On March 6, 2009, the S&P 500 index hit 666.80, shedding 13 years of gains. 13 years! Guess how long it has been since March 2009? 13 years! Something to ponder as the possibility of more war looms ahead.

On March 6, 2009, the S&P 500 index hit 666.80, shedding 13 years of gains. 13 years! Guess how long it has been since March 2009? 13 years! Something to ponder as the possibility of more war looms ahead.

I remember my portfolio being halved at the time and thinking… how can it not eventually be back at at 1,000? Should I double down on stocks? Meanwhile, Goldman Sachs released “analyst research” that warned the S&P could fall as low as 400. People were panicked and “get out now and wait until things calm down” started to sound more and more like solid advice. The best I could do was not sell anything.

I am re-reading The Psychology of Money by Morgan Housel. In this book of timeless advice about controlling your behavior, he points out that the long-term stock returns that we all expect is not free. There is a price that must be paid.

Like everything else worthwhile, successful investing demands a price. But its currency is not dollars and cents. It’s volatility, fear, doubt, uncertainty, and regret—all of which are easy to overlook until you’re dealing with them in real time.

We should accept this price volatility as an expected cost of doing business, not something to be avoided:

It sounds trivial, but thinking of market volatility as a fee rather than a fine is an important part of developing the kind of mindset that lets you stick around long enough for investing gains to work in your favor. Few investors have the disposition to say, “I’m actually fine if I lose 20% of my money.” This is doubly true for new investors who have never experienced a 20% decline. But if you view volatility as a fee, things look different.

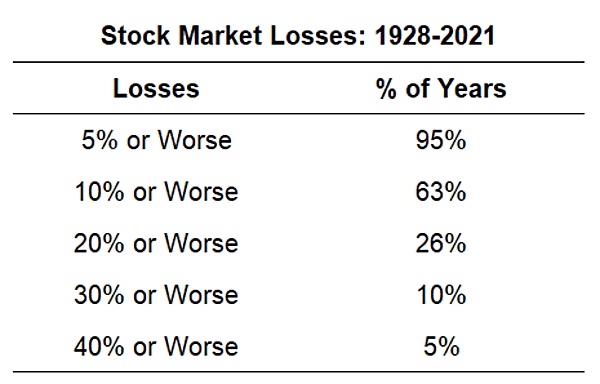

From A Wealth of Common Sense, we can get a better understanding of How Often Should You Expect a Stock Market Correction?

I would add one thing. Accepting price swings after looking at a chart may sound okay in isolation. However, you should also prepare for the fact that there will always be a great reason for those drops. We’ve had housing bubbles and dot-com bubbles and now worldwide pandemics. But the next reason will likely be different. And it will be a widely-accepted, legit, scary reason. I will be scared. You will be scared.

If I mentally agree to pay this price now, hopefully it will help me when the next scary thing inevitably comes along.

Charlie Munger is now 98 years old and still answering questions at the 2022 Daily Journal Annual Shareholder Meeting. Yahoo Finance livestreamed the event again, and you can view the full two-hour recording on

Charlie Munger is now 98 years old and still answering questions at the 2022 Daily Journal Annual Shareholder Meeting. Yahoo Finance livestreamed the event again, and you can view the full two-hour recording on

Here’s my monthly roundup of the best interest rates on cash as of January 2022, roughly sorted from shortest to longest maturities. I look for lesser-known opportunities earning more than most “high-yield” savings accounts and money market funds while still keeping your principal FDIC-insured or equivalent. Check out my

Here’s my monthly roundup of the best interest rates on cash as of January 2022, roughly sorted from shortest to longest maturities. I look for lesser-known opportunities earning more than most “high-yield” savings accounts and money market funds while still keeping your principal FDIC-insured or equivalent. Check out my

Here’s my (late) quarterly update on the income produced by my “

Here’s my (late) quarterly update on the income produced by my “

Here’s my (late) quarterly update on my current investment holdings, as of 1/23/22, including our 401k/403b/IRAs and taxable brokerage accounts but excluding a side portfolio of self-directed investments. Following the concept of

Here’s my (late) quarterly update on my current investment holdings, as of 1/23/22, including our 401k/403b/IRAs and taxable brokerage accounts but excluding a side portfolio of self-directed investments. Following the concept of

Instead of focusing on the current hot thing, how about stepping back and taking the longer view? How would a steady investor have done over the last decade? Most successful savers invest money each year over a long period of time.

Instead of focusing on the current hot thing, how about stepping back and taking the longer view? How would a steady investor have done over the last decade? Most successful savers invest money each year over a long period of time.

The GMO quarterly letter is on my recurring “must read” list, and the 2021 Q3 letter

The GMO quarterly letter is on my recurring “must read” list, and the 2021 Q3 letter

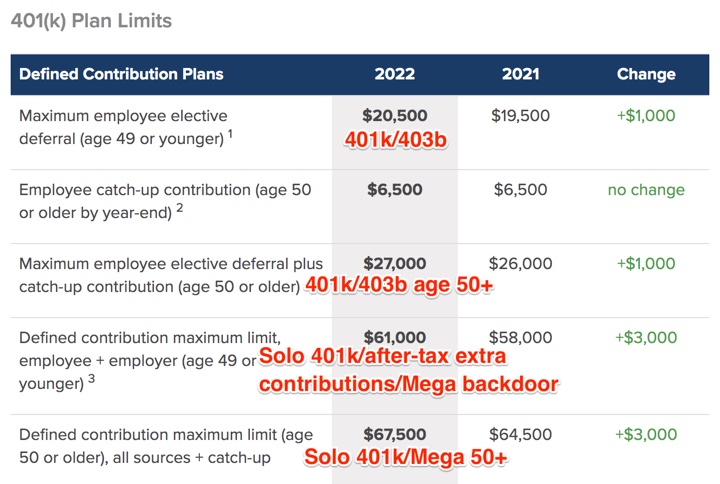

The beginning of the year is a good time to check on the new annual contribution limits to the various available retirement accounts. Our income has been quite variable these last few years, so I regularly adjust the paycheck deferral percentages based on expected income for the year. This

The beginning of the year is a good time to check on the new annual contribution limits to the various available retirement accounts. Our income has been quite variable these last few years, so I regularly adjust the paycheck deferral percentages based on expected income for the year. This

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)