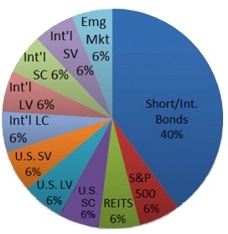

Some investors like to break down their portfolio into several different asset and sub-asset classes. One long-standing example of the “slice-and-dice” is the “Ultimate Buy-and-Hold Portfolio” recommended by Paul Merriman (see pie chart; expanded labels below). You don’t need to hold every one of these asset classes, but when held in combination they historically offer a higher return with lower volatility.

Some investors like to break down their portfolio into several different asset and sub-asset classes. One long-standing example of the “slice-and-dice” is the “Ultimate Buy-and-Hold Portfolio” recommended by Paul Merriman (see pie chart; expanded labels below). You don’t need to hold every one of these asset classes, but when held in combination they historically offer a higher return with lower volatility.

- S&P 500 (US Large Cap Blend)

- US Large Value

- US Small

- US Small Value

- US REIT

- International Large Cap Blend

- International US Large Value

- International Small

- International Small Value

- Emerging Markets

- Short-term/Intermediate-term Bonds

For a long time, Dimensional Fund Advisors (DFA) offered some of the best lower-cost mutual funds tracking these types of sub-asset classes, but they also required you to invest through a DFA-affiliated financial advisor (and pay the accompanying management fees). Eventually, some former DFA executives and employees broke off and started Avantis ETFs, which are available to any investor with a brokerage accounts and offered a good DFA alternative. Avantis’ assets under management have been growing…

Lo and behold, DFA has just announced a big expansion of their DFA ETF lineup. Competition works!

Newly-listed DFA Bond ETFs

- Dimensional Core Fixed Income ETF (DFCF)

- Dimensional Short-Duration Fixed Income ETF (DFSD)

- Dimensional National Municipal Bond ETF (DFNM)

- Dimensional Inflation-Protected Securities ETF (DFIP)

Future DFA Equity ETFs

- International Core Equity 2 ETF

- Emerging Markets Core Equity 2 ETF

- US Small Cap Value ETF

- International Small Cap ETF

- International Small Cap Value ETF

- Emerging Markets Value ETF

- US High Profitability ETF

- International High Profitability ETF

- Emerging Markets High Profitability ETF

- US Real Estate ETF

Existing DFA ETFs

- Dimensional US Core Equity Market ETF (DFAU)

- Dimensional International Core Equity Market ETF (DFAI)

- Dimensional Emerging Core Equity Market ETF (DFAE)

- Dimensional US Core Equity 2 ETF (DFAC)

- Dimensional US Equity ETF (DFUS)

- Dimensional US Small Cap ETF (DFAS)

- Dimensional US Targeted Value ETF (DFAT)

- Dimensional International Value ETF (DFIV)

- Dimensional World ex US Core Equity 2 ETF (DFAX)

Some of the confusing names are a result of these ETFs being conversions from the old mutual fund versions. Even though I try to keep things relatively simple and humble, I welcome these new investment options to the competitive marketplace along with their reasonably-low expense ratios. I may even switch my TIPS holdings to the DFA TIPS ETF (DFIP), as it is cheaper than the iShares TIPS Bond ETF (TIP).

I use Vanguard for my “core” index funds, but about 10% of my total portfolio is split between US Small Value and International/Emerging Small Value stocks. I recently bought/rebalanced into some of the new Avantis International Small Cap Value ETF (AVDV), but will keep an eye on the new DFA version. I suppose they could be a tax-loss harvesting ETF pair, but I have them inside a tax-sheltered account.

Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.

Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.  While my

While my

Here’s my quarterly update on my current investment holdings as of October 2021, including our 401k/403b/IRAs and taxable brokerage accounts but excluding our house, “emergency fund” cash reserves, and a side portfolio of self-directed investments. Following the concept of

Here’s my quarterly update on my current investment holdings as of October 2021, including our 401k/403b/IRAs and taxable brokerage accounts but excluding our house, “emergency fund” cash reserves, and a side portfolio of self-directed investments. Following the concept of

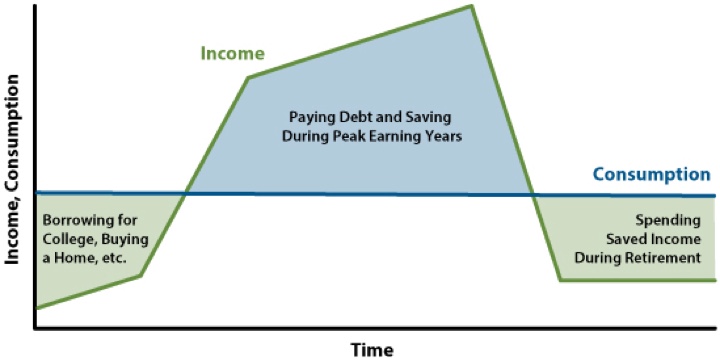

Just over 45 years ago on August 31st, 1976, the late Jack Bogle started the first index mutual fund at Vanguard. It nearly didn’t get off the ground, garnering only 7% of the initial funding goal – it wasn’t even enough to buy shares of all the stocks in the S&P 500! Read Bogle’s own take from exactly 10 years ago at this

Just over 45 years ago on August 31st, 1976, the late Jack Bogle started the first index mutual fund at Vanguard. It nearly didn’t get off the ground, garnering only 7% of the initial funding goal – it wasn’t even enough to buy shares of all the stocks in the S&P 500! Read Bogle’s own take from exactly 10 years ago at this

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)