The Morningstar article Why Investment Complexity Is Not Your Friend points out that out of the thousands of available ETFs and mutuals available, most of them are so narrowly-focused that you really don’t even need to consider them.

What asset classes do you really need to own? Here is their no-nonsense list broken down by “definitely need”, “probably need”, and “don’t need”.

Agree? Disagree? I do believe you can still do quite well over the long run even if keeping things very simple.

Here’s my monthly roundup of the best interest rates on cash as of April 2023, roughly sorted from shortest to longest maturities. We all need some safe assets for cash reserves or portfolio stability, and there are often lesser-known opportunities available to individual investors. Check out my

Here’s my monthly roundup of the best interest rates on cash as of April 2023, roughly sorted from shortest to longest maturities. We all need some safe assets for cash reserves or portfolio stability, and there are often lesser-known opportunities available to individual investors. Check out my  Here’s my 2023 Q1 income update for my

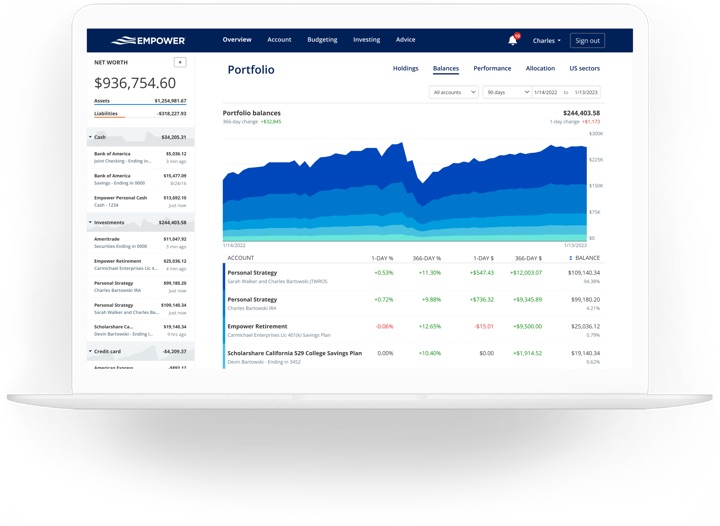

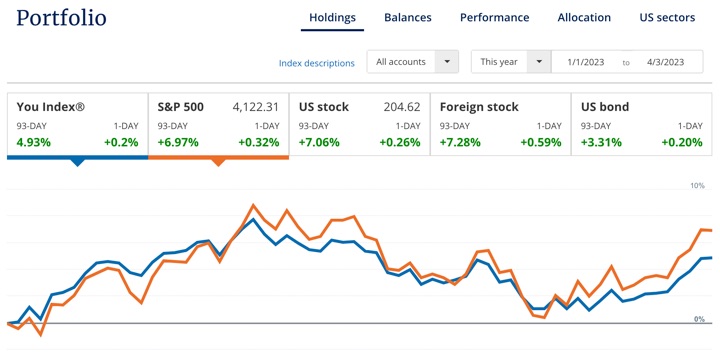

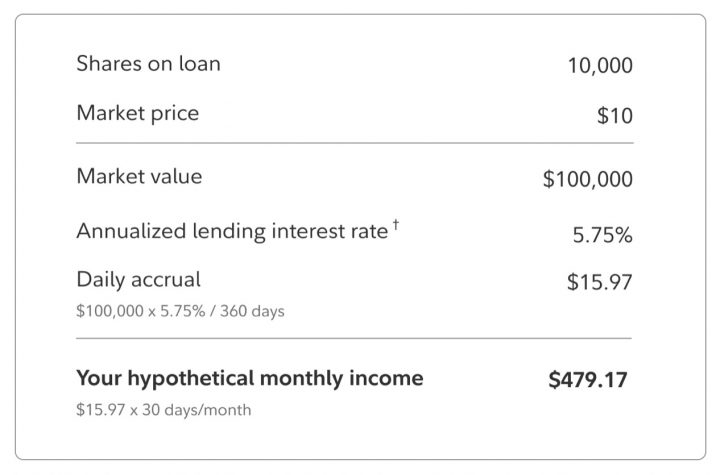

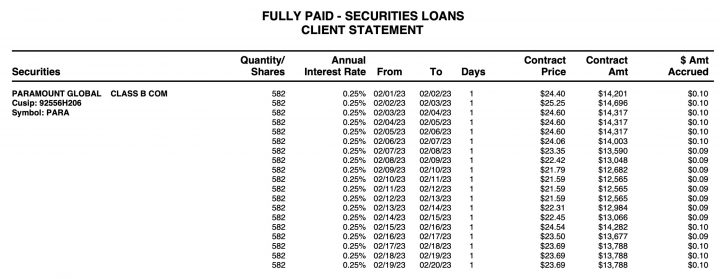

Here’s my 2023 Q1 income update for my

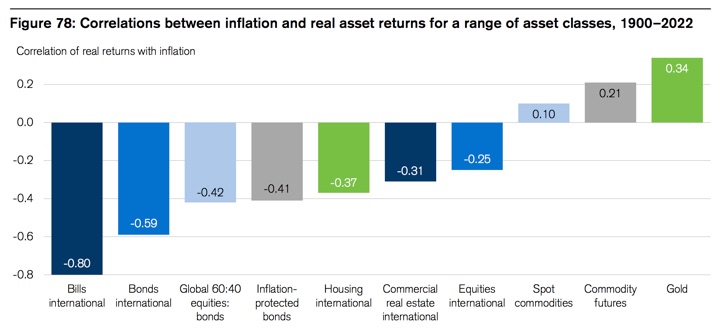

The 15th edition of the Credit Suisse Global Investment Returns Yearbook is available for free download in a

The 15th edition of the Credit Suisse Global Investment Returns Yearbook is available for free download in a

Per

Per

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)