Update. RealtyShares has a referral program that offers a new customer who is referred by an existing client a $100 gift card after linking a bank account. I am no longer available to provide referrals as I have maxed out the limit, but you may be able to find a referral from existing client elsewhere.

Alternatively, using this link and using the code JONATHANPING25 will get you a free $25 to start.

Be sure to follow the terms and conditions and reply to your bank link confirmation e-mail with the proper promo code:

In order to receive $25 sign up bonus, user must register, connect a bank account, and use the promocode provided in the email they received about the program. Payouts to user will be within 30 days via your linked bank account. RealtyShares reserves the right to stop or modify the referral program at its discretion at any time.

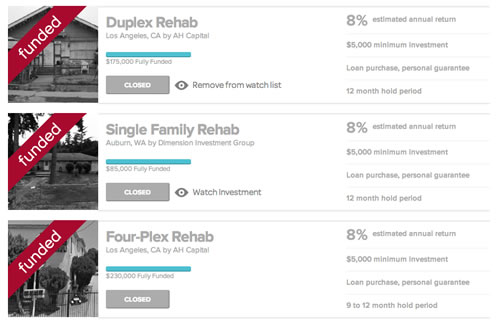

Here’s an update on one of my

Here’s an update on one of my

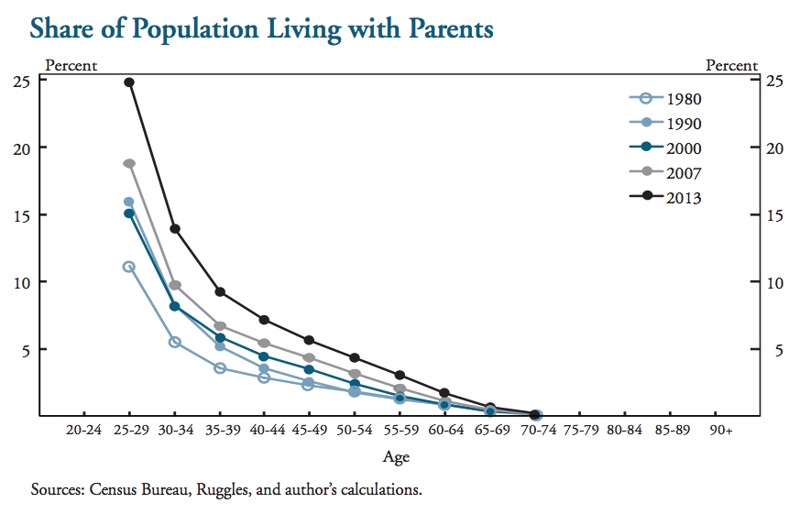

Inside a post about what economists think about buying vs. renting a house,

Inside a post about what economists think about buying vs. renting a house,

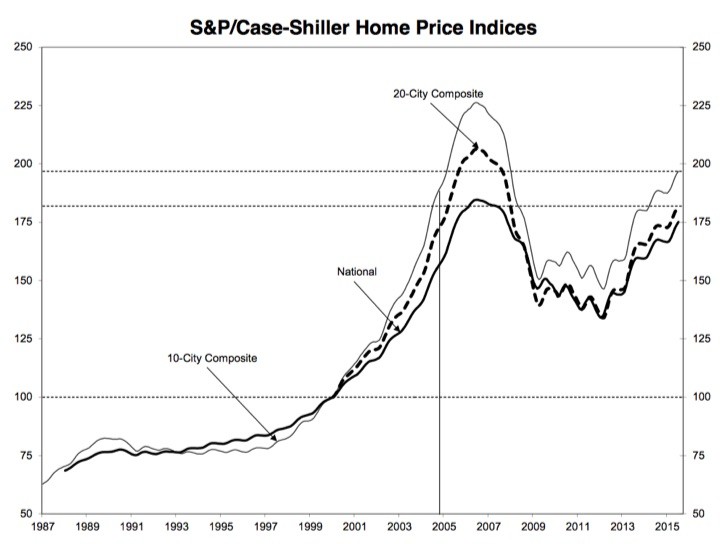

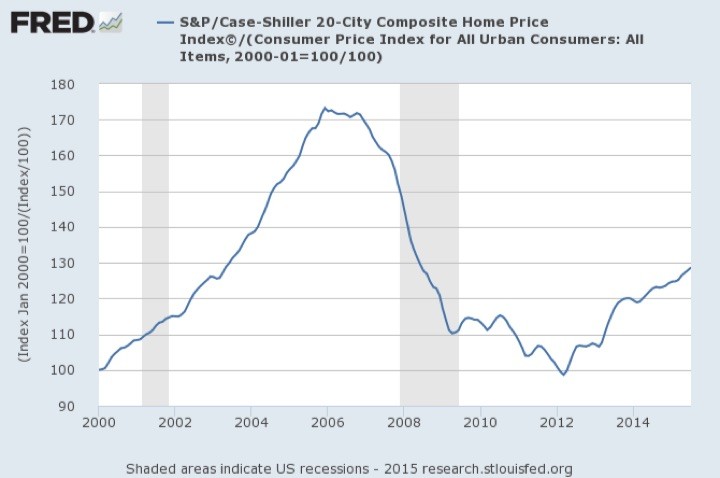

Here’s an update on residential real estate prices via the

Here’s an update on residential real estate prices via the

Updated. Buying a house is always an exciting yet terrifying time. Deciding on how much we can “afford” is often limited by how much someone will lend us. Mortgage lenders use income size, income stability, credit score, down payment size, and other factors before approving a loan. Let’s explore the idea of a “rule of thumb” to greatly simplify such a complicated matter. The most common way to express affordability is as a multiple of your household or individual annual income.

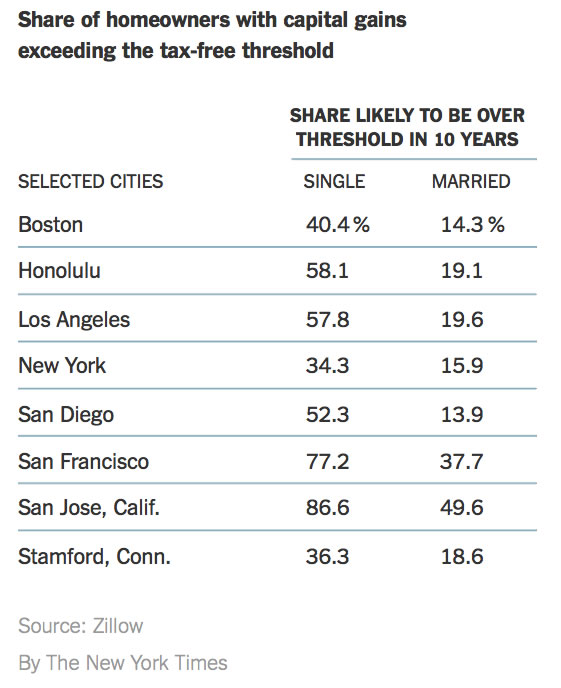

Updated. Buying a house is always an exciting yet terrifying time. Deciding on how much we can “afford” is often limited by how much someone will lend us. Mortgage lenders use income size, income stability, credit score, down payment size, and other factors before approving a loan. Let’s explore the idea of a “rule of thumb” to greatly simplify such a complicated matter. The most common way to express affordability is as a multiple of your household or individual annual income. For many people, when they sell a home they don’t even consider taxes. But over time, especially if you live in a relatively expensive area, more and more people will bump up against the federal capital gains exclusions of $250,000 for individuals and $500,000 for couples. (You must have lived in the home for at least two out of the five years before the sale.)

For many people, when they sell a home they don’t even consider taxes. But over time, especially if you live in a relatively expensive area, more and more people will bump up against the federal capital gains exclusions of $250,000 for individuals and $500,000 for couples. (You must have lived in the home for at least two out of the five years before the sale.)

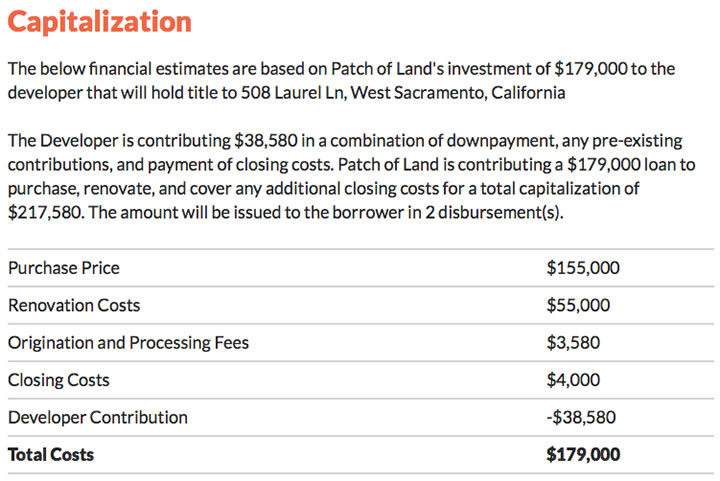

I’m not sure exactly what details of this investment I am allowed to share, so I’ll save that part for later. It will be good for you guys to pick apart, but it doesn’t really matter for other investors as the project is already 100% funded. I’m just waiting on my first interest payment in May, and hope to be done by October. At the end of the year I will get a 1099-INT.

I’m not sure exactly what details of this investment I am allowed to share, so I’ll save that part for later. It will be good for you guys to pick apart, but it doesn’t really matter for other investors as the project is already 100% funded. I’m just waiting on my first interest payment in May, and hope to be done by October. At the end of the year I will get a 1099-INT.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)