I just finished filing my federal and state income tax returns (again) using TurboTax Deluxe Online edition. This is the 2nd part of my series comparing the three major tax preparation websites: TurboTax, TaxACT.

You can see my TaxACT 2011 review here.

Tax Situation

Again, here’s a quick summary of our personal tax situation.

- Married filing jointly, subject to state income tax

- Both with W-2 income, as well as self-employed income (Schedule C).

- Interest income and dividend income from bank accounts, stocks, and bonds (Schedule B).

- Contribute to retirement accounts (401ks and IRAs).

- Capital gains and losses from brokerage accounts (Schedule D).

- Itemized deductions (Schedule A), including mortgage interest and charitable giving.

Retail Price

Although their website shows a “retail” price of $49.95 for TurboTax Deluxe, anyone who visits the site will at most pay $29.95 for Federal including e-File. TurboTax State is $36.95 including e-file. If you are a Vanguard Flagship Services or Asset Management Services client, you get a TurboTax Online Federal Deluxe + State + efile for free. All other clients get discount of about 25% off; you must log in to get your discount. There is also a free edition available if you have a very simple tax return – no itemized deductions, investment income, but remember that State is $27.95 extra in that case.

TurboTax Premier offers “additional guidance” for investment income from stocks and bonds and also rental income. However, I had the usual stock and bond sales and was able to complete my return without upgrading to Premier. I did not feel I needed any extra guidance, but if you do it will run an extra $20 for a total of $49.95. Finally, TurboTax Home & Business ($74.95) offers “additional guidance” for self-employment income including dealing with business expenses. However, if all you have is a couple of 1099-MISCs to report as I did, you can get by with Deluxe.

User Review

With all these tax sites you can start your return for free, and only pay when you file. Since I had already input all my tax data into TaxACT.com, I simply opened that up in a web browser tab side-by-side and start filing things out. The Q&A interview questions are in roughly the same order, but there are enough differences to make you jump around a bit.

Import from TaxACT & H&R Block at Home

Last year, I used TurboTax for my tax return. Thus, this time around TurboTax had all my old tax info pulled up immediately. Filing status, dependents, address, DOB, SSN, etc. They also had all my old W-2 and 1099 providers to reduce my data entry needs a little bit more. For example, all my Employer Tax IDs and addresses were pre-filled. This did feel rather convenient, and it helped make sure I didn’t forget any 1099s from old bank accounts.

However, as a result I was never asked if I wanted to import a previous year’s return from another provider like TaxACT or H&R Block. Perhaps someone can shed some light on this in the comments?

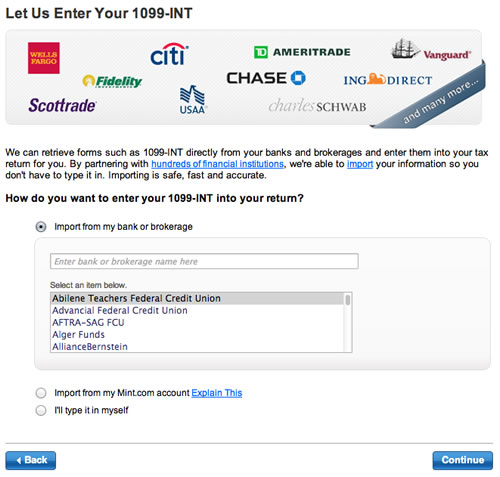

W-2 and 1099 Direct Import from Providers

One of the strengths of TurboTax is that you can directly import your W-2 and 1099 information from a number of partner providers. However, the W-2 part didn’t really impress me. Our W-2s came from Ceridian and we had to enter some sort of username and password which I’ve never set up before. It was faster to just type in the 10 numbers and get on with it.

1099s were a different story, at least for me. I was able to provide my Vanguard username and password and have my 1099-INT, 1099-DIV, and 1099-B data imported in seconds. Other partners that I was able to use included Betterment, Chase Bank, Capital One 360 (Sharebuilder), and Pentagon Federal Credit Union. USAA, TD Ameritrade, E-Trade, and Wells Fargo were also available. For those with a lot of transactions, this is a great time-saver.

In addition, after comparing with my TaxACT data, I found that I had made a data entry error of $300 with one wrong digit when manually entering all those capital gains and losses from stock sales. The TurboTax import would have help me avoided that mistake, which I don’t think I would have caught otherwise.

Finally, a cool feature is that if all your accounts are linked to the aggregation site Mint.com, you can simply log into your Mint account and have all your available forms imported with one login (Intuit owns both TurboTax and Mint).

The Small Stuff

This time around, I did notice that TurboTax has something called “Flags” that are the same as Bookmarks with TaxACT that allow you to mark confusing questions to come back to. The icon is small and there is no text, so I probably would have missed it again if I wasn’t looking for it. A minor positive I noticed is that TurboTax automatically enters commas when you reach thousands (ie. 3,459 instead of 3459). It helps with data entry, as I have already shown that I am error-prone!

A minor negative is that TurboTax had many more server delays where the page would not load or would be blank and I had to refresh the page. I did not have any such problems with TaxACT, which I was using simultaneously on the same internet connection and computer.

Foreign Tax Credit

After everything was entered, there was a difference of less than $50 in my total calculated refund between TurboTax and TaxACT. After some research, I found that it was due to my treatment of my foreign taxes paid as a deduction vs. credit. TaxACT appeared to be more aggressive and just allowed me to take it as a credit, while TurboTax seemed to require more information and otherwise steered me towards taking it as a deduction. This was partially my own fault, but the two questionnaires definitely had a different approach. In the end, I got everything to match up between them. (Take the credit if you can.)

Upselling and Price Tricks?

There are some upsell attempts during the tax return to upgrade to Premier or Home & Business, however it was only a couple times and didn’t feel overly pushy. At the end, the price total was as expected with no bogus charges. There was a final pitch for a product call Audit Defense for $39.95, which provides you “professional representation in the event of an audit” and covers both federal and state returns. As before, I am not convinced of the quality of such representation.

Recap

Turbotax showed why it remains the best-known and popular tax software. That is, it covers all of the tax aspects about as equally as well as the others, perhaps with a bit more thoroughness (anality?). However, where it separates itself is the importing of data from financial institutions. It is indeed more expensive – for most people TurboTax will cost $30+ more than TaxACT but if it saves you both time and effort in data entry (and potentially prevents errors), then I can definitely see how people would be willing to pay a premium.

There is also the familiarity factor. I definitely kept feeling the benefit of using it last year and again this year. It compared all my 2010 and 2011 numbers side-by-side, which was nice for us financial geeks. It also remembered little things like my old IRA basis, so I wouldn’t have to look it up again. On the other hand, if my return was simple and would not benefit much from automatic importing, I would probably rather stick with TaxACT.

OptionsXpress.com (OX) is a online brokerage site that specialized in options and futures trading, but has since expanded their offering to be one-stop-shop – offering stocks, bonds, brokered CDs, and mutual funds. Like some of you, I signed up a while back when they were offering a fat bonus (very limited-time offer). Since I have an account, here’s a user’s review of the broker.

OptionsXpress.com (OX) is a online brokerage site that specialized in options and futures trading, but has since expanded their offering to be one-stop-shop – offering stocks, bonds, brokered CDs, and mutual funds. Like some of you, I signed up a while back when they were offering a fat bonus (very limited-time offer). Since I have an account, here’s a user’s review of the broker.

OptionsXpress has a current promotion offering new customers a $100 bonus if they open an account with at least $500 and make 3 trades with a year.

OptionsXpress has a current promotion offering new customers a $100 bonus if they open an account with at least $500 and make 3 trades with a year.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)