![]() The Vanguard Target Retirement Funds are one of the largest “set-and-forget” mutual funds that own a mix of stocks and bonds that automatically adjust over time based on your targeted retirement year, with combined assets across the institutional and retail classes of over $600 billion.

The Vanguard Target Retirement Funds are one of the largest “set-and-forget” mutual funds that own a mix of stocks and bonds that automatically adjust over time based on your targeted retirement year, with combined assets across the institutional and retail classes of over $600 billion.

Reader rp pointed out that on December 30th, 2021, many Vanguard Target Retirement funds had their price (NAV) drop by over 10% in a single day! This was mostly the result of an abnormally large year-end long-term and short-term capital gains distribution. Taken from Vanguard’s final year-end estimates PDF:

Here is an example for the Vanguard Target Retirement 2040 Fund (VFORX). The 2021 cap-gains distribution was roughly 40 times as large as for 2020. Yet, other funds with a similar asset allocation like the Vanguard LifeStrategy Funds did not have a similar result. What happened?

Background. A mutual fund is forced to make a capital gains distribution when it sells stocks (or bonds) that have appreciated in value, thus realizing capital gains. There are various reasons why a mutual fund might sell stocks:

- An actively-managed fund might sell shares of stocks that they believe are over-valued in order to purchase shares of another business.

- An index fund might have to sell shares if the underlying index changes. By definition, an index fund must track an index. For example, sometimes the S&P 500 will remove a company from its index.

- A balanced mutual fund might rebalance between stocks and bonds. If the target is 80% stocks and 20% bonds, the fund might sell some stocks after a big bull run in order to buy some bonds and revert back towards the target.

- A mutual fund has a high number of redemptions (cash outflows), such that the fund has to sell assets in order to come up with the cash to satisfy all those withdrawals.

Vanguard Target Retirement Funds don’t follow an index themselves, as they are a “fund of funds”. That means they are basically a wrapper for the component index funds. For example, the Vanguard Target Retirement 2055 Fund (VFFVX) is composed of:

- Vanguard Total Stock Market Index Fund Investor Shares 54.90%

- Vanguard Total International Stock Index Fund Investor Shares 35.50%

- Vanguard Total Bond Market II Index Fund Investor Shares 6.60%

- Vanguard Total International Bond Index Fund Investor Shares 2.80%

- Vanguard Total International Bond II Index Fund 0.20%

However, these underlying funds did not have huge capital gains distributions themselves that might flow through. In fact, the main components had zero capital gains to distribute, while the other distributed tiny amounts less than 1%.

What we have left is that the Target Retirement Fund itself sold some shares of the component index funds. Stocks did go up in 2021, but not nearly enough to warrant such a huge capital gain. Besides, stocks also went up a similar amount in 2020, and as we saw above the 2020 capital gains distribution was 40x smaller.

In addition, the Institutional Target Retirement 2040 fund only had cap gains distributions of 0.39% of NAV. This fund should have the same rebalancing needs as the retail version for individual investors. The rest of the Institutional Target Retirement years had similarly low distributions.

Strange! Thankfully, I found a great clue by “cas” in this Bogleheads thread. From reading the annual reports for VFORX, we find that as of 3/31/21, the net assets for Target Retirement 2040 was about $35 billion. From January through September 2021, over $16 billion of shares were redeemed from the Target Retirement 2040 fund, while only $6 billion were purchased. The underlying investments grew in value, but investors took out a net $10 billion in cash over the first 9 months of 2021! The large capital gains distribution was primarily due to these large net redemptions.

Okay, but again, why? The main problem was that the “Institutional Target Retirement Funds” are not a share class of the “Target Retirement Funds”. In December 2020, Vanguard lowered the plan-level minimum investment requirement for the Institutional Target Retirement Funds to $5 million from $100 million. Now, as long as an employer’s 401k plan had $5 million in assets across the entire plan (not just one person), they could now access the much cheaper Institutional version… a big savings for possibly thousands of small businesses.

Let’s check the annual reports again. Over the same time period that Target Retirement 2040 lost $10 billion in net cash outflows, the Institutional Target Retirement 2040 Fund gained $13 billion in net cash inflows. Coincidence?

Vanguard incentivized small business retirement plans to sell their holdings from Target Retirement in order to buy Institutional Target Retirement funds by offering them a 30% to 50% reduction in fees, and they did so, moving over billions and billions.

Eventually, in September 2021, Vanguard announced that they would merge each of the Vanguard Institutional Target Retirement Funds into its corresponding Target Retirement Fund. The mergers are not scheduled to be completed until February 2022. There may be more outflows until then. A merger would not have created any forced selling, so why not do this in the first place?

I wonder if Vanguard made a mistake and they simply didn’t realize this would create large outflows. Or perhaps they just didn’t care? Either way, it’s another recent blemish on their record. The order and time delay in which they did things indirectly hurt the individual taxable investors of Target Retirement funds. They should have simply merged the two series in the first place.

This is why the DIY investor should strongly consider only investing in the “raw materials” and “cook from scratch”. VTI, VXUS, and BND ETFs can be held at any brokerage firm, bought and sold for free, distributed tax-efficiently between 401k/IRA and taxable, and are available for ETF-pair tax-loss harvesting in a taxable account. On the other hand, this is something of a one-time event, so you may value the simplicity of Target Retirement funds above the potential drawbacks.

If you like the idea of “auto-pilot” but also want to be be only one allowed to program the autopilot, check out out M1 Finance and their pies (which you can always break back up into component ETFs) as well as Utah My529 and their “customized glide path” option for college savings. I don’t like the fact that Vanguard can always change up their target asset allocation to whatever is trendy. (I have the same issues with the robo-advisors like Wealthfront and Betterment.)

Summary. Vanguard Target Retirement Funds (Investor shares) made large capital gains distributions at the end of 2021. This was mostly due to large outflows from Target Retirement Funds (owned by individual investors and small businesses) into their separate Institutional Target Retirement Funds, as Vanguard lowered the minimums for the Institutional funds from $100 million to $5 million in December 2020. This appears to have forced the Target Retirement funds so sell their investments and incur large capital gains.

If you hold Target Retirement funds in a tax-deferred accounts like 401k/403b/IRA, this has no taxable effect on you. The net asset value (NAV) dropped by a certain amount, and you received a distribution for the same amount. You most likely have it set to reinvest immediately anyway. However, if you held this in a taxable account, you received a taxable distribution. You now owe some extra tax and lost the ability to compound that money into the future. It’s not a disaster, but it did hurt your returns a little, in my view unnecessarily as Vanguard could have handled things differently on their end.

2021 is finally in the books! Most of my portfolio is in low-cost index funds across various asset classes, which I purposefully ignore most of the time as I believe the proper time horizon is at least several years long. However, I do check in once a year. Per Morningstar, here are the annual returns for select asset classes as benchmarked by popular ETFs after market close 12/31/21.

2021 is finally in the books! Most of my portfolio is in low-cost index funds across various asset classes, which I purposefully ignore most of the time as I believe the proper time horizon is at least several years long. However, I do check in once a year. Per Morningstar, here are the annual returns for select asset classes as benchmarked by popular ETFs after market close 12/31/21.

A few readers asked about “fully paid lending programs” offered by some brokerage firms. The premise is very intriguing: You lend out the stock shares you own and earn interest, all while keeping full “economic” ownership. You still get any upside or downside, you can still sell at any time, and your loans are backed by 100%+ collateral at a custodial bank. The broker finds borrowers, collects interest, and splits it with you (usually 50/50). Is this zero-effort free money? These programs can go by various names:

A few readers asked about “fully paid lending programs” offered by some brokerage firms. The premise is very intriguing: You lend out the stock shares you own and earn interest, all while keeping full “economic” ownership. You still get any upside or downside, you can still sell at any time, and your loans are backed by 100%+ collateral at a custodial bank. The broker finds borrowers, collects interest, and splits it with you (usually 50/50). Is this zero-effort free money? These programs can go by various names:

One of my newer interests is better understanding individual businesses and how they work. Accounting is the “language of business” used to write annual reports, 10-Ks, 10-Qs, income statements, and so on. I was afraid a textbook would be too boring, so I am auditing the online Coursera course

One of my newer interests is better understanding individual businesses and how they work. Accounting is the “language of business” used to write annual reports, 10-Ks, 10-Qs, income statements, and so on. I was afraid a textbook would be too boring, so I am auditing the online Coursera course  Financial freedom seekers usually have a Number – the value at which their investments can support their spending indefinitely. This is directly linked to “safe withdrawal rates”. For example a 4% safe withdrawal rate is a 25x multiplier – meaning $30,000 in spending needs not covered by Social Security, annuities, or pensions would require 25 x $30,000 = $750,000. Morningstar recently released a 59-page research paper called

Financial freedom seekers usually have a Number – the value at which their investments can support their spending indefinitely. This is directly linked to “safe withdrawal rates”. For example a 4% safe withdrawal rate is a 25x multiplier – meaning $30,000 in spending needs not covered by Social Security, annuities, or pensions would require 25 x $30,000 = $750,000. Morningstar recently released a 59-page research paper called

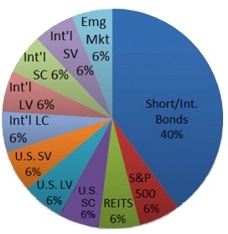

Some investors like to break down their portfolio into several different asset and sub-asset classes. One long-standing example of the “slice-and-dice” is the “

Some investors like to break down their portfolio into several different asset and sub-asset classes. One long-standing example of the “slice-and-dice” is the “ Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.

Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.  Investment research firm Morningstar has released their annual 529 College Savings Plans

Investment research firm Morningstar has released their annual 529 College Savings Plans

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)