Consumer Reports recently released the results from their 2015 Annual Auto Reliability Survey of over 740,000 vehicles owned by its subscribers. Below are the complete rankings from Consumer Reports, including the change from last year. Taken from this CNBC article. Lexus and Toyota remain on top. In terms of big movers, Honda went down 4 spots, while Kia moved up 4 spots.

Consumer Reports recently released the results from their 2015 Annual Auto Reliability Survey of over 740,000 vehicles owned by its subscribers. Below are the complete rankings from Consumer Reports, including the change from last year. Taken from this CNBC article. Lexus and Toyota remain on top. In terms of big movers, Honda went down 4 spots, while Kia moved up 4 spots.

One of the trends they note is that fancy infotainment systems and complex transmissions (including CVT, 8+ speeds, and dual clutch) are a growing source of complaints. Many brands, including Acura, were significantly hurt in their rankings due to issues in these areas.

Here’s another view that takes into account the range of scores taken from individual models (the brands are ranked by averages). Taken from the public version of the Consumer Reports page.

Jaguar, Land Rover, Mitsubishi, Scion, Smart, and Tesla were excluded due to a lack of data on two or more of their models. However, Tesla’s Model S was individually given a reliability rating of “below average”.

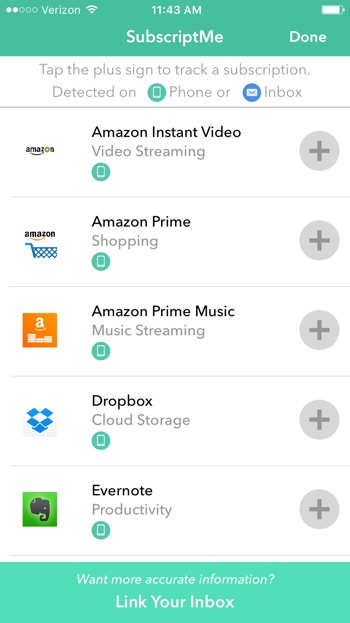

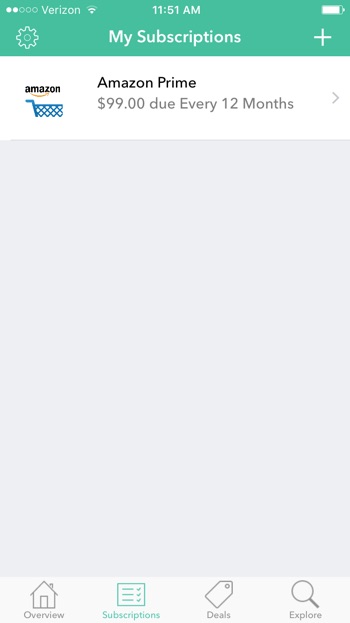

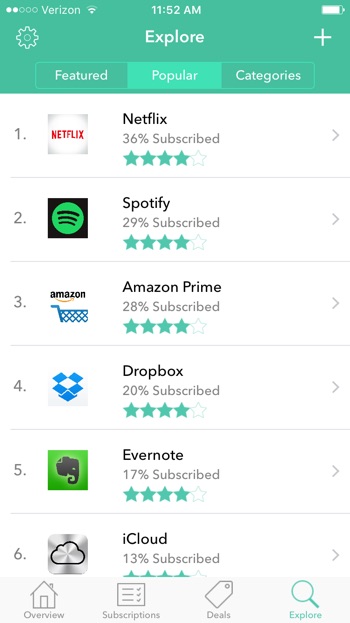

I usually don’t upgrade my iPhone to the latest OS right away, as you know there is going to be 9.0.1 and 9.0.2 and so on in the upcoming weeks. But since the

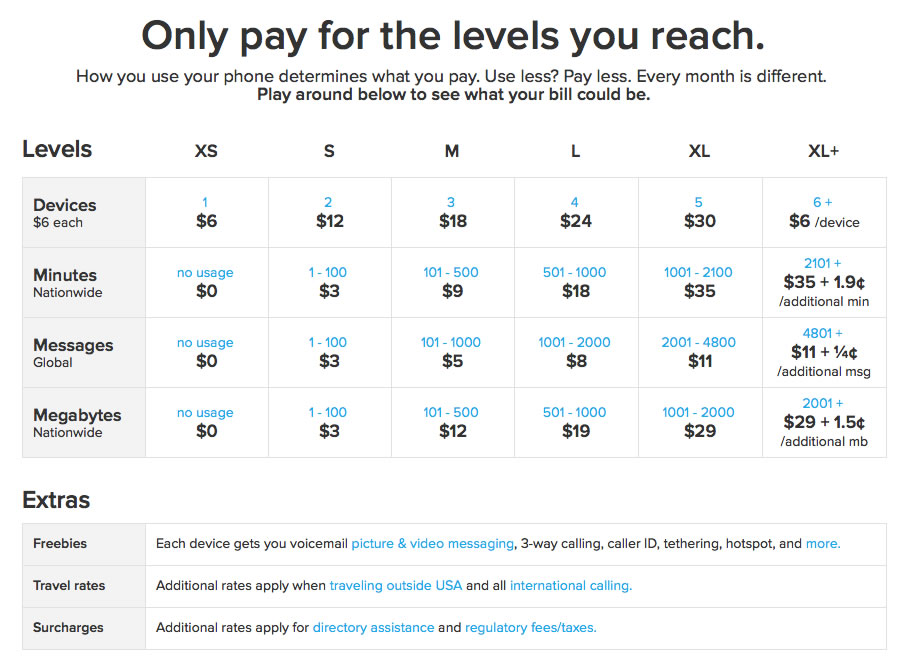

I usually don’t upgrade my iPhone to the latest OS right away, as you know there is going to be 9.0.1 and 9.0.2 and so on in the upcoming weeks. But since the  Ting provides mobile phone service with a “pay-only-for-what-you-use” structure. While their classic program required Sprint phones, their newer GSM program is compatible with nearly any phone that takes GSM sim cards. Supposedly 80% of smartphones now work with GSM service and have SIM card slots. My old Verizon iPhone 5 was GSM unlocked. Their GSM SIM card service uses the T-Mobile GSM MVNO network.

Ting provides mobile phone service with a “pay-only-for-what-you-use” structure. While their classic program required Sprint phones, their newer GSM program is compatible with nearly any phone that takes GSM sim cards. Supposedly 80% of smartphones now work with GSM service and have SIM card slots. My old Verizon iPhone 5 was GSM unlocked. Their GSM SIM card service uses the T-Mobile GSM MVNO network.

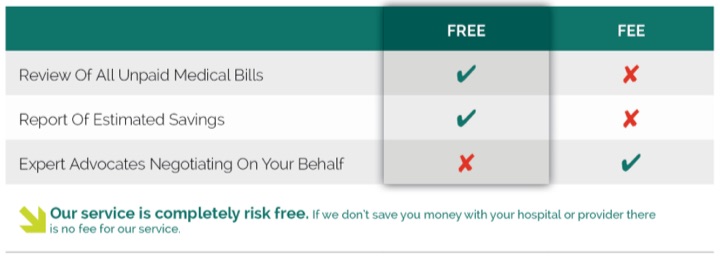

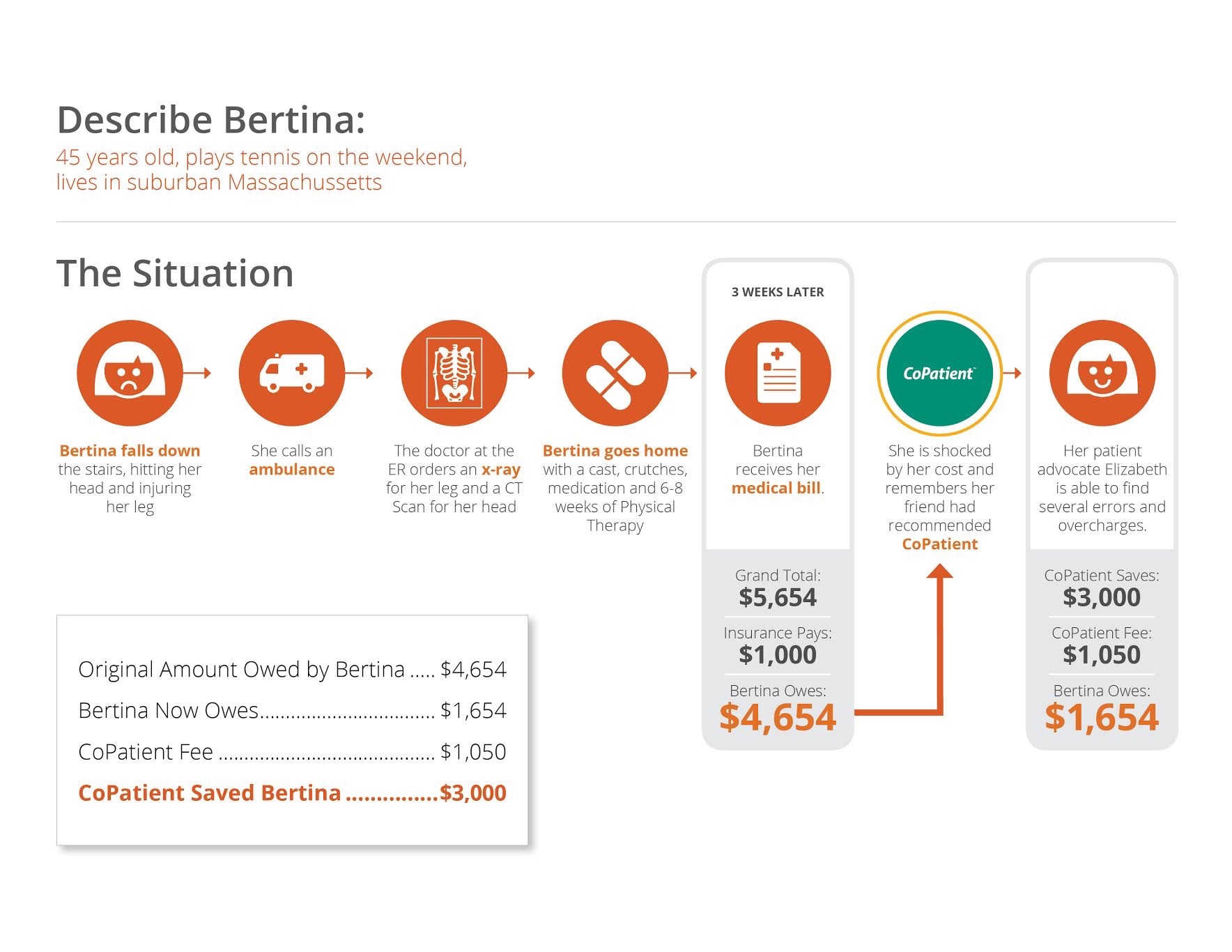

High-deductible health plans are still growing in popularity. While these can be a great way to save on your monthly premiums, it also means that when you do have to visit the emergency room, you get to tackle nearly the entire bill instead of a small co-pay. The problem is that most medical bills cannot be understood by mere mortals. Likely, the doctors and nurses themselves have no clue how that $6,344 bill for a broken arm got generated.

High-deductible health plans are still growing in popularity. While these can be a great way to save on your monthly premiums, it also means that when you do have to visit the emergency room, you get to tackle nearly the entire bill instead of a small co-pay. The problem is that most medical bills cannot be understood by mere mortals. Likely, the doctors and nurses themselves have no clue how that $6,344 bill for a broken arm got generated.

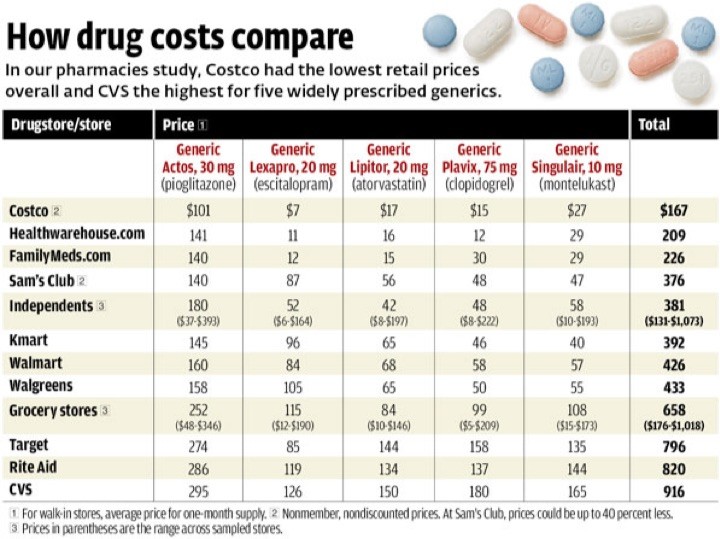

While standing in line at the Costco pharmacy, I found myself in a discussion with another Costco member who apparently saves over a thousand dollars a year on her meds by buying them there instead of her neighborhood CVS. (I also got an earful about the Medicare Part D “

While standing in line at the Costco pharmacy, I found myself in a discussion with another Costco member who apparently saves over a thousand dollars a year on her meds by buying them there instead of her neighborhood CVS. (I also got an earful about the Medicare Part D “

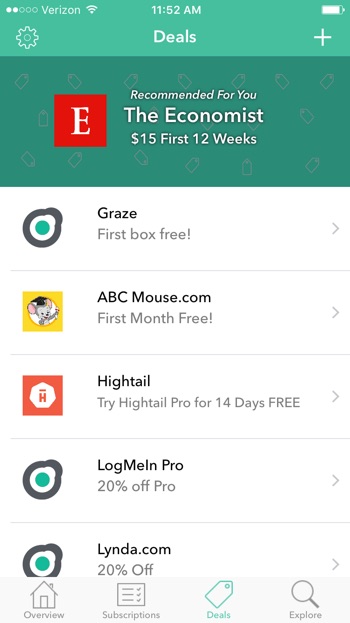

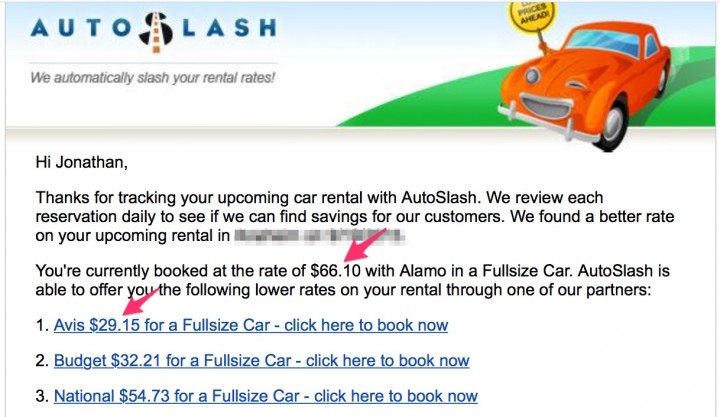

Here’s a quick tip that I’ve been using regularly this summer for saving money on car rentals.

Here’s a quick tip that I’ve been using regularly this summer for saving money on car rentals.

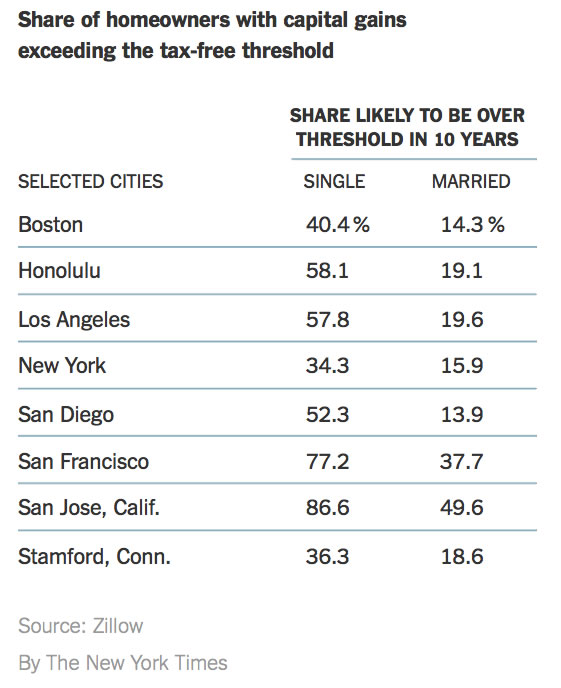

For many people, when they sell a home they don’t even consider taxes. But over time, especially if you live in a relatively expensive area, more and more people will bump up against the federal capital gains exclusions of $250,000 for individuals and $500,000 for couples. (You must have lived in the home for at least two out of the five years before the sale.)

For many people, when they sell a home they don’t even consider taxes. But over time, especially if you live in a relatively expensive area, more and more people will bump up against the federal capital gains exclusions of $250,000 for individuals and $500,000 for couples. (You must have lived in the home for at least two out of the five years before the sale.)

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

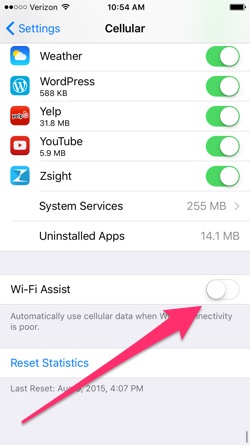

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work){kind=link}