Woohoo, I just received my first interest payment on my real estate crowdfunding experiment #1. I put in $5,000 at 11% APR, which should work out about $46 a month but the first partial payment was an underwhelming $16.81. I e-mailed Patch of Land and they said I could share the details of my loan, so here they are. If you are a SEC accredited investor and a (free) registered member, you can view it on their site.

Financial details. Here is the summary and breakdown from the Patch of Land listing:

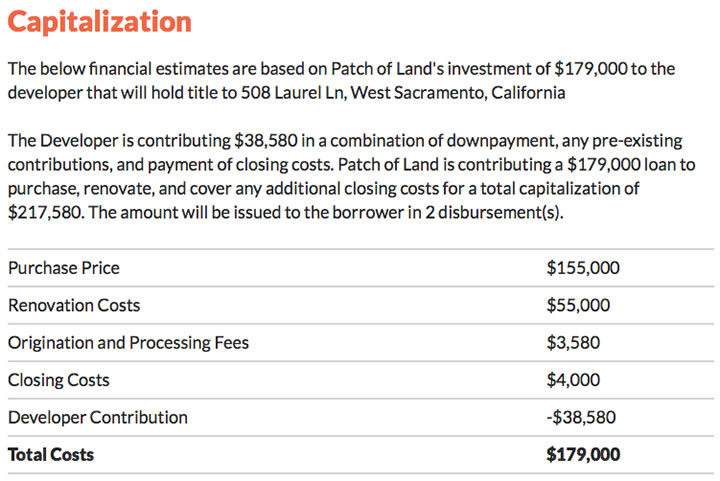

The developer is requesting a loan of $179,000 in order to purchase and renovate the underlying property. The property was purchased for a total of $155,000 in April of 2015. There is minor renovation needed for the underlying property, totaling $55,000. The borrower will receive 2 draw(s) totaling $175,420 over the course of the loan. The initial draw in the amount of $120,420 occurs when the loan closes. The second draw of $55,000 will be disbursed when renovation is completed. The borrower plans to sell in 1 year or under.

Loan is secured by the property, in the first position. Also have personal guarantee from borrower (not worth much). 6-month term (roughly April 15th to October 15th). 11% APR interest, paid monthly.

So the developer is contributing roughly $40,000 and the loan is roughly $180,000. So a total of $220,000 is being put into this house. Considering that the loan will charge roughly $10,000 in interest over 6 months, plus a potential 6% brokers commission upon sale, this house would have to sell for around $245,000 for the developer to break even. The developer thinks the house can sell for $275,000 but it all depends on how well they spend that $55,000 in renovation costs and how the local market holds in the next 6 months. A 3rd-party appraisal gave a estimated after-repair value of roughly $240,000, which is probably a conservative number but suggests a potentially tight profit opportunity for the developer.

In the end, I do believe it likely that the loan amount of $179,000 can be recovered from this property in a liquidation scenario (see below). It is important to note that the developer doesn’t actually get the final $55k until the renovations are completed and thus the home will be worth more.

Property details. Single-family home in West Sacramento, California. The address is 508 Laurel Lane. You can look up details from public records using sites like Zillow or Trulia. Built in 1954, 3 bedrooms, 1 bath, 1,675 sf living area, 7,000 sf lot. The pictures provided suggest a house that is definitely in need of a kitchen remodel and light repairs, but it wasn’t destroyed inside. The house is about the same size and appearance of other houses in the neighborhood.

I am not familiar with the Sacramento area. The zip code of 95691 appears to have slightly above-average selling prices compared to West Sacramento overall. According to Google Maps, the neighborhood is relatively close to freeway access and downtown Sacramento. I also looked at Google Street View and I liked that the neighboring houses all appeared to have well-maintained houses and manicured lawns. That suggests pride of ownership and/or a certain level of peer pressure to keep your house looking nice. Based on a quick Craiglist search of comparable rentals, this house should support roughly $1,400 to $1,500 in monthly rent, which is not bad compared to the ~$245,000 that I’d like this house to sell for once fixed up.

In the end, there are a number of risks in this deal, but otherwise it wouldn’t pay an 11% annualized interest rate. From my vague understanding of hard money loans, I was hoping for much lower LTVs in the 50% range instead of the 80% range. Perhaps the lessening of loan standards from new money flooding this new asset class is already happening. It would be educational to see how they handle a liquidation… but I should just sit back and quietly cash my interest checks.

I’m not sure exactly what details of this investment I am allowed to share, so I’ll save that part for later. It will be good for you guys to pick apart, but it doesn’t really matter for other investors as the project is already 100% funded. I’m just waiting on my first interest payment in May, and hope to be done by October. At the end of the year I will get a 1099-INT.

I’m not sure exactly what details of this investment I am allowed to share, so I’ll save that part for later. It will be good for you guys to pick apart, but it doesn’t really matter for other investors as the project is already 100% funded. I’m just waiting on my first interest payment in May, and hope to be done by October. At the end of the year I will get a 1099-INT. The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)