HBO has a new documentary film called Becoming Warren Buffett that includes a more personal look at his life, including “never-before-released home videos, family photographs, archival footage and interviews with family and friends.” I just watched it on using the HBO Now 30-day free trial. Here’s the HBO trailer:

My notes:

Warren Buffett does have a folksy exterior. He drives around in his own car, eats at McDonald’s, drinks Coke, and still lives in the same house he bought in 1957 for $31,500. He doesn’t have a personal stylist or fashionable clothes. He likes to say things that sound like common sense.

Some people think this is a fake exterior. I don’t think so. Some people take this to mean that “anyone” can get rich buying and selling stocks. I also don’t think so.

Warren Buffett is also extraordinarily intelligent and competitive. His net worth is one of his scorecards. His skill is capital allocation and that involves extreme emotional detachment and rationality. These are features that aren’t visible, and he’s better at it than you are.

Warren Buffett is always learning and improving. Buffett skipped grades, finished high school at age 16, and finished his undergraduate degree in 3 years. However, instead of any degree hanging on his office walls, he has a certificate from a Dale Carnegie course on public speaking. Buffett realized his weaknesses and worked to improve himself.

Charlie Munger shared an analogy with someone who can juggle 15 balls in the air. How did that happen? Well, at some point they started with one ball, practiced, and then two balls, and then practiced some more…

The film does explore his personal life, albeit in a very sensitive and respectful manner. His emotionally volatile mother is mentioned but not explored deeply. His father was a great influence and Warren keeps a picture of his dad on the wall in his office. His late first wife, Susan, was shown as a very kind, considerate person. In her interviews, she came off as very well-spoken, fair, and intelligent. She definitely played a huge part in his overall development. She is also a huge reason that eventually $100 billion is going to charitable causes to improve the world.

Buffett has said many times that he won the “ovarian lottery”. He was born in the United States. He was born a male. He had many opportunities to succeed and support structures if he failed.

As a relatively new and clueless parent, I wonder about his kids. Warren Buffett spent most of his time working and not much time raising the kids. I wonder what they would have been like if their father didn’t become famous and rich. (Supposedly when they were young, Warren really wasn’t all that rich or famous yet.) Today, all three of them appear to be well-adjusted adults, but everyone’s job is to give away their parent’s money. Do they do this out of obligation to their parents? Out of obligation to make sure the money is well spent? Is this the “job they would get if they didn’t need a job”?

Warren attributes his financial success to “Focus”. Was that laser focus detrimental to his family and other personal relationships? What if he had just stopped when he reached $10 million or whatever?

Warren Buffett is worth over $60 billion, yet he doesn’t meet certain definitions of “retirement”. What Buffett has always been keen on is constructing a life that fits him. His version of financial freedom includes sitting by himself and reading 5-6 hours a day and thinking. He’s loved being his own boss since filing his first income tax return at age 13 and taking a $35 tax deduction for the use of his bicycle and watch on his paper route.

I think hero-worshipping can be dangerous when you simply try to follow everything about someone else. Every human has their flaws. We should extract the qualities that we admire, and try to emulate those qualities. Warren Buffett has a lot of worthy attributes and I value his shareholder letters, but I certainly don’t want to “be just like Warren Buffett”. For me, I respect that he basically figured out how he wanted to live his life (no bosses, lots of reading) and that he achieved it an early age. The eventual billionaire status doesn’t really excite me, other than the fact that he managed to remain “grounded” and relatable.

Overall, the film does offer some new personal glimpses but not much new deep material for those that have read his biographies – The Snowball: Warren Buffett and the Business of Life by Alice Schroder and Buffett: The Making of an American Capitalist by Roger Lowenstein.

Berkshire Hathaway has released their

Berkshire Hathaway has released their  The sales pitch for American Express has always been that their cardholders are wealthy and thus big spenders, which in turn justifies their above-average transaction fees charged to merchants. The theory is a merchant won’t mind paying more in fees if it is offset by higher average receipts (and thus profits). This is why Tiffany & Co takes AmEx and my favorite Indian food truck does not.

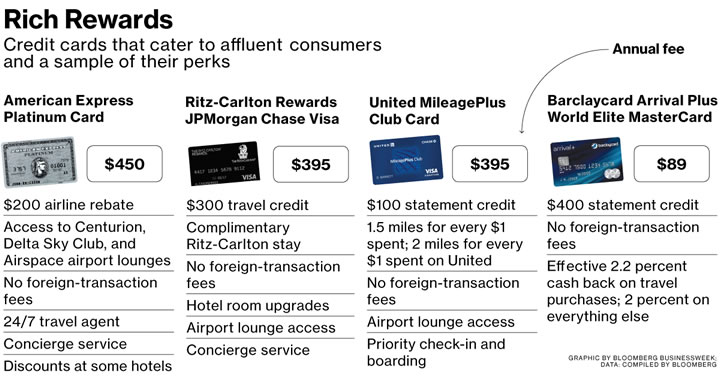

The sales pitch for American Express has always been that their cardholders are wealthy and thus big spenders, which in turn justifies their above-average transaction fees charged to merchants. The theory is a merchant won’t mind paying more in fees if it is offset by higher average receipts (and thus profits). This is why Tiffany & Co takes AmEx and my favorite Indian food truck does not.

In the provocatively-titled article

In the provocatively-titled article  The Best Credit Card Bonus Offers – November 2024

The Best Credit Card Bonus Offers – November 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - November 2024

Best Interest Rates on Cash - November 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)