The 2021 Berkshire Hathaway Annual Shareholder Meeting was on May 1st, 2022 and is now available as a recorded video on Yahoo Finance and a handy Rev.com transcript. I expect the podcast version to be updated shortly. I recommend listening or reading on your own, as I always find valuable tidbits outside the media highlights.

The 2021 Berkshire Hathaway Annual Shareholder Meeting was on May 1st, 2022 and is now available as a recorded video on Yahoo Finance and a handy Rev.com transcript. I expect the podcast version to be updated shortly. I recommend listening or reading on your own, as I always find valuable tidbits outside the media highlights.

Buffett started out with the 2021 version of his annual advice for the average investor that doesn’t read 10-K SEC filings, shareholder annual reports, and multiple newspapers in their entirety every day: buy index funds. Buffett created a few slides for those “new entrants” who might think stock market investing means trading 25 times a day on Robinhood.

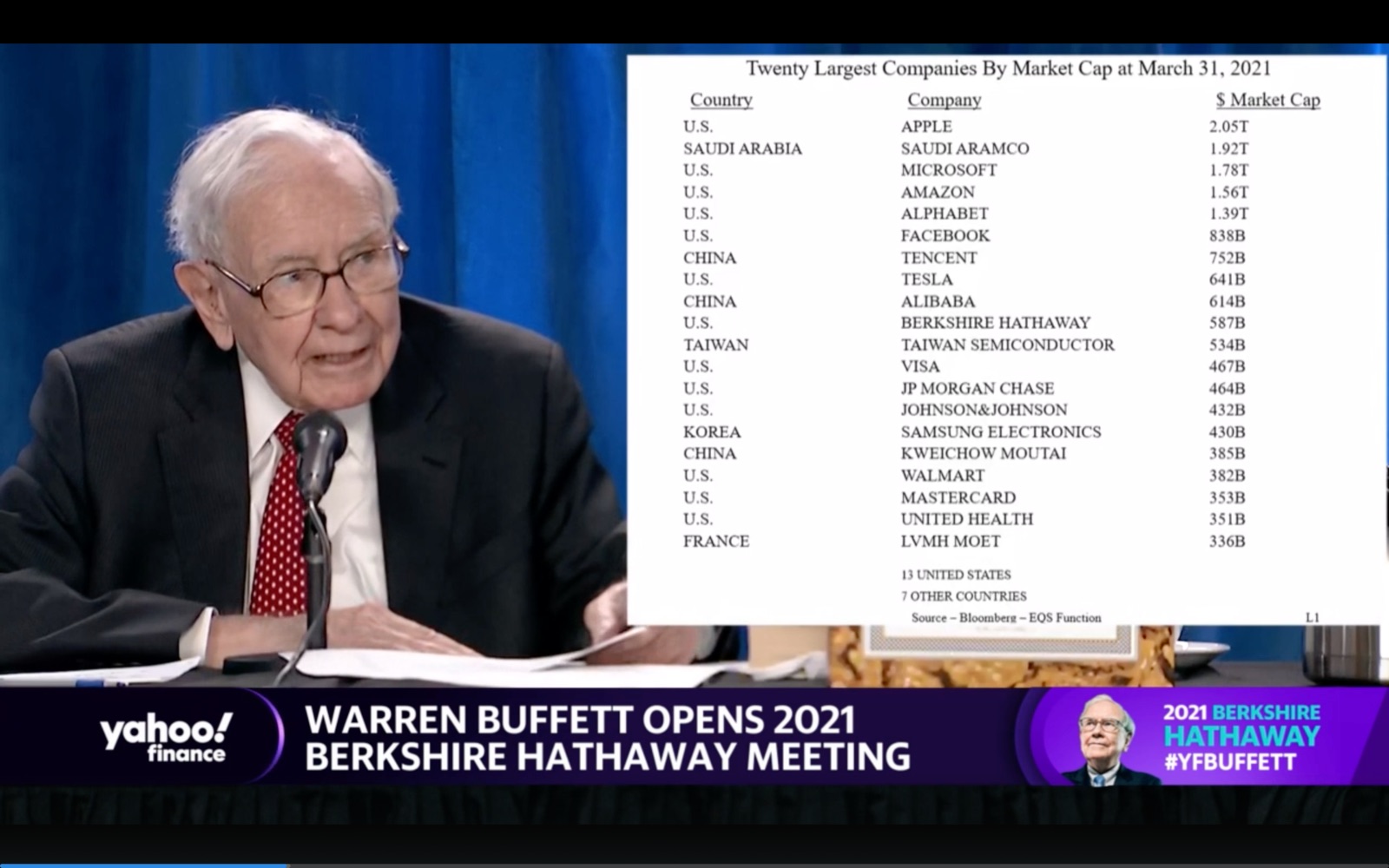

Here are the 20 most valuable companies in the world as of March 31st, 2021. The list includes 13 from the United States, three from China, and one each from Saudi Arabia, Taiwan, South Korea, and France.

He then asks “How many of these companies do you think will be on this same Top 20 list in 30 years? (2051)”

8?

5?

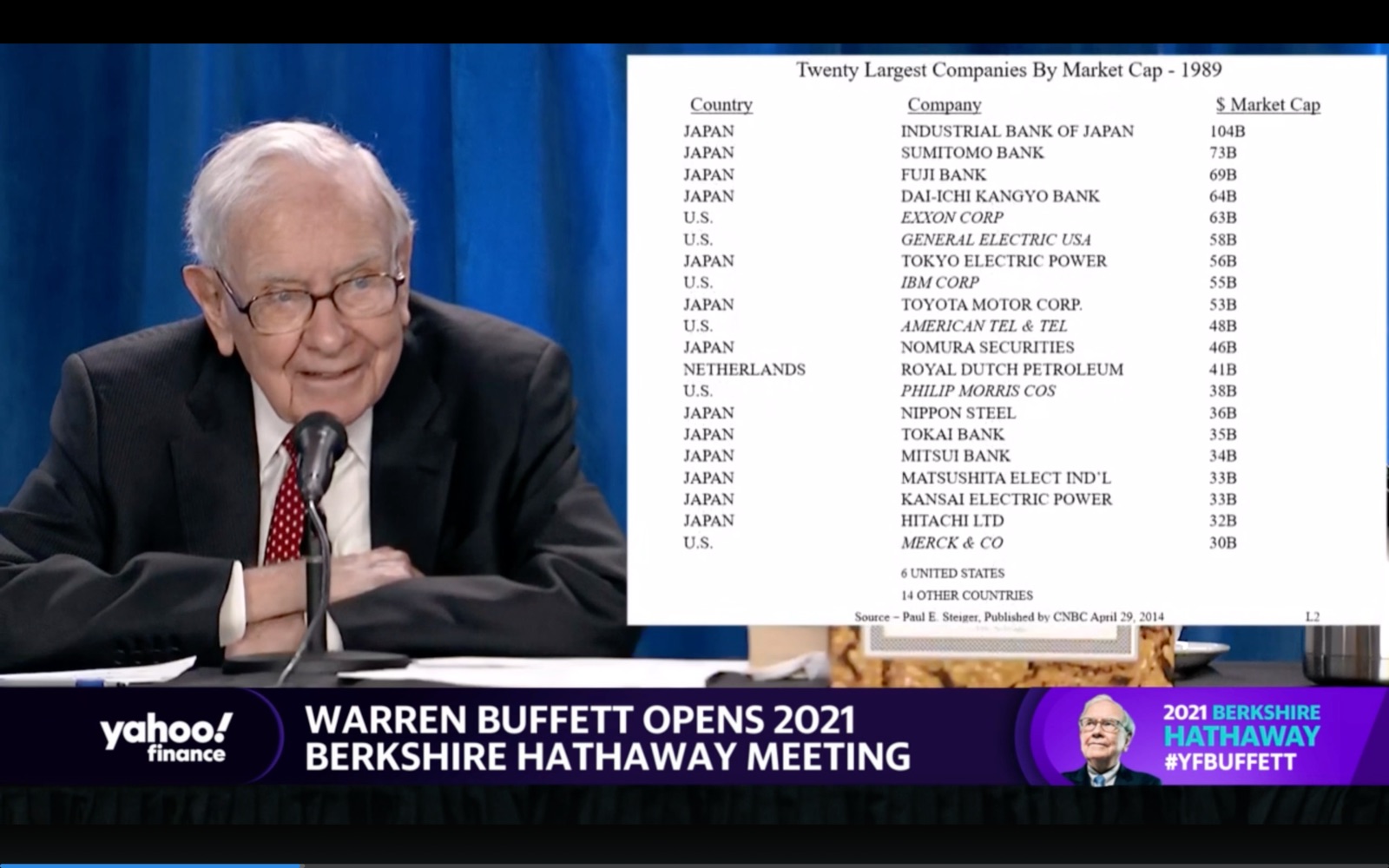

Once you have the answer in mind, you can consider this list of the 20 most valuable companies in the world from ~30 years ago (1989).

There is zero overlap in the two lists in regards to actual companies. Some names might be familiar, but not a single company stayed in the top 20. The 1989 list includes 13 from Japan, 6 from the United States, and one from the Netherlands.

In 1989, the most valuable company was worth $100 billion. (That company, the Industrial Bank of Japan, later merged with another business and that new company is only worth $37 billion in 2021.) Meanwhile, the most valuable company of 2021 is worth over $2,000 billion, a 20X increase.

If you are under the age of 50, you are a time billionaire. Your time horizon is a billion seconds (30 years) or longer. Many things will change over that period. Hopefully you will enjoy a happy, fulfilling life. But if you own a low-cost, market-cap weighted index fund, you will be guaranteed to own the world’s largest companies in 2051. As the late Jack Bogle told us: “Don’t look for the needle in the haystack. Just buy the haystack.” He might have added “…and get on with your life!”.

This comparison also shows why I remain diversified internationally, even though it hasn’t paid off recently. Does anyone really know that the future holds in regards to world geopolitics? It’s possible the US companies will continue to outperform for another 30 years. I hope so, and if that happens then I’ll hold a large majority of US stocks in the future. It will work itself out.

As part of a complete personal finance education, I submit that the longread article

As part of a complete personal finance education, I submit that the longread article

Although I’m still decades away from Social Security, I see a constant stream of articles about the “best” time to start taking benefits. Often, you are told to delay claiming until age 70, as you will receive a more valuable, inflation-adjusted, government-guaranteed payout for the rest of your life. But if you have a spouse, it may be better for one of them to claim as early as possible, at age 62. There are many calculators out there – here is one

Although I’m still decades away from Social Security, I see a constant stream of articles about the “best” time to start taking benefits. Often, you are told to delay claiming until age 70, as you will receive a more valuable, inflation-adjusted, government-guaranteed payout for the rest of your life. But if you have a spouse, it may be better for one of them to claim as early as possible, at age 62. There are many calculators out there – here is one

Instead of focusing only on

Instead of focusing only on

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)