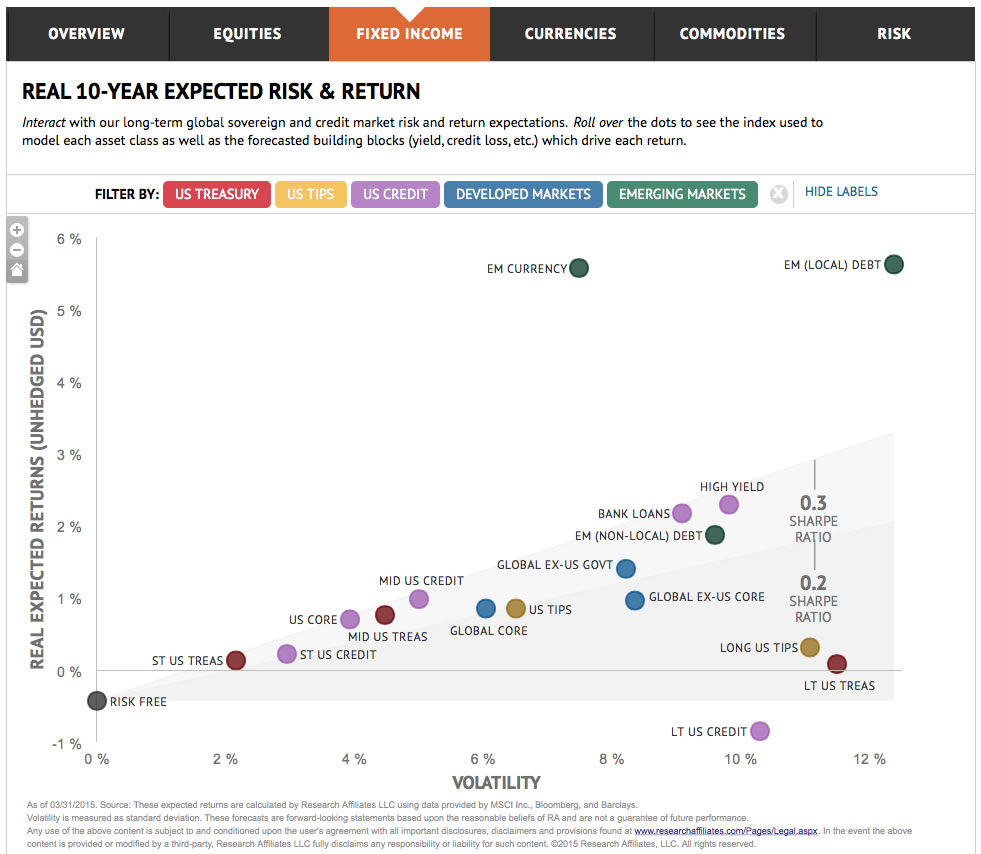

When investing in stocks and bonds, it is important to take a long-term perspective. We’ve all heard that phrase. A new tool called PortfolioCharts.com lets you create charts that make it easier to visualize the relationship between returns and holding periods. Created by a fellow named Tyler, found via The Reformed Broker.

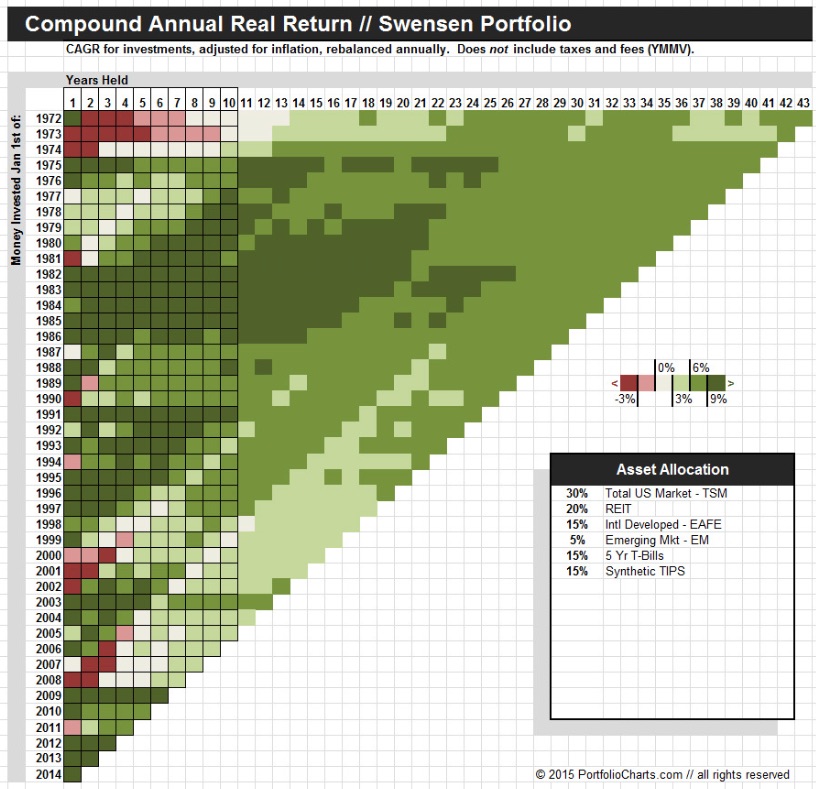

With the Pixel chart, you can customize any asset allocation and see that portfolio mix’s returns over a multitude of timeframes. Here’s the chart for The Swensen Portfolio, which is the closest “lazy portfolio” to my personal portfolio – 30% US Total, 15% Foreign Developed, 5% Emerging Market, 20 US REIT, 15% 5-Year Treasuries, 15% TIPS.

You can see that depending on your starting year, the returns over the next 1-9 year period could be pretty rough. But as long as you held for 10 years or more, you always got a positive real return above inflation. You can also see that the often-promised 5% real returns aren’t always guaranteed, although historically if you held on for 20+ years your odds were pretty good.

You may recall a similar style of chart from the NYT and Crestmont Research which includes additional data going back to 1920:

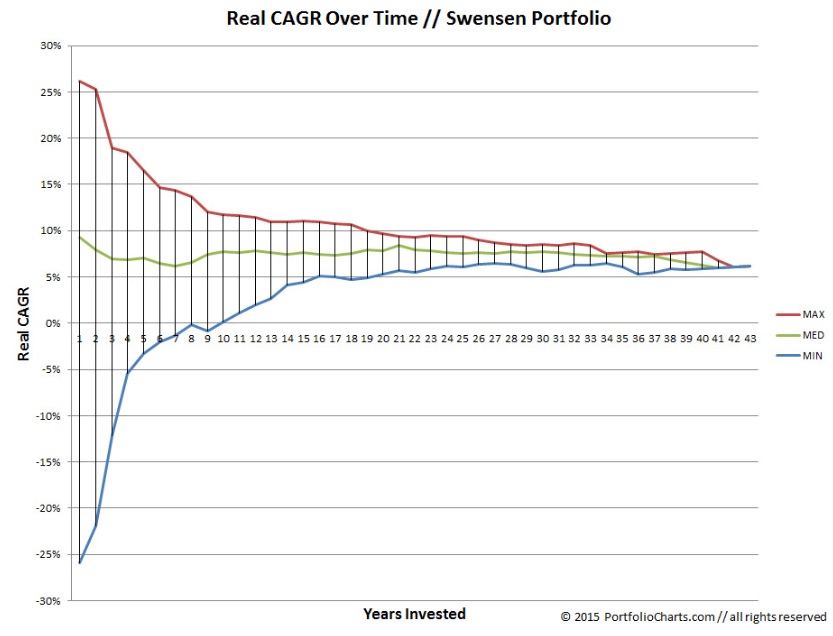

My favorite style is the Funnel chart:

The Funnel chart shows the changing uncertainty of compound annual growth rates over time. This demonstrates how long you may need to hold a portfolio to experience the average long-term returns it advertises. It also provides a nice snapshot of the range of 1-year volatility.

Here’s the Funnel for the same Swensen Portfolio:

The funnel chart also supports the notion – in an even simpler way – that if you can take a long-term perspective, your risk of losing money should decrease. Here’s a similar chart from the classic investing book A Random Walk Down Wall Street that was one of my early blog posts:

Finally, the Hurricane chart allows you to simulate what would have happened to your portfolio balance if you made annual withdrawals, such as in a retirement scenario.

Warren Buffett is another famous supporter of taking the long-term view. From a recent CNBC interview:

Buffett, who looks to buy stocks or business for their long-term prospects, said recent weakness in the market does not concern him.

“Stocks are going to be higher, and perhaps a lot higher 10 years from now, 20 years from now,” he said, adding that’s why he does not try to time the market.

Hopefully for those investors with a long runway ahead of them, this new tool will help you view your portfolio in a more patient manner. I’ll try to remember it when the next market panic arrives.

I ran across

I ran across  The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)