When I was a senior in high school, I still remember my parents offering me a new luxury car instead of tuition assistance. Although I’m pretty sure it was only a test, it did serve to remind me of the cost of tuition and not to waste it. Seeing the average student debt of graduates is now over $30k, I wanted to see how the price of a new car and student debt tracked. These are the best charts that I could fine.

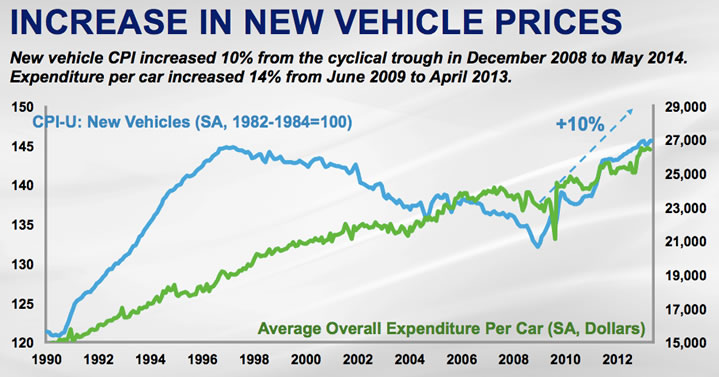

The green line in the first chart tracks the average cost of a new vehicle as rising from ~$15,000 to ~$27,000, within the time period of 1990 to present. I don’t believe the green line is inflation-adjusted. You can see it runs from roughly $15,000 to roughly $27,000. (Source: Atlantic)

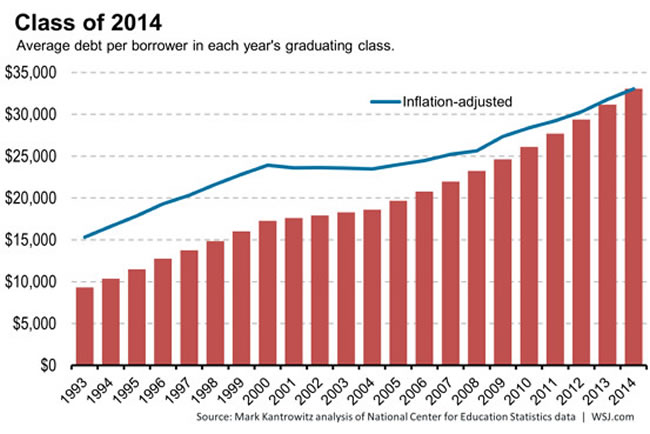

The second chart below tracks the average student debt upon graduation over basically the same timeframe, 1990 to present. The non-inflation-adjusted value has risen gone from ~$9,000 to ~$33,000. (Source: WSJ)

It is hard to equate the two values because student debt is just the amount left over after the parent (usually) pays as much as they can while the student is in school. However, this USA Today article suggests that since 2010 parents on average have been paying less.

Five years ago, only half of families reported using grants and scholarships to pay for college. This year, two-thirds of families did, the study shows. […] Meanwhile, parents are contributing less of their income and savings toward college costs, covering 27% of college costs compared with 37% in 2010, the study shows.

At the same time, other reports show that for parents with top 20% incomes, education spending has nearly doubled as a share of their total budget.

Average student debt is definitely growing faster than new car price. But in terms of total size, it is still comparable to the cost of a new car. People finance new cars all the time. Does that make student loans less scary? I don’t know, because financing a new car has always scared me a lot too.

Even after taking the tuition assistance from my parents, I still came out of college with roughly $30,000 in student debt myself, above-average at the time. I like to think that I got better value of my degree than a new car. 🙂

The Best Credit Card Bonus Offers – November 2024

The Best Credit Card Bonus Offers – November 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - November 2024

Best Interest Rates on Cash - November 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Cool data!

Another factor that likely contributes to the march up of student debt in the middle of a recession is the lack of employment opportunities for young people. Without good job prospects, students who might be lured into the workforce tend to stay in school and rack up more tuition, fees, etc. It is essentially a demand spike leading to higher costs for college education, particularly at competitive colleges that will not expand their enrollment supply.

To your point that both student loans and cars require roughly the same financing: you can’t repo a student’s knowledge or degree. Collateralized debt always seems less risky to me.

I attended three different major universities and graduated with a Ph.D. from the last one. When I graduated, I had around $9,000 in the bank and no student debt. My parents helped with my undergrad degree while I lived at home after returning from the service and before there was a GI Bill in the 60s. Between each degree, I worked and saved money for school. In my grad programs, I worked for the university. The worked experience I obtained between degrees gave me a better chance of getting a job after I received my Ph.D. There are ways to fund your degrees without going into debt, but it is not as easy as going out and getting a loan. My son is funding his degree right now with the GI Bill after serving four years in the Marines, and he will graduate debt free, too.

Jonathan, I really like your parents’ “test”.

Well, I went to an out-of-state public university and they knew I really wanted to go so maybe it wasn’t so risky. 😉 I guess they just wanted to make sure I REALLY wanted to go since it was so expensive.

Things like the GI Bill and ROTC scholarships are still very viable ways to pay for school. Many states, especially in the South (Georgia, Florida, SC, among others) still have large state-level scholarship programs, funded by the lottery, which pay for a bulk of an undergrad degree’s cost.

The large outliers for student debt you generally read about in the news are either 1) students who failed to graduate & have the burden of school debt without the benefit of a degree and 2) students who took on added debt in pursuit of a Masters/Doctorate.

Steve, I understand your PhD experience colors your outlook on higher-level degree cost, but I would frankly be shocked if ANY higher-level degree recipient can obtain one without any student loan debt AND $9,000 (which is presumably an inflation-adjusted ~$30k from when you were in school) in the bank.

I recently obtained my JD and am now a gainfully-employed attorney, but my student debt level (solely from law school; I had no undergrad debt) is over six figures, even with funds I contributed from professionally working between undergrad & law school. Without utilizing PAY-E/income based debt repayment options, paying off that debt would be near-impossible.

Grad degrees in engineering are often covered via assistances and paid a stipend. So yes you can go get a doctorate without any debt… at least in engineering.

Also many doctorate programs in the humanities, depending on the university of course, include support of tuition and a stipend with admission. IMHO the economics of those programs only make sense if they are fully supported, i.e. it doesn’t make economic sense to pay PhD tuition to become a liberal arts professor (in part because of the pay but also because the ratio of candidates to positions is very high).

The thing I really hate about stories like this, is the use of “average” student debt, instead of median student debt, which would be more accurate and, frankly, more responsible.

Four guys are drinking at a bar and among them they have an average of $3,000 in assets. Bill Gates walks in, grabs a seat. Among the five, personal assets now average in the billions. Average is meaningless. Median is what matters.

That about 35% of students graduate college/university with a four-year degree without debt is rarely mentioned. But including that 35% as part of the pie, the *median* average debt for a four-year graduate is just over $10,000, less if from a public institution. Note myth number three in this article:

http://www.washingtonpost.com/blogs/innovations/wp/2013/09/24/five-myths-about-college-debt/

IMO, that is still too much of a burden placed on students and – if they are lucky – their families. But the focus of “average” student debt is inaccurate.

The MEDIAN student debt for graduates of my alma mater is $0 and its a large public university.

Thats because less than half of students who graduate ever take out any loans. Thats the result of a mixture of good financial aid for low income students and high income families being able to afford the entire bill out of picket and a few athletic scholarships.

Thats an interesting test your parents did. I assume they were pretty certain of the answer before they asked you. 🙂

I think its interesting how we as a nation seem to be panicking about student loans yet people buy new cars all the time and twice as many households carry car loans.

Good comments; You have to be very careful with student loan statistics as to what you are referring to. Are you looking at all students? Or just students with some sort of outstanding loan? Did they graduate? From undergrad or advanced degree? Average, or median?

Based on the wording of the WSJ article, the $33k number and chart above is the average for graduating (undergrad) student with some sort of outstanding loan. If you included all students, the number would be much lower. 30% of students graduate without any loans at all.