The standard advice for saving money on auto insurance is to shop and compare prices. You could use a comparison website, but they may not include every insurance carrier listed in your state. A lesser-known fact is that auto insurance is regulated on the state level, where each company must submit their rates for approval. Many states in turn share this information with consumers. Some states also provide complaint data, so you can also view which insurers have the most complaints relative to their market share. Here is an example report for the state of California:

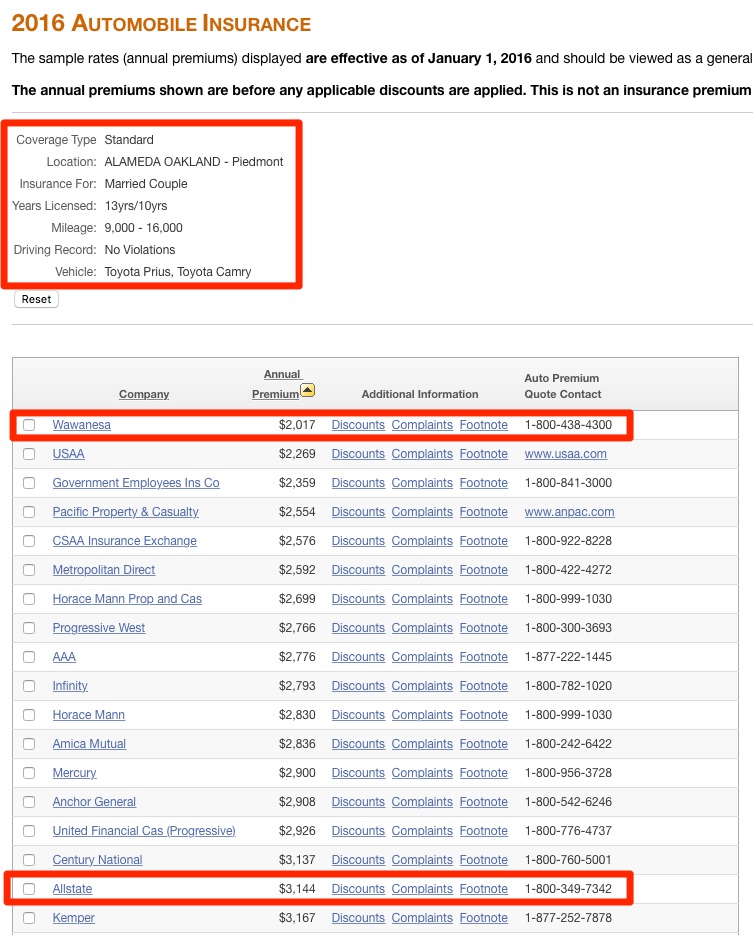

For the hypothetical scenario above, the difference between the cheapest option (Wawanesa) and the 17th cheapest option (AllState) is over $1,100 a year.

Using this information, a consumer can more efficiently choose to get quotes from the insurance companies which will likely offer them the lowest rates. Individual companies often choose to focus on certain areas of the market – drivers with clean records, drivers with tickets/accidents, teen drivers, and so on. Credit scores are another newer area of focus. Try to find the comparison example that fits your situation the closest.

These premium comparison reports can often be hard to locate, so I manually searched for all 50 states and the District of Columbia and shared my results below. (I used the same template as my free state income tax e-filing post.) Some states share very specific data down to zip code, some share only a few broad example rates, and others share essentially nothing. In alphabetical order (just click on the state):

| State | Notes |

| Alabama | Click on “Compare Premiums” for the scenario that best fits your own. |

| Alaska | Personal Auto Insurance Premiums Comparison Guide > Premiums Comparison Guide.pdf |

| Arizona | 2015 WEB_AutoPremiumComparison_Publication.pdf |

| Arkansas | Insurance Cost Comparison > Private Passenger Auto |

| California | 2016 Automobile Insurance |

| Colorado | Private Passenger Automobile Premium Comparison Report. |

| Connecticut | None found. |

| Delaware | Automobile Insurance Rate Comparison |

| Florida | Auto Rate Comparison Tool |

| Georgia | Automobile Insurance Rate Comparisons |

| Hawaii | Motor Vehicle Insurance Premium Comparison |

| Idaho | None found. |

| Illinois | No premium info, but some guidance provided including complaint ratios. |

| Indiana | None found. |

| Iowa | Auto Insurance Pricing Guides |

| Kansas | Auto Insurance Shopper’s Guide. |

| Kentucky | Auto and Home Insurance Guide with Disaster Guide and Premium Comparison. [PDF available] |

| Louisiana | Automobile Rate Comparison Guide. |

| Maine | Auto Insurance, Comparison of top 10 policies. |

| Maryland | Auto Insurance – A Comparison Guide to Rates. |

| Massachusetts | Auto Insurance Premium Comparisons. |

| Michigan | Comprehensive Guide to Auto Insurance. |

| Minnesota | None found. |

| Mississippi | Personal Auto Rate Comparison. |

| Missouri | Auto Policies – See policies of insurance companies ranked by market share. |

| Montana | Auto Insurance Price Comparison (pdf). |

| Nebraska | Auto Rate Guide (direct link to PDF). |

| Nevada | Consumer’s Guide to Auto Insurance Rates. |

| New Hampshire | New Hampshire Auto Cost Premium Rate Comparison. |

| New Jersey | Auto Insurance Premium Comparison. |

| New Mexico | None found. |

| New York | No premium comparison, but there are complaint rankings and discount list (pdf). |

| North Carolina | No premium comparison, but there is a Consumer Guide to Automobile Insurance and complaint ratio list for insurers. |

| North Dakota | Cost Comparison Survey |

| Ohio | Shopper’s Guide to Auto Insurance, with example premiums and complaint data. |

| Oklahoma | Rate Comparison Chart. |

| Oregon | No premium comparison found, but the Oregon Consumer Guide to Auto Insurance has helpful info |

| Pennsylvania | A rate comparison guide for Automobile Insurance in Pennsylvania. |

| Rhode Island | Could not find rate comparison, but see Consumers Guide to Auto Insurance for helpful info. |

| South Carolina | Quick Links – Automobile Price Comparison Guide. |

| South Dakota | None found. |

| Tennessee | Limited market share and other info at Personal Auto Policies Rate Changes. |

| Texas | Automobile Insurance Price Comparison |

| Utah | Auto & Homeowner Annual Comparison Tables with Complaint & Loss Ratio Info. |

| Vermont | No premium information found, limited info in Consumer’s Guide To Auto Insurance. |

| Virginia | Auto Insurance Sample Premium Table. |

| Washington | None found. |

| Washington DC | None found. |

| West Virginia | 2011 Annual Survey (see bottom right). |

| Wisconsin | No premium information found, limited info in Consumer’s Guide To Auto Insurance. |

| Wyoming | No premium information found, limited info in Wyoming Personal Automobile Insurance Guide (last updated in 2000, ack!) |

I have tried my best to locate the information for each state, but it is quite possible I’ve overlooked something or the websites have since changed. Please let me know if you find any errors or broken links.

The Best Credit Card Bonus Offers – November 2024

The Best Credit Card Bonus Offers – November 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - November 2024

Best Interest Rates on Cash - November 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

As a tangent, I live in Minnesota. For this last year my premiums jumped $100 per 6 months. No accidents, violations or claims submitted. When I called up and asked why the jump (~$500 to ~$600/ per 6 months) I was told Minnesota wasn’t paying enough in premiums for all the claims out there? That was a new twist on the insurance rate game. If you don’t like the risk pool or what it pays, just widen it. I live in rural, outstate. I’m not the risk that someone living in metro area is, and the insurance company has stats to prove that.

Time to shop around? 🙂

Yeah, I did that too in response. Do that regularly, so it showed industry wide when I looked again. Unfortunately.

I had a similar experience recently. I moved from VA to AZ & my insurance premium jumped $200/6 months for same coverage. No issues/changes in my profile.

Wow – what a useful thing to do.

Too bad my state sucks. (WA)

Amazing work, thank you so much! Would you mind if I linked to your post on my blog whitecoatmoney.com?

Link away!

Also note that if you have been with the same company more than a few years, you are probably overpaying. New customers get the best rates.

Besides house and auto I also opt for Umbrella coverage. Are there any risks in coverage if you do not have all 3 with the same insurance company? My reasoning was that they would at least pay up without passing the buck if they cover all 3 policies. Thoughts?

Thank you

I was excited to read your post, then thoroughly annoyed that my state of CT has no such info. I sent them an email asking them why, and I’ll share their response when I get it.