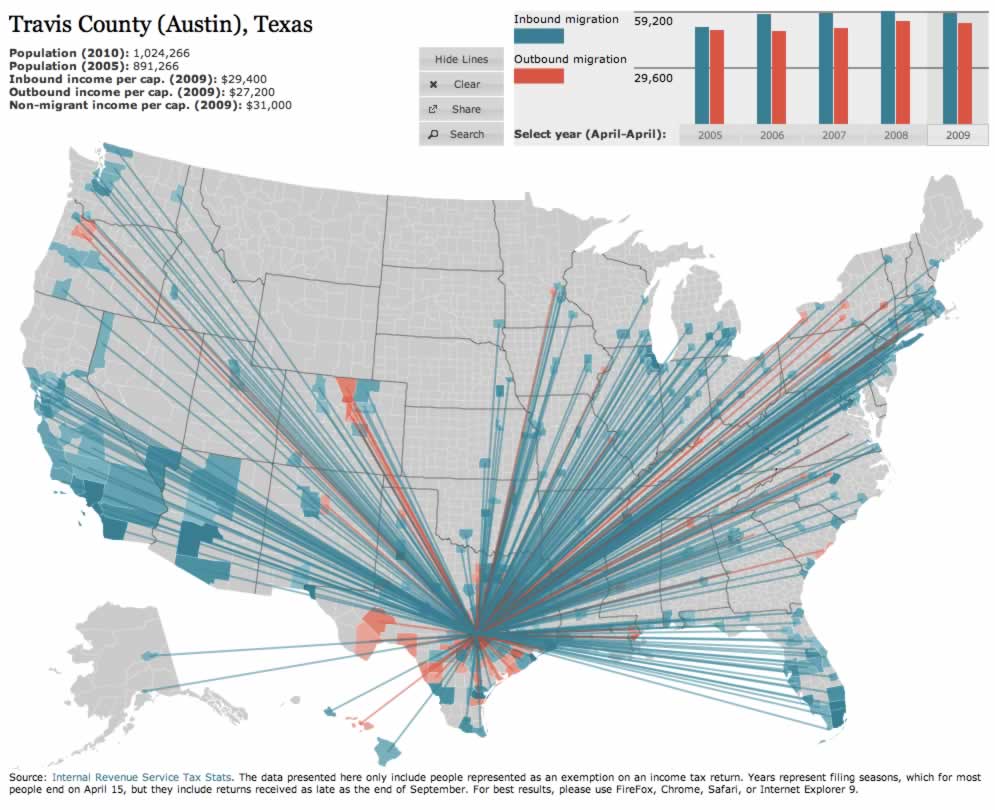

Have you moved for financial reasons?

Have you moved for financial reasons?

Where did you move to? Where did you move from? How did you decide?

Larger income? Better job for similar income? Lower housing costs? Something else?

Share your story in the comments below!

I don’t think there will be as many as the 358 replies to my six-figure salary stories request, but I’m sure reading your case studies would be very interesting.

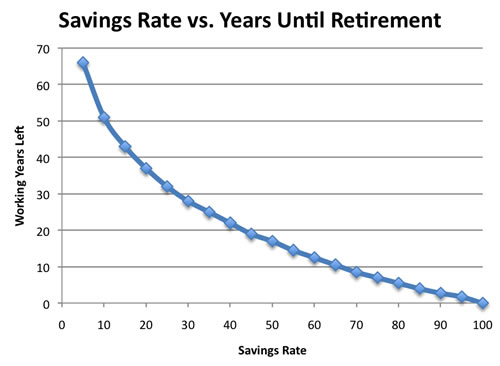

One of my overall goals for 2012 is to make this site more of a permanent resource for information. As part of this, I want to create an “Expense Reduction Guide” that will provide an organized way to find ways to maximize personal value and make your spending efficient.

One of my overall goals for 2012 is to make this site more of a permanent resource for information. As part of this, I want to create an “Expense Reduction Guide” that will provide an organized way to find ways to maximize personal value and make your spending efficient. The Daily Beast has an article

The Daily Beast has an article

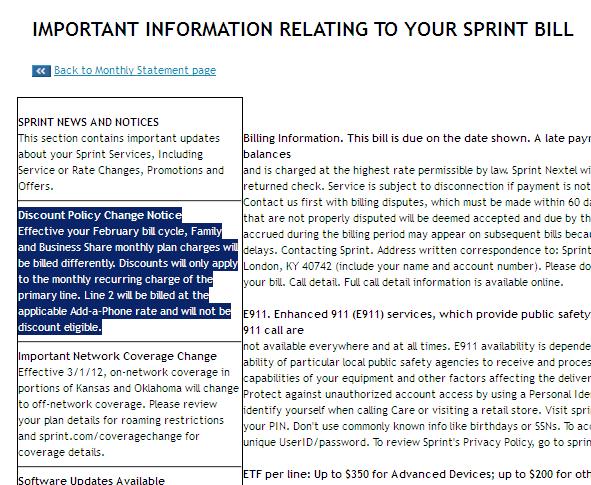

If you’re the person in your family or circle of friends that always seems to be asked computer questions, or are simply the person asking for help, what you really need is software that allows remote access between computers. That way, you can diagnose and fix problems from across the country without having to leave your desk.

If you’re the person in your family or circle of friends that always seems to be asked computer questions, or are simply the person asking for help, what you really need is software that allows remote access between computers. That way, you can diagnose and fix problems from across the country without having to leave your desk.

Updated with current price quotes for 2012!

Updated with current price quotes for 2012!

Not done shopping yet? December 16th (today) is

Not done shopping yet? December 16th (today) is  The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work){kind=link}