Here’s a good question from reader Elizabeth in response to yesterday’s post about buying Treasury bonds on the open secondary market:

One thing I’m interested in is on that same table you shared – Corporate bonds rated BBB are around 6% for 5 years. Can you write about this? What are the pros and cons?

Here’s my thought process. Yes, us “retail” investors can also buy individual corporate bonds via major brokers with a fixed income desk like Fidelity. (Bond trading is rare on newer trading apps like Robinhood.) The bonds are judged by various rating agencies and usually separated by their grading. Right now, I see a Moody’s BAA3-rated corporate bond with 5 years left until maturity paying 6.78% interest (click to enlarge):

However, corporate bonds are not within my circle of knowledge. The special thing about every single US Treasury bond is that they are all fully-backed by the US government. Same with an FDIC-insured bank CD or NCUA-insured credit union certificate. It’s like comparing all 16 oz. jars of JIF brand peanut butter; I know all of them are the same, so I can just buy on price.

Once you venture into the world of corporate bonds, things get a lot more complicated. There is wide range of potential credit risk from the issuing company. If the company fails, you may not receive your initial principal back. There is call risk from callable bonds where the issuer can redeem your bond early (to their benefit), not to mention several other early redemption wrinkles like “make whole call”, “sinking fund protection”, and “special optional redemptions”.

Baa3 and BBB- rated bonds are still technically “investment-grade”, but they are just one notch above “below investment-grade”, aka “junk”, aka “high-yield” bonds. Here is a quick table of bond ratings from Investopedia:

If take a closer look at the available bonds above, you’ll see that only one bond is paying over 6.7% and it doesn’t even have an S&P rating, which means there might be something funny going on. The rates quickly go back down to the 5.XX% range.

Do I know why one bond has to pay 6.7% interest rate to entice a buyer, while another one only has to offer 4.8%? I must admit that I really have no idea.

Bonds are for safety. In addition, I should remember my reason for holding bonds. They are my safety blanket. They are my next 10 years of expenses that are guaranteed to be there even if bad things happens. What if Russia bombed a NATO country tomorrow? The US would be obligated to go to war. China might then feel that it has to back Russia. Who knows. Hope for the best. Prepare for the worst.

My goal with bonds is to maximize yield without sacrificing safety.

Stocks are for growth and upside potential. Let’s take the bottom bond highlighted – an Ally Financial corporate bond paying 5.6% yield for the next 5 years. Ally Bank is familiar to me, and I am a longtime customer. Why not buy that bond? Well, if I bought that bond, the most that it will ever pay me back is the bond face value and interest. Worst case is still that Ally goes bankrupt and I lose all or most of my entire investment and end up with zero. This has happened, and to much larger companies than Ally.

Up to 6 days before their eventual collapse, Lehman Brothers had an A investment grade rating. The eventual recovery on their bonds was 21 cents on the dollar.

However, I could also buy Ally Financial stock (ticker ALLY). Right now, it is trading at only a 4.72 P/E ratio and is even paying a dividend yield of 3.54%. Five years from now, I could be sitting on a +50% or +100% or +200% total return. In other words, if you want to take on risk for a higher return, you are competing with stocks. There is ongoing debate about the inclusion of high-yield bonds in a portfolio, but I prefer to take risks with stocks and keep my bonds as safe as possible.

Consider a low-cost, diversified mutual fund or ETF. The benefit of holding riskier corporate bonds inside a mutual fund/ETF is that any one corporate bankruptcy won’t wipe you out. You can be diversified across hundreds of companies. Now, you can’t control the maturity as tightly, you’ll still lose some yield to management costs, and you’re still subject to interest rate risk. If you own the Vanguard Total Bond Market ETF (BND) or any Vanguard Target Retirement Fund, you already own corporate bonds inside a fund.

If I had to buy corporate bonds and wanted a stream of higher income without a reckless amount of credit risk, I would consider the Vanguard High-Yield Corporate Fund Investor Shares (VWEHX, $3k min) or Vanguard High-Yield Corporate Fund Admiral Shares (VWEAX, $50k min). VWEHX has a 0.23% expense ratio and a 30-day SEC yield of 6.71% as of 07/18/2022. VWEAX has a 0.13% expense ratio and a 30-day SEC yield of 6.81% as of 07/18/2022.

You are buying a basket of nearly 700 bonds that straddle the line between investment-grade and below investment-grade. This is a bond fund that I would own for the income stream, not if I needed the entire amount in cash soon as it can drop quite a lot during times of market stress. The expense ratio on this Vanguard fund is much lower than the industry average. Just a suggestion for further research. I don’t own this fund. In fact, I don’t own any corporate bonds at all.

Hope that helps!

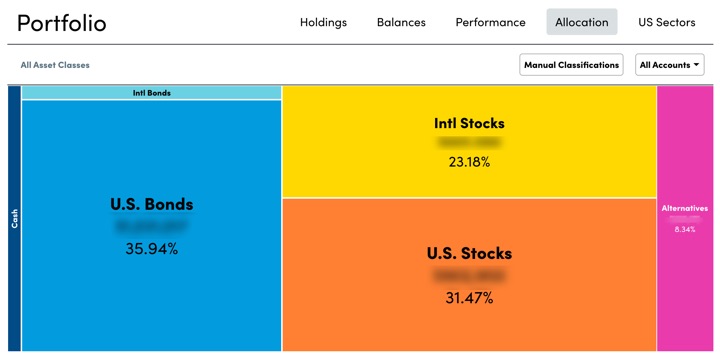

Here’s my quarterly update on my current investment holdings as of 7/8/22, including our 401k/403b/IRAs and taxable brokerage accounts but excluding real estate and side portfolio of self-directed investments. Following the concept of

Here’s my quarterly update on my current investment holdings as of 7/8/22, including our 401k/403b/IRAs and taxable brokerage accounts but excluding real estate and side portfolio of self-directed investments. Following the concept of

Inside various financial forums, I am seeing the “anyone else worried?” 😓 posts as most portfolios are down double-digits. For a retiree with a $1 million portfolio, seeing $100,000 or $200,000 of value evaporate is understandably stressful. However, much of this is because you are comparing to your portfolio’s all-time high, or high-water mark, which is a relatively arbitrary number. Just because at one moment in time, there were a few willing buyers of your assets for a given price doesn’t mean you should anchor yourself to that number.

Inside various financial forums, I am seeing the “anyone else worried?” 😓 posts as most portfolios are down double-digits. For a retiree with a $1 million portfolio, seeing $100,000 or $200,000 of value evaporate is understandably stressful. However, much of this is because you are comparing to your portfolio’s all-time high, or high-water mark, which is a relatively arbitrary number. Just because at one moment in time, there were a few willing buyers of your assets for a given price doesn’t mean you should anchor yourself to that number.

Inflation (and thus I Bonds) 🚀🚀🚀! Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.

Inflation (and thus I Bonds) 🚀🚀🚀! Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)