Paul Merriman is a long-time financial advisor known for his “Ultimate Buy-and-Hold Portfolio” that utilized a more complex 10-fund version of a low-cost index fund portfolio. Although now retired from advising, he continues to add new content to his website for the Merriman Financial Education Foundation that is geared more towards to DIY investors.

He has published a new book called We’re Talking Millions!: 12 Simple Ways to Supercharge Your Retirement by himself and co-author Richard Buck. For a very limited-time, you can download this book in PDF format for free. I would recommend downloading it now and saving it to read later. I haven’t read it yet, but a quick skim shows that it appears to be a condensed version of everything on his site.

This book is designed to show you how you can change your life by making a handful of smart choices. It’s a recipe for potentially accumulating millions of dollars you can spend in retirement and leave to your heirs. […] But one thing is new: an action plan that applies them in a single solution that can be carried out easily by just about anybody who has a job. We call this plan Two Funds for Life.

Much of the 12 steps are based on common personal-finance advice, and they are still good advice. But if you’re looking for what Merriman offers that is different, that’s the “Two Funds for Life”. It appears that Merriman is still a strong believer in the future outperformance of small-cap value stocks. Here are the bare basics:

The basic Two Funds for Life recommendation for your 401(k) plan is pretty simple:

• Multiply your age by 1.5.

• Use the result as the percentage of your portfolio that should be in a target-date retirement fund. The rest goes into a small company value fund.

• As you get older, rebalance these two funds periodically, ideally once a year, based on your age at the time. This will gradually reduce your small-company value exposure.

Based on this formula, a 30 year-old today would hold 55% of their portfolio in a low-cost US Small-Cap Value index fund and 45% in a Vanguard Target 2055 Retirement Fund (assuming retirement at age 65). The Small-Cap Value percentage decreases each year by 1.5%. By the time they are 65 years-old, they would effectively transitioned to 100% Vanguard Target Retirement (Income) fund.

I appreciate the simplicity as this is much easier than juggling 10 funds yourself (Merriman also recommends M1 Finance to manage your DIY portfolio automatically). Still, 55% is a lot to hold in Small Value and you will definitely want to have read enough about company size and value factor investing and have faith in the fundamental reasons behind this approach before implementing this plan. I’m sure the book will contain his supporting evidence, but you should read about all the drawbacks as well before making the final decision. I own a small-cap value fund myself, and you must accept that small value stocks have gone through very long periods of underperformance relative to the S&P 500.

If you have a workplace 401k/403b/457 retirement plan, there is probably a target-date fund (TDF) inside. TDFs provide a “set-and-forget” investment option that automatically adjusts the asset allocation over time as you move towards your target retirement age. A recent WSJ article

If you have a workplace 401k/403b/457 retirement plan, there is probably a target-date fund (TDF) inside. TDFs provide a “set-and-forget” investment option that automatically adjusts the asset allocation over time as you move towards your target retirement age. A recent WSJ article

Allan Roth is one of the financial planners whose independent opinions I have come to respect, and he shares

Allan Roth is one of the financial planners whose independent opinions I have come to respect, and he shares

Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.

Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.  After reading the

After reading the

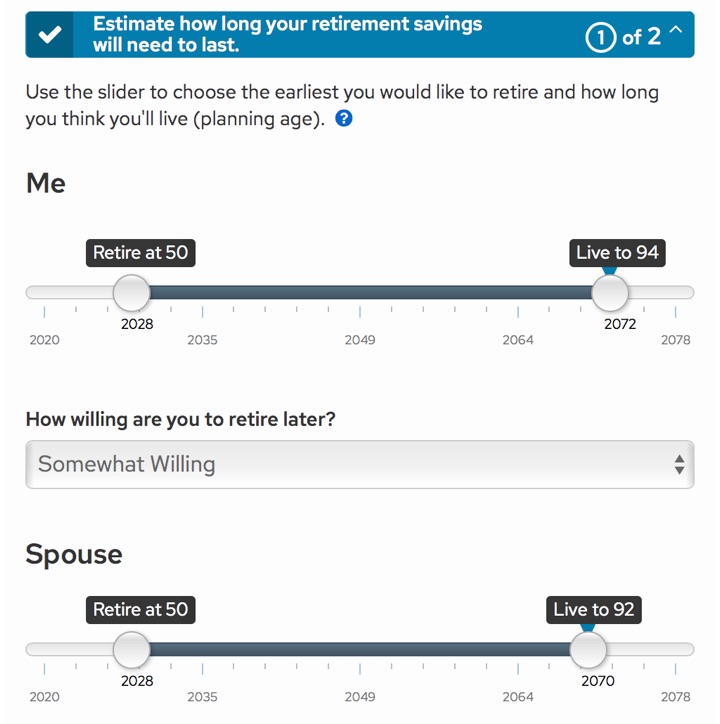

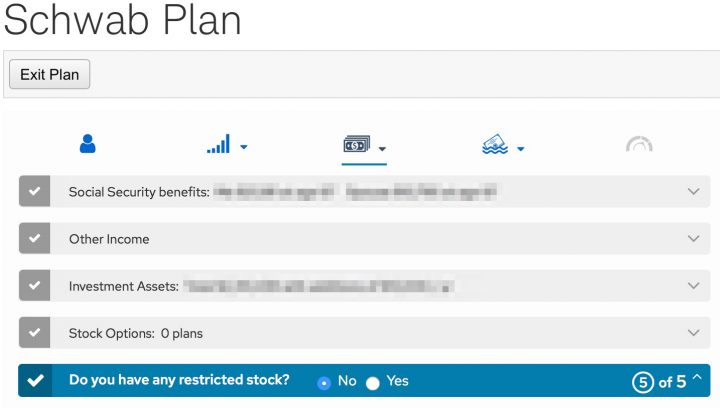

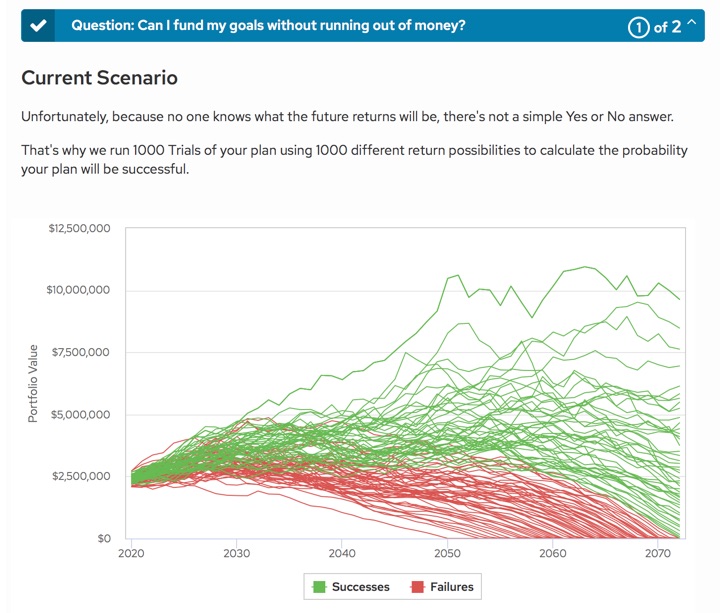

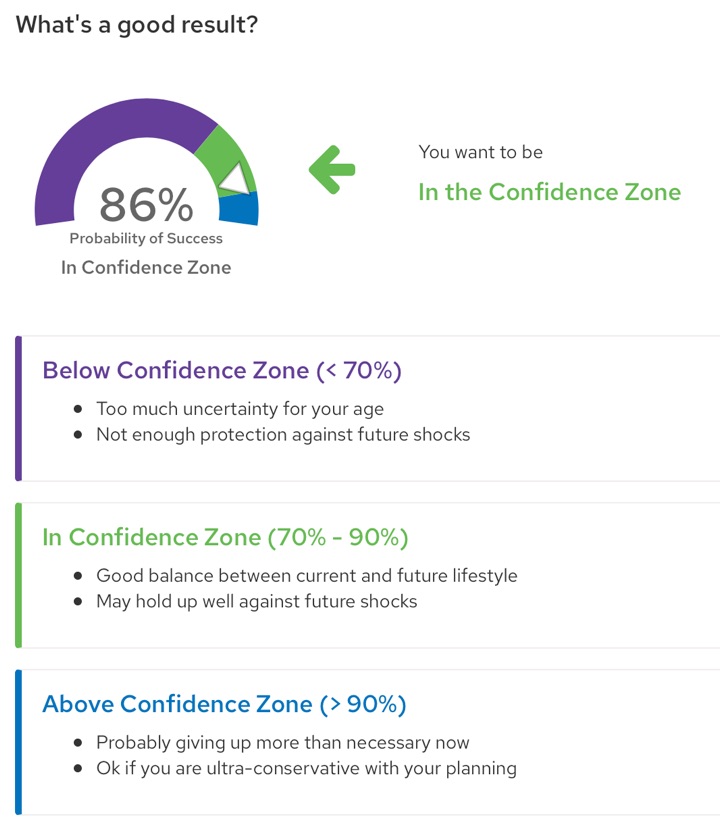

Schwab has rolled out a new digital financial planning tool called

Schwab has rolled out a new digital financial planning tool called

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)