Updated with alternative method. My relative lack of travel these days means that I am constantly keeping miles and points from expiring. Here’s the official policy of Hilton Honors point expiration:

Updated with alternative method. My relative lack of travel these days means that I am constantly keeping miles and points from expiring. Here’s the official policy of Hilton Honors point expiration:

Hilton Honors Points do not expire as long as Members remain active in the program. To keep an account active, Members can stay at one of Hilton’s hotels, or earn or redeem Hilton Honors Points within 12 months. [For Hilton Honors credit card holders, Hilton Honors Points will not expire as long as the Member is a cardholder in good standing.]

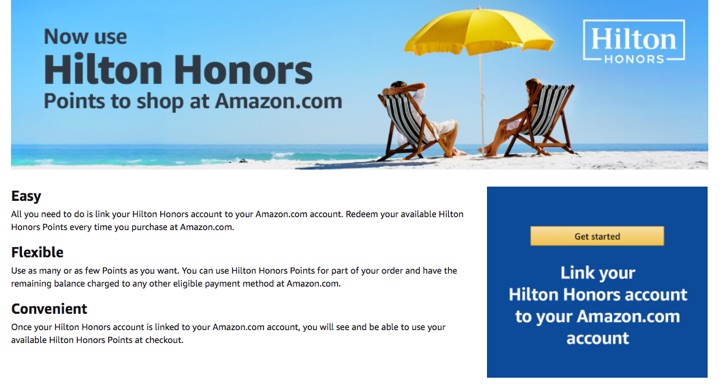

You need to earn or spend Hilton points every 12 months, which is on the short side. My usual strategy is to use Hilton Honors Dining to earn a few points at my neighborhood burger joint, but I was running short on time. I found that you can redeem Hilton points at Amazon through their Shop with Points program. The redemption ratio is 500 Hilton Honors points = $1 on Amazon.

First, link your Hilton Honors account to Amazon.

Next simply use as little as 5 Hilton Honors points to offset $0.01 of any purchase. If you were planing on buying something for $25, just pay for $0.01 with Hilton points, and $24.99 on your credit card. You used to be able to simply buy a $1 Amazon gift code for 500 points and call it a day, but that is no longer an option. If you have Amazon Prime and no other needs, you can still buy one of the following items that cost only $1 or less:

- Taylors of Harrogate Yorkshire Red Teabags (10 count)

- Crayola White Chalk (12 count)

- Ajax Powder Cleanser with Bleach

- Banana Boat Sunscreen for Kids

- Softsoap Liquid Hand Soap

Checkout and choose to pay with Hilton Points, where you can specify to only use as little as 5 points ($0.01). You would want to make sure that it is in stock, so they charge you immediately.

Check for the activity to show up in your Hilton.com account the same day as it is shipped:

Bottom line. If you have Hilton points expiring soon, you can redeem as little as 5 Hilton points for $0.01 off any Amazon purchase and create qualifying activity that posts the same day. If you have Amazon Prime, I share some $1 ideas. Hilton points are more valuable when redeemed for a free hotel night, but in this case it can be worth sacrificing a few to keep the rest alive and active.

Despite the fresh packaging, we should remember that the “FIRE” concept (Financially Independent, Retire Early) is anything but a new concept. Even I can’t help being a little intrigued by the clickbait title “This Secret Trick Let This Couple Retire at 38”. Such an article could have been written about the

Despite the fresh packaging, we should remember that the “FIRE” concept (Financially Independent, Retire Early) is anything but a new concept. Even I can’t help being a little intrigued by the clickbait title “This Secret Trick Let This Couple Retire at 38”. Such an article could have been written about the  After finishing

After finishing

I subscribe to a NY Times e-mail newsletter called

I subscribe to a NY Times e-mail newsletter called

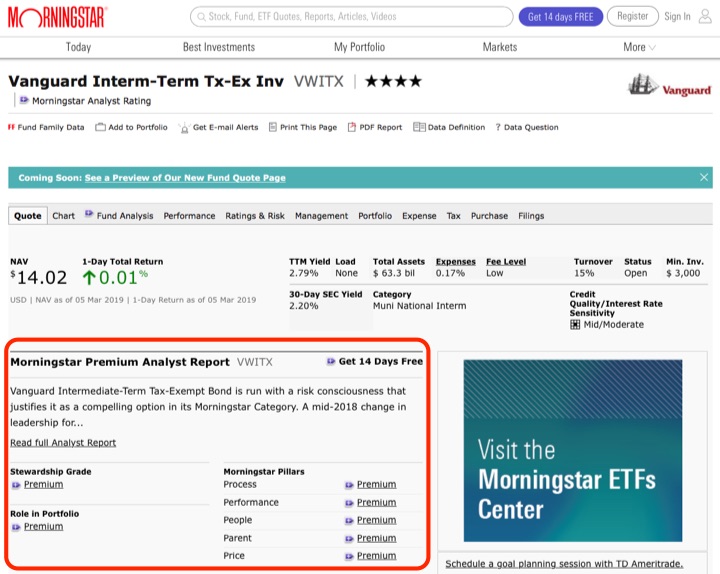

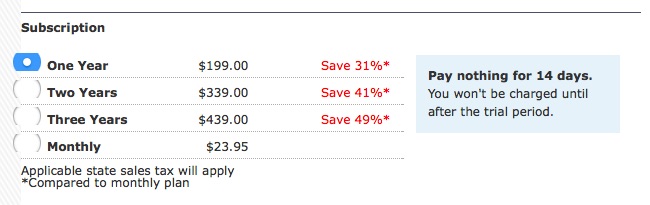

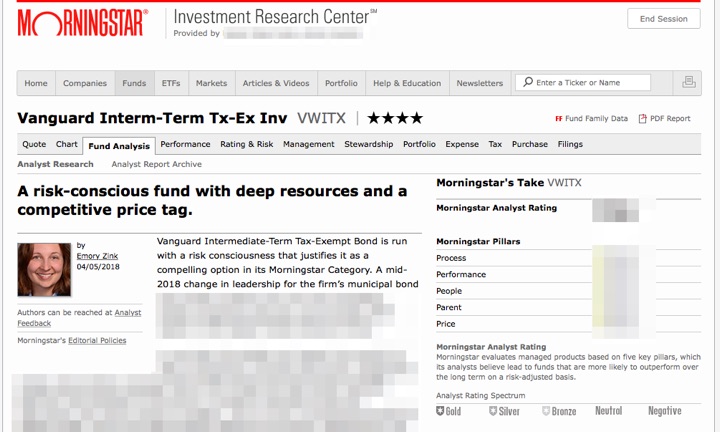

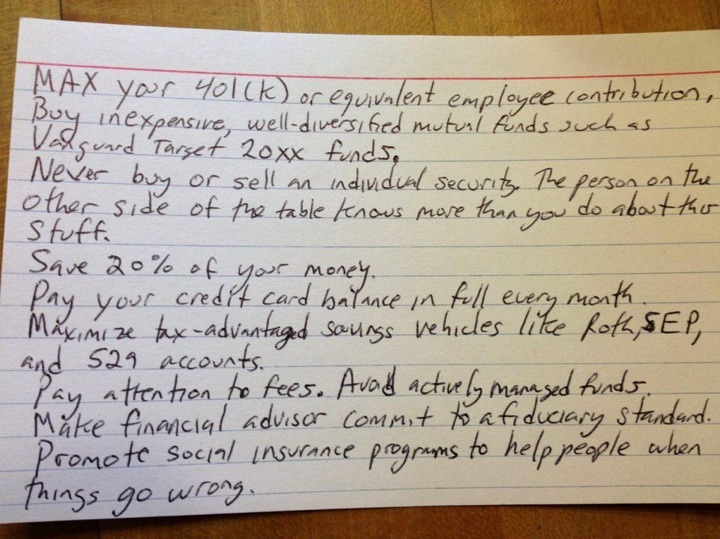

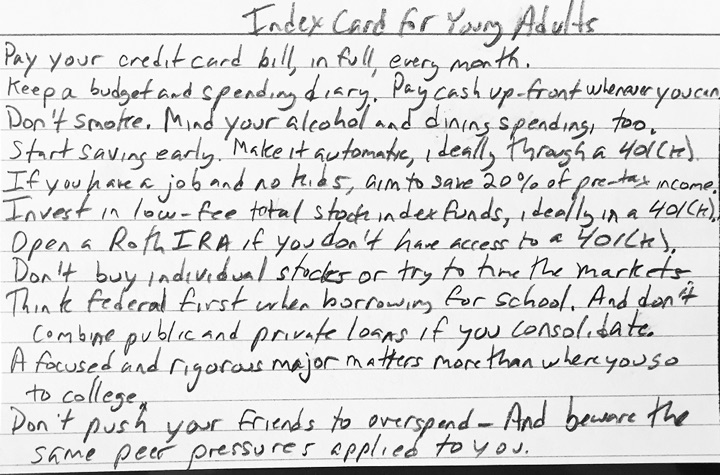

Updated 2019. Let’s say you are a DIY investor and doing some research on some mutual funds. You decide to learn more about the Vanguard Intermediate-Term Tax-Exempt Fund. You pull up the Morningstar quote pages (ticker

Updated 2019. Let’s say you are a DIY investor and doing some research on some mutual funds. You decide to learn more about the Vanguard Intermediate-Term Tax-Exempt Fund. You pull up the Morningstar quote pages (ticker

If you have Amazon Prime, I noticed that the documentary film

If you have Amazon Prime, I noticed that the documentary film

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)