile has a free

A while back I did a post on

A while back I did a post on

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)