Update 11/3/13: The new rates for November 2013-April 2014 are 0.20% fixed and 1.18% variable. See details here.

Update 11/3/13: The new rates for November 2013-April 2014 are 0.20% fixed and 1.18% variable. See details here.

Savings I-Bonds September/October 2013 Rate Speculation

Posted on October 31, 2013 // 19 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.Last updated: November 3, 2013

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Savings I-Bonds May 2013 Upcoming Rate: 1.18%

Posted on April 16, 2013 // 8 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.New inflation numbers for March 2013 were just announced, so it’s time for the usual semi-annual update and rate predictions.

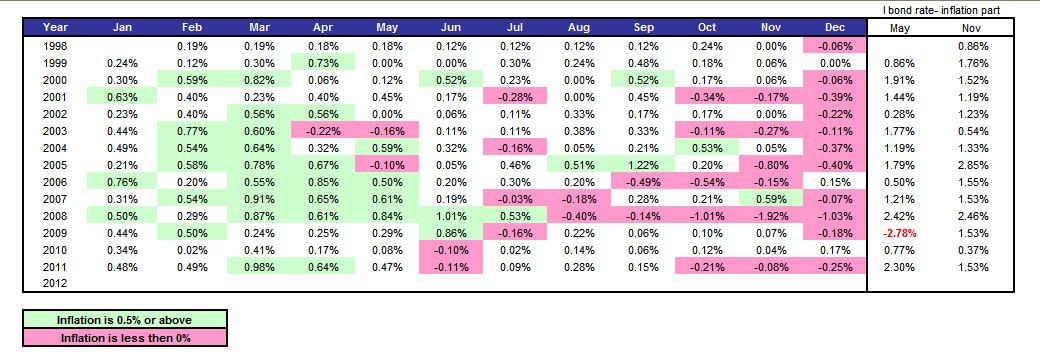

New Inflation Rate

September 2012 CPI-U was 231.407. March 2013 CPI-U was 232.773, for a semi-annual increase of 0.590%. Using the official formula, the variable component of interest rate for the next 6 month cycle will be approximately 1.18%. The new fixed rate is nearly guaranteed to be zero, so the total rate will be 1.18% as well. If you have an older savings bond, your fixed rate may be different.

Purchase and Redemption Timing Reminder

You can’t redeem until 12 months have gone by, and any redemptions within 5 years incur an interest penalty of the last 3 months of interest. A known “trick” with I-Bonds is that if you buy at the end of the month, you’ll still get all the interest for the entire month as if you bought it in the beginning of the month. It’s best to give yourself a few business days of buffer time though, since if you wait too long your effective purchase date may be bumped into the next month.

Buying in April

If you buy before the end of April, the fixed rate portion of I-Bonds will be 0.0%. You will be guaranteed the current variable interest rate of 1.76% for the next 6 months, for a total rate of 0 + 1.76 = 1.76%. For the 6 months after that, the total rate will be 0.0 + 1.18 = 1.18%. Let’s say we hold for the minimum of one year and pay the 3-month interest penalty. If you buy on April 30th and sell on April 1, 2013, you’ll earn a 1.28% annualized return for an 11-month holding period, for which the interest is also exempt from state income taxes. This is better than any 1-year bank CD that I can find right now, keeping in mind the liquidity concerns and the purchase limits. If you hold for longer, you’ll be getting the full 1.47% over the first year.

Given the combination of current low rates and the fact that you lose the last 3 months of interest (again, for holding less than 5 years), it might be better to wait long enough to grab 12 full months of interest by holding for 15 months (14 buying late). If you buy on April 30th and hold until July 1st, 2014, you’d achieve a annualized return of ~1.26% over 14 months. After that, you can see what the new rates are and decide whether to keep holding them.

Buying in May

Last updated: August 9, 2018

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Savings I Bonds September/October 2012 New Rate 1.76%

Posted on October 17, 2012 // 9 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.New inflation numbers were just released for September 2012, so here’s the usual semi-annual update.

New Inflation Rate

March 2012 CPI-U was 229.392. September 2012 CPI-U was 231.407, for a semi-annual increase of 0.88%. (CPI-U increased 2.0% over last 12 months.) Using the official formula, the variable interest rate for the next 6 months will be approximately 1.76%.

Purchase and Redemption Timing Tips

You can’t redeem savings bonds until after 12 months, and any redemptions within 5 years incur a interest penalty of the last 3 months of interest. A known “hack” with I-Bonds is that if you buy at the end of the month, you’ll still get all the interest for the entire month. It’s best to give yourself a little buffer time though, as if you wait too long your effective purchase date will be bumped into the next month.

Buying in October

If you buy before the end of October, the fixed rate portion of I-Bonds will be 0%. You will be guaranteed an variable interest rate of 2.20% for the next 6 months, for a total rate of 0 + 2.20 = 2.20%. For the 6 months after that, the total rate will be 0.0 + 1.76 = 1.76%. Let’s say we hold for the minimum of one year and pay the 3-month interest penalty. If you buy at the end of October 2012 and sell at the beginning of October 2012, you’ll earn a 1.68% annualized return for an 11-month holding period, although you may want to hold it longer if the rates stay higher than that of other available safe investments. This is much better than any 1-year FDIC-insured bank CD available right now, keeping in mind the lack of early withdrawals and purchase limits.

Given the combination of current low rates and the fact that you lose the last 3 months of interest (again, for holding less than 5 years), it might be better to wait long enough to grab 12 full months of interest by holding for 15 months (14 month holding period if buying late). If you buy at the end of October and hold until January 1st, 2014, you’d achieve a annualized return of ~1.70% over 14 months. After that, you can see what the new inflation rates are and decide whether to keep holding them.

Buying in November

If you wait until November, you will get a new unknown fixed rate + ~1.76% for the first 6 months, and an unknown rate based on ongoing inflation after that. Based on the current market rates of Treasury Inflation-Protected Securities (TIPS), it is almost certain that the new fixed rate will remain zero. So you’ll get 1.75% for 6 months for certain. My personal opinion is that you might as well lock on the guaranteed above-market rates for 12 months by buying in October instead of buying in May. If rates spike, you’ll eventually get the benefit of any higher rates eventually in the future anyway.

Existing I-Bonds

If you have an existing I-Bond, the rates reset every 6 months (depending on your purchase month). Your bond rate = your specific fixed rate + variable rate. Even at a low or even zero fixed rate, your existing savings bonds are paying much more than current savings accounts and will continue to be hedged against inflation, so weigh carefully whether or not to redeem them.

Annual Purchase Limits

The annual purchase limit is now $10,000 in online I-bonds per Social Security Number. For a couple, that’s $20,000 per year. Buy online at TreasuryDirect.gov, after making sure you’re okay with their security protocols and user-friendliness. If you have children, you may be able to buy additional savings bonds by using a minor’s Social Security Number.

For more background, see the rest of my posts on savings bonds. I’m keeping all of mine for the foreseeable future, due to their tax deferral possibilities and other unique advantages. Compare the rates on these savings bonds to what you’re earning on your FDIC-insured bank deposits or even your TIPS and bond mutual funds, and you may find them a good addition to your portfolio.

Last updated: August 9, 2018

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Savings I-Bonds March/April 2012 New Rate Prediction: 2.21%

Posted on April 17, 2012 // 19 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.New inflation numbers for March 2012 were announced on April 13th, so it’s time for the usual semi-annual update and rate predictions.

New Inflation Rate

September 2011 CPI-U was 226.889. March 2012 CPI-U was 229.392, for a semi-annual increase of 1.1032%. Using the official formula, the variable interest rate for the next 6 months will be approximately 2.21%, depending on the upcoming fixed rate announcement (although really it’s highly unlikely to be anything but zero).

Purchase and Redemption Timing Tips

You can’t redeem until 12 months have gone by, and any redemptions within 5 years incur a interest penalty of the last 3 months of interest. A known “trick” with I-Bonds is that if you buy at the end of the month, you’ll still get all the interest for the entire month as if you bought it in the beginning of the month. It’s best to give yourself a few business days of buffer time though, since if you wait too long your effective purchase date may be bumped into the next month.

Buying in April

If you buy before the end of April, the fixed rate portion of I-Bonds will be 0.0%. You will be guaranteed the current variable interest rate of 3.06% for the next 6 months, for a total rate of 0 + 3.06 = 3.06%. For the 6 months after that, the total rate will be 0.0 + 2.21 = 2.21%. Let’s say we hold for the minimum of one year and pay the 3-month interest penalty. If you buy on April 30th and sell on April 1, 2013, you’ll earn a 2.27% annualized return for an 11-month holding period, for which the interest is also exempt from state income taxes. This is better than any 1-year bank CD that I can find right now, keeping in mind the liquidity concerns and the purchase limits.

Given the combination of current low rates and the fact that you lose the last 3 months of interest (again, for holding less than 5 years), it might be better to wait long enough to grab 12 full months of interest by holding for 15 months (14 buying late). If you buy on April 30th and hold until July 1st, 2013, you’d achieve a annualized return of ~2.26% over 14 months. After that, you can see what the new rates are and decide whether to keep holding them.

Buying in May

If you wait until May, you will get a new unknown fixed rate plus 2.21% for the first 6 months. I would bet my own money that that the fixed rate will be 0.0% again (any takers?), given current real yields for TIPS. The next 6 months will be based on an unknown rate based on future inflation. If there is high inflation for the next 6-month period, this may get you a higher rate sooner, but buying in April will eventually get you the same rate anyway.

My personal opinion is that you might as well lock on the guaranteed above-market rates for 12 months by buying in April instead of buying in May. You could always wait all the way until in October for the next rate announcement, but if you have the cash now you’ll have the opportunity cost of lower rates until then.

Low Purchase Limits

The annual purchase limit is now $10,000 in online I-bonds per Social Security Number. For a couple, that’s $20,000 per year. Buy online at TreasuryDirect.gov, after making sure you’re okay with their security protocols and user-friendliness.

For more background, see the rest of my posts on savings bonds. I’m keeping all of mine for the foreseeable future, due to their tax deferral possibilities and other unique advantages. Compare the rates on these savings bonds to what you’re earning on your FDIC-insured bank deposits, and you may start hoarding them like me.

Last updated: August 9, 2018

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Savings Bonds vs. Bank Savings Accounts

Posted on January 27, 2012 // 16 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.(In this post, I’m not going to provide all the background information on savings bonds that I normally do. For that, please read the older posts in my Savings Bonds category.)

When the Treasury announced the $10,000 purchase limit for 2012, a few readers asked if you should buy savings bonds in January, or wait until later in the year. Since then, a few things have happened. For one, the Federal Reserve has basically said that they will keep their target fed funds rates at zero until late 2014, while setting a target inflation rate at 2% annually. Translation: Interest rates on savings accounts and similar products will be remain crap while the things we buy get more expensive.

Also, we have another month’s worth of Consumer Price Index (CPI) data which is how the inflation rate is defined for savings bonds. The next 6-month variable rate update will be based on the CPI-U change between September 2011 and March 2012. We are halfway there:

CPI-U

Sep 2011 226.889

Oct 2011 226.421

Nov 2011 226.230

Dec 2011 225.672

Jan 2012 ?

Feb 2012 ?

Mar 2012 ?

You can see that inflation is actually negative over these three months. However, user MoneyOCD of Bogleheads posted this informational chart showing that in recent years there have been many periods of negative inflation from September to December, only to be followed by periods of higher inflation from December to March.

Basically, making predictions now is premature. If you buy in January through April, you will get a fixed rate of 0%, and a variable rate of 3.06% for six months. Given the interest rate environment, this is pretty much one of the best options for “safe” money. If you wait all the way until May, you’ll get something new based on whatever happens to inflation the next few months along with a fixed rate that will most likely be zero again. The inflation rate resets every 6 months based on your purchase month.

In general, if you have the money and are looking to put it in shorter-term, low risk investments that are guaranteed not to lose money (in terms of face value), I would be maxing out my limit on savings bonds for 2012. Keep in mind that savings bonds can’t be cashed in for an entire year after purchase. My personal opinion on the short-term? I don’t see any benefit in waiting until May. If you have money to put aside now, buy Series I savings bonds now. If you don’t, just wait until you do. The rate is already higher than savings accounts or 1-year CDs, and by waiting around in a 0.75% savings account or 1-year CD you’ll be missing out in interest.

If you’re looking to buy in January, I’d put in your order today at TreasuryDirect. It’s better to buy near the end of the month, as you get credit for the entire month no matter if you buy at the beginning or the end.

Last updated: January 27, 2012

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

TreasuryDirect Electronic Savings Bond Purchase Limit Now $10,000 Annually

Posted on January 5, 2012 // 12 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.The Treasury announced today 1/4 that the annual purchase limit for electronic U.S. savings bonds bought at TreasuryDirect is now $10,000 per series, per person. I’m not sure why they waited so long to decide this, given that it’s been six months since they announced that they would will no longer sell paper U.S. savings bonds through banks and other financial institutions in 2012. Thanks to reader JR for the heads up.

Under the new rules, an individual can buy a maximum of $10,000 worth of electronic savings bonds of each series in a single calendar year, or a total of $20,000. Since 2008, investors could buy a maximum of $5,000 in each series and in each form (paper or electronic). So a single owner could buy $20,000 in one year. As of January 1, 2012, paper bonds are no longer being sold through financial institutions. With today’s announcement, the total amount an individual can purchase in online savings bonds in one calendar year is $20,000. An investor still can purchase up to $5,000 annually in Series I paper savings bonds using his/her tax refund and IRS Form 8888.

This also means that you could theoretically buy $10,000 electronically and $5,000 in paper bonds in 2012. However, another weird glitch on IRS Form 8888 [pdf] is per the directions, the total amount bought on that form cannot exceed $5,000 – whether you file single or married filing jointly. So a married filing joint couple can only buy $5k between the both of them, while two single filers can get $5k each. Boo.

The Finance Buff has a nice post about what he calls the backdoor to paper savings bonds regarding overpaying your taxes on purpose. Basically, you do your taxes, then file an extension with payment included in order to make sure you have a $5k refund amount, and shortly afterward file your taxes. Supposedly tax software like TurboTax supports Form 8888, so it’s not even necessary to file using paper forms.

Last updated: January 5, 2012

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Treasury Direct Review: Electronic Savings Bond Security Concerns

Posted on December 28, 2011 // 33 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.Despite the Treasury’s obvious dislike for the small investor, Series I Savings Bonds still offer a relatively good interest rate. As of January 1st, 2012, you will no longer be able to buy paper savings bonds other than a small window using your tax refund. The only option left is buying electronic savings bonds via TreasuryDirect.gov. This brings me to the following reader question:

Was just reading Mel Lindauer’s comments in the Bogleheads forum about I-Bonds and the trouble with Treasury Direct. Seems a great many folks hate the system to the point that they would rather not use it. 2012 is/was to be the year that I first began purchased I-Bonds, having finally got to the point of maxing out all other tax deferred and tax free methods. Now I am not so sure…what is your experience with TD?

First, let’s get to what I see as the main reason why most people choose not to use the online service at TreasuryDirect (TD). TD is not a bank and does not fall under Regulation E and the Electronic Fund Transfer Act that establishes consumer protections for loss or theft of money from your account.

If your paper savings bonds are stolen or lost, the Treasury has a process in place to reclaim your bonds. However, if somehow your electronic savings bonds were stolen, you would stuck with the loss with no liability from TD. It doesn’t seem to make sense, but it’s true.

So what do you do? The easiest thing to do is not use TreasuryDirect. But it remains a good investment, so in my case I looked into what security measures were in place to prevent such theft. In November 2011, TD instituted some security changes to their login process. What would a thief have to do in order to cash in your savings bonds?

- They need your account number, which is more like Z-12345678 as opposed to johnsmith.

- When you login with a new computer, a one-time passcode will be sent to your e-mail address. So, they would need to have access to your e-mail address as well. You can choose to register your computer for future visits if you like, but it would seem safer not to do so. I don’t log into TD very often so my cookie expires anyway by the time I log in again. This means a unique code is sent every single time I log in.

- They would also need your account password. I would hope your e-mail password and your TreasuryDirect password are different. In any case, it’s harder for viruses or keylogger programs to record your password because you must enter it using a virtual keyboard (unless you circumvent it by disabling Javascript).

- Now, at this point they have online access to your account and can see your balances. But to cash out a bond, first you must answer a security question (mom’s maiden name, etc.). More importantly, you can only cash out a bond to a linked bank account. So the thief would need access to your bank account (…which is protected by Regulation E mentioned above!)

- Alternately, they would need to send in a paper form adding an alternate bank account under their control. However, the name on the bank account must match the name on the TD account, and the form requires a Medallion Signature Guarantee where a third party checks official ID for identity verification. The TD website itself has improved over the years so that any small change (bank addition, profile change) results in a e-mail notice.

Personally, I deemed it exceedingly unlikely for an actual theft to occur and made the decision to go ahead and use the website. My holdings there are significant, but under 5% of total net worth. I know that others have also had technical issues with accessing their account, but I have not experienced anything like that. In the end, TreasuryDirect definitely has its flaws, and I would not fault someone for not using it as a result. You have to weight the risks and benefits for yourself.

Last updated: December 28, 2011

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

TreasuryDirect.gov Security Login Changes 2011

Posted on November 8, 2011 // 28 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone. TreasuryDirect.gov is the official US Treasury website that allows individuals to directly buy securities online, including savings bonds and Treasury bonds. The problem is that they don’t want to take any responsibility for unauthorized access to your account, including reported fraud and theft, which actually makes them less consumer-friendly than even those evil megabanks. In the past, they figured the problem would be best solved with a series of clunky security measures.

TreasuryDirect.gov is the official US Treasury website that allows individuals to directly buy securities online, including savings bonds and Treasury bonds. The problem is that they don’t want to take any responsibility for unauthorized access to your account, including reported fraud and theft, which actually makes them less consumer-friendly than even those evil megabanks. In the past, they figured the problem would be best solved with a series of clunky security measures.

I’m not sure why, but they have now streamlined the login process to be more similar to banking industry standards. On November 6th, they sent out the following e-mail to account holders:

TreasuryDirect has completed its security upgrades. Now, it is not necessary to use an access card to log into your account. When you log into your account, you will receive an e-mail containing a one-time passcode and the opportunity to register your computer. Also, for your added security, you will select a personalized image and verify your contact information.

The website was subsequently slammed and completely unusable all day. Always fun to spend the day wondering if your money is still there. 🙂 Today, I was able to log into my account and check out the new process. As mentioned in the e-mail, here are the new layers of security:

- You must enter your account number, no usernames. So it’s still W-123-456-789, instead of something you would use across multiple websites like “johndoe90210”.

- If your computer is not recognized, a one-time passcode is sent to the e-mail address on file, valid for only 2 hours. You must enter this passcode to go further, and you can set a cookie to remember your computer and skip this step in the future. For some reason, the cookie didn’t work for me, I always have to go the passcode route. (screenshot)

- You must set a personalized image and caption text. This is standard procedure amongst banks now to prove that you are on the valid TreasuryDirect site and not a fake spoofing website.

- Finally, you must enter your account password by clicking keys on a virtual keyboard. This is to counteract keyloggers. As before, You can use a physical keyboard simply by disabling javascript.

I see this as an improvement in accessibility, although probably a slight decrease in security. I’m okay with it; I can finally shred my secret decoder ring access card!

Last updated: November 7, 2011

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Savings I Bonds September 2011 Update: 3.06% For Next 6 Months

Posted on October 20, 2011 // 15 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.New inflation numbers are out for September 2011, so it’s time for the usual semi-annual update.

New Inflation Rate. March 2011 CPI-U was 223.467. September 2011 CPI-U was 226.889, for a semi-annual increase of 1.53%. (CPI-U increased 3.9% over last 12 months.) Using the official formula, the variable interest rate for the next 6 months will be approximately 3.06%, depending on the upcoming fixed rate announcement.

Purchase and Redemption Timing Tips. You can’t redeem savings bonds until after 12 months, and any redemptions within 5 years incur a interest penalty of the last 3 months of interest. A known “trick” with I-Bonds is that if you buy at the end of the month, you’ll still get all the interest for the entire month. It’s best to give yourself a little buffer time though, since if you wait too long your effective purchase date may be bumped into the next month.

Buying in October. If you buy before the end of October, the fixed rate portion of I-Bonds will be 0.0%. You will be guaranteed an variable interest rate of 4.60% for the next 6 months, for a total rate of 0 + 4.60% = 4.60%. For the 6 months after that, the total rate will be 0.0 + 3.06 = 3.06%. Let’s say we hold for the minimum of one year and pay the 3-month interest penalty. If you buy at the end of October 2011 and sell at the beginning of October 2012, you’ll earn a 3.34% annualized return for an 11-month holding period, although you may want to hold it longer as new interest rates are announced. This is much better than any 1-year FDIC-insured bank CD available right now, keeping in mind the liquidity and purchase limits.

Buying in November. If you wait until November 1st, you will get a new unknown fixed rate + ~3.06% for the first 6 months, and an unknown rate based on ongoing inflation after that. Based on the current market rates of Treasury Inflation-Protected Securities (TIPS), in my opinion it is very likely that the new fixed rate will remain zero. A lot of uncertainty with this route.

Existing I-Bonds? If you have an existing I-Bond, the rates reset every 6 months (depending on your purchase month). Your monthly rate = your specific fixed rate + variable rate. Even at a low fixed rate, your existing savings bonds are paying much more than current savings accounts, so be very sure if you wish to redeem them.

Beware Low Purchase Limits. The annual purchase limit is $5,000 in paper I-bonds and $5,000 in online I-bonds per Social Security Number for 2011. For a couple, that’s a $20,000 total cap per year. If you have children, you may be able to buy additional savings bonds by using a minor’s Social Security Number

Buy online at TreasuryDirect.gov. As for paper, here is a post on how to buy paper savings bonds from your local bank. Paper bonds will be ended in 2012, except through a small window by overpaying your taxes on purpose.

With the interest rate calculations above, we find that savings bonds still pay much more interest than equivalent bank CDs with the same low risk. Also, interest on savings bonds is not subject to state income taxes as well as other unique tax advantages. I’m buying up to our limits and keeping all of my existing bonds for the foreseeable future. For more background, please see the rest of my posts on savings bonds.

Last updated: August 9, 2018

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

U.S. Savings Bonds Have Outperformed Stocks Since 1998?

Posted on August 31, 2011 // 24 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.A reader recently told me that he was no longer investing in the stock market after seeing the chart below from the Savings Bond Advisor. It shows the total portfolio value after investing equal monthly amounts in either the S&P 500 stock market index or Series I US Savings Bonds. The time period is from September 1998 (when “I Bonds” started being sold) through August 1, 2011. My comments follow.

The past returns of savings bonds are indeed pretty good, but not likely to be repeated. Series I Savings Bonds (I Bonds) were the new thing in 1998, and the government offered some really enticing interest rates on them. I Bonds have a fixed component that lasts for the duration of that specific bond and an variable component that adjusts with inflation every 6 months. From 1998 to May 2001, the fixed component was always between 3% to 3.60% above inflation (source). However, since May 2008, the fixed rate has been between 0% and 0.7%. For the past year, the fixed rate has been a big fat zero. I would love to have a savings bond paying 3% plus inflation (currently 2.30%), as some current bondholders have, but I don’t expect that to ever happen again.

Now, that doesn’t mean that they aren’t still a competitive investment, especially for the short term. Since interest rates are so low, I still buy savings bonds even at a 0% fixed rate as part of my emergency fund cash reserves.

Savings Bonds are being slowly killed by the government. Even though savings bonds have historically encouraged people of all income levels to save, it appears that the US Treasury is slowly killing the savings bond. As recently as 2008, you could buy $30,000 worth of each type of savings bonds a year, per person. For a while, we were able to even use credit cards to buy them without a fee. Today, you can only buy $5,000 of paper I-bonds and $5,000 of electronic I-bonds a year, and even paper savings bonds are being phased out in 2012. (You can still overpay your taxes and buy paper bonds with a tax refund in 2012.) There was even a NY Times article last week entitled Save the Savings Bond. Basically, even if you wanted to create your retirement portfolio with savings bonds, you can’t.

Investing solely in inflation-linked bonds is actually recommended by some financial authors. The thing is, the government has so much debt that it greatly prefers US Treasury bonds which can be sold by the billions. Printing a $50 savings bonds is not even a drop in the bucket, it’s closer to a H2O molecule in the bucket. What you can invest in is Treasury Inflation Protected Securities (TIPS), which like I Bonds are backed by the government and pay an interest rate linked to inflation. Economics professor Kolitkoff in the book Spend ‘Til The End recommends your entire portfolio to be TIPS. The problem? You’re gonna have to save a lot. TIPS yields are very low, currently offering yields of negative 0.7% above inflation (!) for a 5-year bond to a meager 1.1% above inflation for a 30-year bond. If you’re okay with saving 50% of your income every year for 30 years, then this plan might work for you.

There is no easy answer as to the best place to invest right now. I am sticking with a diversified low-cost portfolio with both stocks and bonds (including a nice chunk of TIPS inside, which has done quite well recently), and you can see with this chart that it has also done pretty well the last decade.

Last updated: April 25, 2019

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

US Treasury Ends Paper Savings Bonds in 2012

Posted on July 14, 2011 // 20 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone.According to a press release, the Treasury will no longer sell paper U.S. savings bonds through banks and other financial institutions as of January 1, 2012. You can still buy electronic savings bonds through TreasuryDirect.gov.

I didn’t see any news regarding the purchase limits changing. The annual purchase limit is currently $5,000 in paper bonds and $5,000 in online bonds per Social Security Number. However, with the disappearance of paper bonds this would seem to cut the overall limit in half starting in 2012. There does seem to be a small loophole in the press release:

Series I paper savings bonds remain available for purchase using part or all of one’s tax refund. For more information on this feature, visit www.irs.gov.

Does this mean I should intentionally overpay my taxes by $5,000 this year, so I can buy an extra $5k in savings bonds in 2012? If there is continued inflation and low interest rates, Series I bonds could continue to be a good deal. They currently offer 4.60% interest for 6 months, plus an yet-to-be determined amount for the next 6 months. Even if that later rate is zero, you could still earn over 2.5% annualized over the next 11 months. For more details, see the rest of my posts on savings bonds.

Last updated: July 14, 2011

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

Reminder: Savings Bonds Monthly Purchase Deadline Tips

Posted on May 20, 2011 // 7 Comments

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone. Here’s a reminder regarding an opportunity to buy savings bonds near the end of May and receive an annualized return of 2.51% over the next 11 months. This would be 1% more than the highest current CD rates, with potential for continued higher interest. See this previous post for more details. The main catch to this opportunity is that you will not be able to sell your savings bonds at all for the next 11 months.

Here’s a reminder regarding an opportunity to buy savings bonds near the end of May and receive an annualized return of 2.51% over the next 11 months. This would be 1% more than the highest current CD rates, with potential for continued higher interest. See this previous post for more details. The main catch to this opportunity is that you will not be able to sell your savings bonds at all for the next 11 months.

The reason why you want to buy at the end of the month is that savings bonds are labeled by month, and as long you buy anytime in May, it will be stamped with a May 2011 date. Then, on the first day of May 2012, you can redeem for an entire year’s worth of interest. However, you don’t want to miss the deadline, because then your bond will end up an April 2011 bond. The annual purchase limit is currently $5,000 in paper I-bonds and $5,000 in online I-bonds per Social Security Number. For a couple, that’s $20,000 per year.

For electronic bond purchases, Ken of DepositAccounts conducted an experiment as to how late you can wait to buy them on TreasuryDirect. To summarize, in order to avoid this, you should enter your purchase order a minimum of two business days before the last day of the month. For peace of mind, I would pad it 4 business days. You can schedule your purchase ahead of time online (recommended).

For paper bond purchases, you can visit your local bank and ask to buy them. Here are detailed instructions. Not all banks do this, so check ahead of time. The issue date of the savings bond will be the same day that the bank accepts payment. This date will be noted clearly on the application, and the bank should also stamp it to confirm. In this case, if you are familiar with the bank and you have the money available, you could conceivable wait until the last day the bank is open before the end of the month. Again, I’d try a couple days beforehand to be safe.

Last updated: May 20, 2011

My Money Blog has partnered with CardRatings and may receive a commission from card issuers. Some or all of the card offers that appear on this site are from advertisers and may impact how and where card products appear on the site. MyMoneyBlog.com does not include all card companies or all available card offers. All opinions expressed are the author’s alone, and has not been provided nor approved by any of the companies mentioned. MyMoneyBlog.com is also a member of the Amazon Associate Program, and if you click through to Amazon and make a purchase, I may earn a small commission. Thank you for your support.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work){kind=link}