Vanguard has an interesting whitepaper called Automatic Enrollment: The power of the default [pdf]. It takes effort to make a choice beyond the default setting. Doing nothing is always easier. Behavioral economics is still gaining popularity and I knew that auto-enrollment was a powerful way to increase participation in retirement plans, but I didn’t know it was this powerful. Here are a few examples.

Much higher participation: After 3+ years, 90% of auto-enrolled employees kept participating in the retirement plans.

You might think, is that really better than normal? Yes! Here is what participation looked like without auto-enrollment.

Higher contribution rates: After 3 years, 90% of employees auto-enrolled with automatic annual increases indeed kept increasing their contribution percentages. Most stayed with the gradual auto-increase even though they could opt-out at any time, but some also increased more on their own (for example to reach the max).

More appropriate investments: After 3+ years, 94% stayed with a mix of the default and other investments and 74% stayed with solely the default investment option. This is usually a diversified Target Date Fund, whereas in the past a significant amount of participants just stuck with a money market or similar cash account.

My takeaway is that I keep underestimating the power of the default. We see the effects all around us. Why do people keep using Google as their search engine? Default. Switch to DuckDuckGo? Hassle. Why do I simply buy the newest iPhone again after a few years? Default. Switch to Android? Hassle. Buying from Amazon? Easy. Input your name, address, payment info and buy from 100 different online stores? Hassle. Why does Netflix auto-renew with zero effort instead of sending you a bill to pay each month? Behavioral tendencies are big component of business success.

The power of the default is also why you can get $300 to open a new bank account and $500 to try out a new credit card. It takes a big fat incentive for people to move beyond their default. Car insurance companies like GEICO, Progressive, and Liberty mutual spend billions just to get you to even compare premium quotes, let alone switch. Getting over this behavioral tendency is a big component of improving your personal finances.

The official IRA contribution deadline for Tax Year 2021 is April 15th, 2022. However, I choose to use April 15th as the informal deadline for my same-year IRA contributions (Tax Year 2022). By around April 1st, I have usually finished filing my income taxes and thus have handled any expected tax bills. I also have the first quarter of dividends arrive in my brokerage accounts, so I also have funds ready to re-invest. The optimal time would actually be make my contributions on January 1st, but sometimes we just have to settle for “good enough”.

The official IRA contribution deadline for Tax Year 2021 is April 15th, 2022. However, I choose to use April 15th as the informal deadline for my same-year IRA contributions (Tax Year 2022). By around April 1st, I have usually finished filing my income taxes and thus have handled any expected tax bills. I also have the first quarter of dividends arrive in my brokerage accounts, so I also have funds ready to re-invest. The optimal time would actually be make my contributions on January 1st, but sometimes we just have to settle for “good enough”.

Here’s my monthly roundup of the best interest rates on cash as of March 2022, roughly sorted from shortest to longest maturities. I look for lesser-known opportunities available to individuals while still keeping your principal FDIC-insured or equivalent. I use this information for both my cash reserves and as possible bond substitutes. Check out my

Here’s my monthly roundup of the best interest rates on cash as of March 2022, roughly sorted from shortest to longest maturities. I look for lesser-known opportunities available to individuals while still keeping your principal FDIC-insured or equivalent. I use this information for both my cash reserves and as possible bond substitutes. Check out my  Stash $20 in Free Stock Offer

Stash $20 in Free Stock Offer WeBull 12 Free Fractional Stocks Offer

WeBull 12 Free Fractional Stocks Offer SoFi Invest Free $25 in Stock Offer

SoFi Invest Free $25 in Stock Offer TradeUP Free Stocks Offer

TradeUP Free Stocks Offer Public Free Stock Offer

Public Free Stock Offer Robinhood Free Stock Offer

Robinhood Free Stock Offer

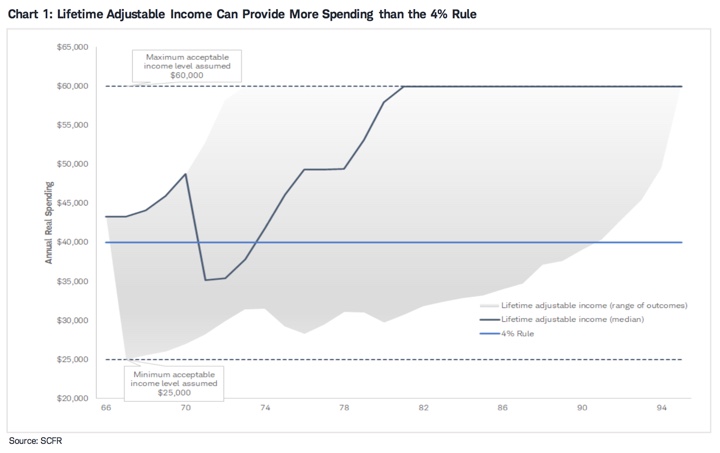

One of the perpetual debates in retirement planning circles is withdrawal rates, AKA how much monthly income can you take from a portfolio. Once you nail down a withdrawal rate and retirement spending target, then you get Your Number – how much you need to have saved to retire (after backing out Social Security and other income streams). It’s common to start with the static 4% rule, but that rule also includes some drawbacks. An alternative is a flexible withdrawal rule that adjusts based on market returns. When your portfolio grows, you can spend a little more. If it shrinks, you cut back a little. Sounds reasonable, right?

One of the perpetual debates in retirement planning circles is withdrawal rates, AKA how much monthly income can you take from a portfolio. Once you nail down a withdrawal rate and retirement spending target, then you get Your Number – how much you need to have saved to retire (after backing out Social Security and other income streams). It’s common to start with the static 4% rule, but that rule also includes some drawbacks. An alternative is a flexible withdrawal rule that adjusts based on market returns. When your portfolio grows, you can spend a little more. If it shrinks, you cut back a little. Sounds reasonable, right?

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)