Tax-advantaged 401k and 403b plans can help you save for retirement, but did you know that you’re probably paying for all the costs of this “employee benefit”? 76% of large employers have workers pick up all the costs of 401(k) administration, according to a recent Forbes article Creative Ways to Cut Your 401(k) Fees. The tab is often quietly paid via high-fee mutual funds (which in turn kick back money to the administrator). The article also focuses on brokerage windows, an “escape hatch” that allows employees to move their funds into a self-directed account with a many more investment options. Their availability is growing:

What is the catch? These self-directed plans have their own set of fees, notably annual maintenance fees and transaction fees. While regular 401(k) plan options may be limited and more expensive on a percentage basis, they usually don’t charge transaction fees each time you buy or sell. For this reason, brokerage windows tend to work better people with larger account balances. With bigger trade sizes, a flat commission is only a small percentage of the total amount involved.

We recently gained access to Schwab’s brokerage window, called the Personal Choice Retirement Account (PCRA). The mechanics were pretty simple. After completing a special application, you could sell a portion (or all) of your existing investments and transfer them into a “Schwab PCRA” bucket. That money then shows up into your linked account at Schwab.com, where you do all your trades.

Commission Schedule and Available Mutual Fund List. Here is the PCRA fee schedule and PCRA mutual fund availability list that was provided to me by Schwab. (I am assuming these documents are the same across all PCRA plans, but I could be wrong. As I’ll explain shortly, just because something is listed does not mean it is available to everyone.)

The commission schedule is pretty similar to what is available in their standard brokerage account. $8.95 ETF and stock trades, $0 trades for Schwab ETFs. No commission on their No-Transaction-Fee mutual fund list (funds have to pay to be on the list), otherwise $50 to buy and $0 to sell. Schwab PCRA does not charge any annual account or maintenance fees, but your Retirement Plan Service Provider may charge account maintenance fees or some form of “recordkeeping fees”. In our case, there is a $50 annual account fee.

The mutual fund list is quite extensive. Let’s say I was trying to buy the Vanguard REIT ETF (VNQ). I searched and found two results:

The big caveat in my particular case: ETF and stock trades were not allowed at all. I still tried to make a purchase but got this message:

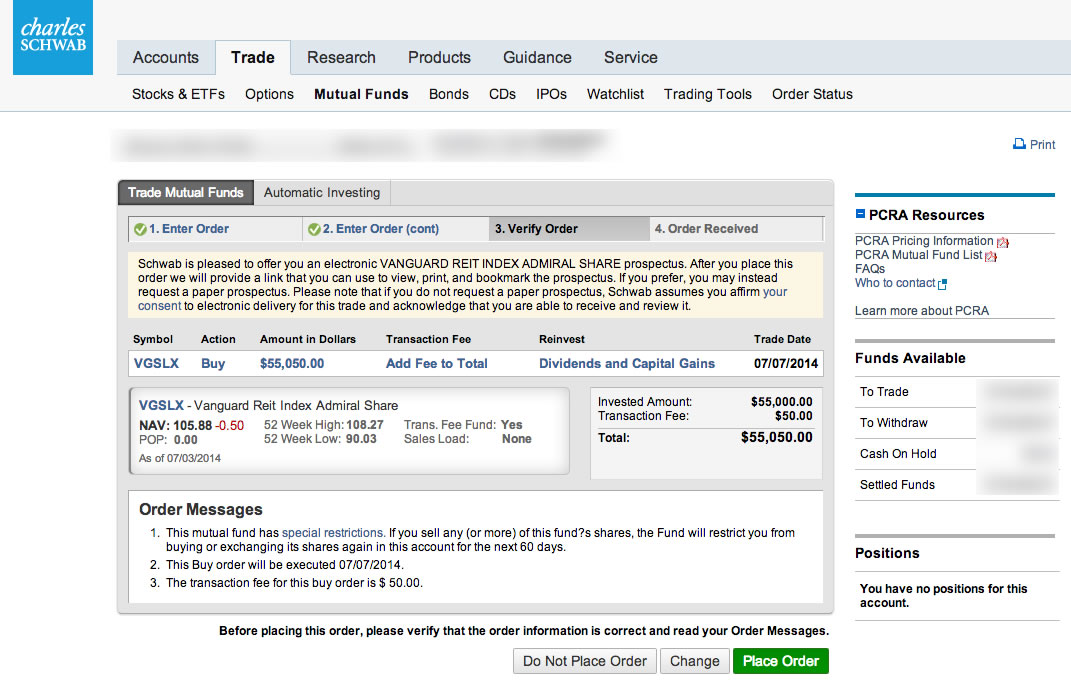

From the fee schedule, I assume that some PCRA plans will offer this feature. But in my case, I had to be satisfied with buying the Vanguard REIT mutual fund (VGSIX) and paying $50 per buy trade. The good news is that I was able to buy Admiral Shares (VGSLX) which has the same expense ratio (0.10%) as the ETF version ($10,000 minimum).

Should I use my brokerage window? According to this Money article, just 5.6% of 401(k) investors opt for a brokerage window even with it is offered. The Schwab PCRA has worked out well for me as an alternative to my standard 401k investment options, but only because a few things aligned:

- My balance was big enough. Paying $50 a year and $50 per trade is only worth it when your balance is big. Let’s say my balance is $100,000. $50 is only 0.05% of $100,000. If I am saving over 0.05% in expense ratios every single year in exchange, that is a great deal. But $50 is a full 1% of a $5,000 balance.

- There was a better option in the brokerage account. For example, the S&P 500 index fund in my 401k standard menu charges 0.30% annually, while I can access a Schwab S&P 500 index fund at only 0.09% annually. In my case, I wanted cheap access to the REIT asset class which I didn’t have otherwise. Only about 25% of 401k plans offer access to an REIT fund.

- I don’t trade too frequently. $50 a pop adds up, so I intend to accumulate money in the normal account, and then transfer over a chunk of money once a year to my Schwab PCRA. This way my bi-weekly contributions are invested for free, and I limit my $50 Schwab trades to once or twice a year.

Papa John’s sent me a code for a free song download the other day. It was really a way to introduce me to the

Papa John’s sent me a code for a free song download the other day. It was really a way to introduce me to the  Many stores offer a “low price guarantee” but in reality nobody actually uses them. You have to find the competing price yourself, wait in the returns line, all for the opportunity to argue with the cashier about the validity of your claim. Who wants to do that?

Many stores offer a “low price guarantee” but in reality nobody actually uses them. You have to find the competing price yourself, wait in the returns line, all for the opportunity to argue with the cashier about the validity of your claim. Who wants to do that? Low-cost index ETF portfolio are everywhere these days! Covestor is a site that usually charges you a fee to manage your portfolio to follow various active managers, with fees ranging up to 2% per year (split Covestor/manager 50/50). However, they recently introduced their

Low-cost index ETF portfolio are everywhere these days! Covestor is a site that usually charges you a fee to manage your portfolio to follow various active managers, with fees ranging up to 2% per year (split Covestor/manager 50/50). However, they recently introduced their  Another online ETF portfolio advisor joins the mix. Discount brokerage

Another online ETF portfolio advisor joins the mix. Discount brokerage

Wouldn’t a Netflix for books be neat? You could borrow all the books that you wanted to read and then return them when you’re done. Oh wait, they already invented it and called it a library.

Wouldn’t a Netflix for books be neat? You could borrow all the books that you wanted to read and then return them when you’re done. Oh wait, they already invented it and called it a library.

Online portfolio manager Betterment recently rolled out a new Retirement Income feature that will help you withdraw money from your nest egg. Unfortunately, even though I have a Betterment account I couldn’t test it out directly as it is currently only available to customers with a $100,000+ balance that have designated themselves as retired. But through a combination of reading through their website materials, press releases, blog posts, as well as asking an employee specific questions, I was able to get a good idea of how this feature works.

Online portfolio manager Betterment recently rolled out a new Retirement Income feature that will help you withdraw money from your nest egg. Unfortunately, even though I have a Betterment account I couldn’t test it out directly as it is currently only available to customers with a $100,000+ balance that have designated themselves as retired. But through a combination of reading through their website materials, press releases, blog posts, as well as asking an employee specific questions, I was able to get a good idea of how this feature works.

TaxACT Online

TaxACT Online  H&R Block at Home Online

H&R Block at Home Online  (See also:

(See also:  The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)