One of the biggest problems in retirement planning is turning a pile of money into a reliable stream of income. I have read hundreds of articles about this topic, and I have not yet found a perfect solution to this problem. Everything has pros and cons: stocks, high-dividend stocks, bonds, annuities, real estate, and so on.

One of the biggest problems in retirement planning is turning a pile of money into a reliable stream of income. I have read hundreds of articles about this topic, and I have not yet found a perfect solution to this problem. Everything has pros and cons: stocks, high-dividend stocks, bonds, annuities, real estate, and so on.

The imperfect (!) solution I chose is to first build a portfolio designed for total return and enough downside protection such that I can hold through an extended downturn. As you will see below, the total income is a little under 3% of the portfolio annually. I could easily crank out a portfolio with a 4% income rate, or even 5% income. But you have to take some additional risks to get there. With a total return-oriented portfolio, I am more confident that the (lower initial) income will grow at least as fast (and hopefully faster) than inflation.

Starting with a more traditional portfolio, I then try to only spend the dividends and interest. The analogy I fall back on is owning a rental property. If you are reliably getting rent checks that increase with inflation, you can sit back calmly and ignore what the house might sell for on the open market.

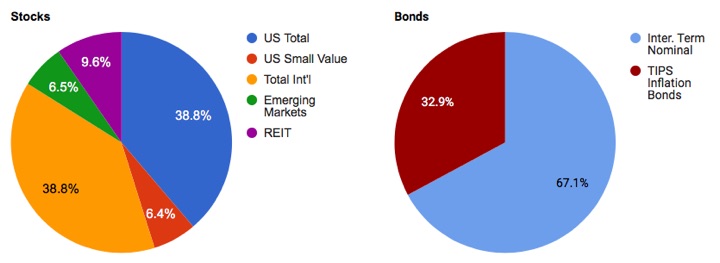

I track the “TTM Yield” or “12 Mo. Yield” from Morningstar, which the sum of a fund’s total trailing 12-month interest and dividend payments divided by the last month’s ending share price (NAV) plus any capital gains distributed over the same period. (Index funds have low turnover and thus little in capital gains.) I like this measure because it is based on historical distributions and not a forecast. Below is a very close approximation of my investment portfolio (2/3rd stocks and 1/3rd bonds).

| Asset Class / Fund | % of Portfolio | Trailing 12-Month Yield (Taken 3/15/19) | Yield Contribution |

| US Total Stock Vanguard Total Stock Market Fund (VTI, VTSAX) |

25% | 1.81% | 0.45% |

| US Small Value Vanguard Small-Cap Value ETF (VBR) |

5% | 2.03% | 0.10% |

| International Total Stock Vanguard Total International Stock Market Fund (VXUS, VTIAX) |

25% | 2.89% | 0.72% |

| Emerging Markets Vanguard Emerging Markets ETF (VWO) |

5% | 2.63% | 0.13% |

| US Real Estate Vanguard REIT Index Fund (VNQ, VGSLX) |

6% | 4.21% | 0.25% |

| Intermediate-Term High Quality Bonds Vanguard Intermediate-Term Tax-Exempt Fund (VWIUX) |

17% | 2.86% | 0.49% |

| Inflation-Linked Treasury Bonds Vanguard Inflation-Protected Securities Fund (VAIPX) |

17% | 3.09% | 0.53% |

| Totals | 100% | 2.67% |

Using this metric, my maximum spending target is a 2.67% withdrawal rate. One of the things I like about using this number is that when stock prices drop, this percentage metric usually goes up… and that makes me feel better in a gloomy market. When stock prices go up, this percentage metric usually goes down, which keeps me from getting too happy. This also applies to the relative performance of US and International stocks. In this way, tracking yield adjusts in a very rough manner for valuation.

We are a real 40-year-old couple with three young kids, and this money has to last us a lifetime (without stomach ulcers). This number does not dictate how much we actually spend every year, but it gives me an idea of how comfortable I am with our withdrawal rate. We spend less than this amount now, but I like to plan for the worst while hoping for the best. For now, we are quite fortunate to be able to do work that is meaningful to us, in an amount where we still enjoy it and don’t feel burned out.

Life is not a Monte Carlo simulation, and you need a plan to ride out the rough times. Even if you run a bunch of numbers looking back to 1920 and it tells you some number is “safe”, that’s still trying to use 100 years of history to forecast 50 years into the future. Michael Pollan says that you can sum up his eating advice as “Eat food, not too much, mostly plants.” You can sum up my thoughts on portfolio income as “Spend mostly dividends and interest. Don’t eat too much principal.” At the same time, live your life. Enjoy your time with family and friends. You may be more likely to run out of time than run out of money.

In the end, I do think using a 3% withdrawal rate is a reasonable target for something retiring young (before age 50) and a 4% withdrawal rate is a reasonable target for one retiring at a more traditional age (closer to 65). If you’re still in the accumulation phase, you don’t really need a more accurate number than that. Focus on your earning potential via better career moves, investing in your skillset, and/or look for entrepreneurial opportunities where you get equity in a business.

We’re in the midst of an extended Spring Break vacation, so posting will be light for the next two weeks. I have some pre-written content scheduled, but the comment moderation may be delayed.

We’re in the midst of an extended Spring Break vacation, so posting will be light for the next two weeks. I have some pre-written content scheduled, but the comment moderation may be delayed. Day 6 of the

Day 6 of the

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)