Added bonus for new sign-ups. I’ve been a registered member of RealtyMogul for a while, and they recently emailed me that if I referred a friend, we’d both get a $150 Amazon gift card just for completing the registration process (i.e. zero investment required). Here is a screenshot. The restriction is that you must be an accredited investor, which means either a single income of $200,000, joint income of $300,000, or net worth of $1 million excluding primary residence. I’ve registered at a few of these sites, and you may need to send in a scanned W-2 (was allowed to remove SSN) or brokerage statements for verification.

This is a nice carrot if you are already interested in hard money lending or fractional real estate ownership. You must either use this special sign-up link or use the promo code JONATHANP7 during registration. Offer expires 12/31/15.

*The referrer and the referred will each receive a $150 gift card (redeemable at Amazon.com) upon successful completion of the investor registration process at RealtyMogul.com by the referred party. Gift cards will be mailed within 30 business days to the address on file. This promotion is limited to 6 referrals per referral code and is only valid until December 31, 2015.

Original post from mid-2013 below:

Realty Mogul is a new “crowdfunding” start-up that lets you invest in residential investment property for as little as $5,000. You either take a partial ownership position in a property, or you become a lender to (experienced) house flippers. The new thing here is that you can do it completely online with a few mouse clicks (no mortgage brokers, real estate agents, or tenants) and again that low minimum $5,000 investment. (Thanks to reader Johnson for the tip.)

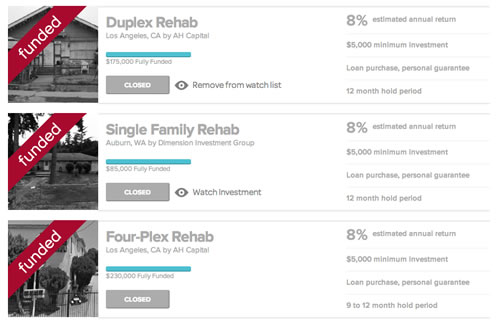

Taking an equity ownership position means that you own a little slice of a single-family home or multi-unit complex while a professional does the buying, fixing up, renting out, and eventual selling. Realty Mogul only has done one deal like this so far (fully funded) and the intended timeframe is 5-7 years. You earn rent while the house hopefully appreciates in value, and cash out when the house sells.

Being a lender looks very similar to the age-old practice of hard money lending, just with smaller chunks. You lend the money to a house flipper who needs a short-term loan (3 months to a year) and doesn’t want to deal with traditional mortgage lenders and their closing costs and long underwriting delays. The loan is backed by a personal guarantee (not too special, you can try to sue and/or hurt their credit score) and more importantly you usually have a first position lien on the property (if they don’t pay, the lender gets the title to the house). Most of the previously funded loans have an annualized interest rate of 8%.

Realty Mogul states that they differentiate themselves from other similar startups like FundRise and Prodigy Network by (1) outsourcing the real estate expertise to vetted professionals and (2) keeping a focus on cashflow, either via rent or interest payments. Right now they’ve only had about 7 investments, but they seem to open a new one up after the last one fully funds.

Currently, the SEC limits this type of investment to accredited investors, which means either a single income of $200,000, joint income of $300,000, or net worth of $1 million excluding primary residence. When I tried the application, the only screening process was to check a few boxes and state that you qualify. Supposedly, the recently passed JOBS Act will allow them to drop this requirement later this year.

If given the option, should I drop $5,000 into this to try it out just like with person-to-person lending? $5,000 is still a lot of money to put into an investment where you are not able to do much due diligence. Getting good returns on a single investment project is all about the skill of that particular rehab team. Will the teams that sign up for capital via Realty Mogul always be the good ones, or those that are having a hard time getting funding from elsewhere? I thought that hard money lending rates were more in the 10%+ range; I don’t know if I’d be happy with 8% but maybe that’s the going rate now. Even if you have collateral, recouping your principal in case of a bad loan can get complicated and time-consuming. At least with P2P lending I can spread $5k over 200 different loans such that even though I am certain to get some defaults, it is unlikely I will get a negative return overall.

More: TechCrunch, LendAcademy, BizJournals, The Verge

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Interesting idea, but I would think that with $5,000 you can invest in several publicly traded Real Estate Investment Trusts (REITs), and have a lower risk investment that you can cash out at any moment.

Hard to ignore an 8% annualized return. Can’t find that in many places nowadays. But as you imply, Jonathan, lack of ability for due diligence makes it difficult to ascertain risk. Top that with the risk of the current housing bubble bursting and it doesn’t seem like a viable investment to me.

With all of the different investment vehicles available today I wouldn’t touch this. The only attractive aspect is the 8% return and I see that more as the cheese in the trap than anything people will actually realize. I would stay far away from this.

I wouldn’t accept an 8% yield for this kind of credit risk. For an accredited investor there are better vehicles to get a better yield from direct lending with much better transparency, less credit risk, and better collateral.

As someone with considerable real estate experience, I would say:

As a lender in past real estate deals, this is awfully risky for an 8% return.

As a borrower in past real estate deals, sign me up for the cheap money! Hard money rates vary depending on local, but you would probably be paying 5+ points and a 12% rate. An experienced individual private investor would probably do 0 pts and 10-12%. An inexperienced rate chaser might give you 8%.

If you were to invest here, you are basically buying into an unproved fund. As the investor, it looks like you won’t have the opportunity to vet either the borrower or the property. With only 7 completed deals, I wouldn’t yet trust the company’s ability to vet deals. It also seems like they are not focused on a specific geographic area, which to me means higher risk. There are a lot of variables in local real estate markets. If you try to focus on more than 1-3 at a time, something is going to be overlooked.

My wife owns shares in a local private placement fund and although we neither vet the properties or the borrowers, I have known one of the fund managers for years and have complete trust in her judgment. The fund takes 2% in management fees and pays a preferred return of 9% and a profit sharing distribution of 25% of the profits.

Can you send me info about the local private placement fund?

Thank you

Adrian

Did you ever get the private placement fund info, if so please send me what you’ve found! Happy Ventures!

Interesting idea. I’d take a ‘wait and see’ attitude on this one. It might be a good deal for investors and the real estate pros both. Kinda like Lending club for house flippers. But it seems like there might be high risk here and so I’d wait to see how well they perform before I’d put any money into it.

Hi all, I’m Jilliene, the CEO of Realty Mogul. Thanks to Jonathan for the post and everybody for the comments.

You are all correct that there is risk in our investments, just like any other investment, but we try and mitigate that by working with established real estate companies and keeping LTVs low on our loans. You are also right that some lenders lend at 5 points and 12% but not to established real estate companies who have done 15, 50, sometimes 100+ transactions. These companies always get lower rates because they have established track records and teams and these are the companies we focus on. We are typically originating at between 9% and 12% and passing on between 8% and 10% to our investors. Our fee is embedded in the spread. There are a lot of added costs to let investors in at $5,000 vs. selling whole notes, so we also pay these fees (Form D filings, blue sky filings, accounting, tax etc.) for every note from our revenue stream.

While we are still a new company, we’ve gone full cycle on our first loan (returning 10% annualized to investors) and we are paying monthly distributions on all of our other loans. We have another loan that is paying off in full this week (returning 8% annualized to investors). I can’t speak to future transactions due to SEC regulations, but rest assured that we spend a lot of time of diligence and are looking to only work with real estate companies that already have an established business. Our ability to go into different geographies is because we identify top performing real estate companies who know those specific geographies cold.

That being said, there is ALWAYS risk and I am a big believer in everybody analyzing that risk for their own personal situation.

Hope that helps, and happy to discuss more. Feel free to email us at info@realtymogul.com.

I agree with others that 8% is too low to make this worth the risk. Perhaps in time if the risk is proven quite low I’d consider it, but right now it’s hardly an attractive offer in my opinion.

As mentioned… No reason to take this risk when you can spread across many loans at lending club and (usually) get a better return.

Hey Charlie

I had to chime in. cant wait to get out of lending club making less than 4 percent

many loans going bad after there first payment (I think lending club gets its money up front for setting up loan. Also in realty Mogul and I have 4 investments doing well non have gone full cycle. but they are backed by real estate

The hard money lend at such a low amount is a really cool option if I were able to do some due diligence. A personal guaranty is obviously only worth who is the guarantor.

As far as the rent I have NO idea how the SEC/FINRA hasn’t jumped on them…they are basically setting up a REIT without the headache of paperwork lol

@Evan – We’re a licensed real estate broker in CA to make the loans and use an exemption in WA for the loans we have made in WA. We work on licensing on a state-by-state basis. The SEC exemption we use is called “Regulation D 506” and we only sell to accredited investors as a result. We provide the property detail, rehab detail, market analysis and share exactly who our borrowers are and their stated track record in addition to linking to their websites/LinkedIN, etc. We want our investors to 100% do their own due diligence, ideally to great extent.

Evan,

I believe only selling to accredited investors gets them exemption from the SEC regulation. Thats the point of doing so.

They’re hoping the new JOBS act would allow them to sell to anyone. Thats the new law that lets crowdfunding sites handle investing and has different new exemptions that would allow broader investment.

I can’t wait for the Jobs Act to go into effect. I am not an accredited investor but I still want to invest.

Does anyone have any more info?

Jonathan, you make a couple good points here that is true of most real estate, as well as other investments. 1) The quality of the sponsorship is important, i.e. “who are you investing with?” 2) Diversification is key. Spreading capital over multiple investment tends to lower risk.

Another point that few people focus on when talking about crowdfunding real estate, is that the average person tends to have a fair amount of knowledge about their own individual real estate market. Most people tend to know which areas are “hot” or what the ball park pricing should be like for a 1 bedroom apt. This may not be true for other asset classes.

I would encourage you to take a look at Fundrise.com and see the track record of some of the sponsors raising capital. In addition, the ability to take your $5,000 and spread it out over multiple investments, in some cases for as little as $100 makes diversification more accessible.

I agree with the sentiment that this is too risky until proven otherwise. While I continue to receive a return of 8% with Lending Club, there is little reason to venture out this far with risk.

Also the bonus seems more of a pittance than a carrot. “single income of $200,000, joint income of $300,000, or net worth of $1 million excluding primary residence.” Would people in this income / net worth range really chase this offer when you can easily apply for a credit card, spend $500 in 3 months, and receive $100 cash back? It’s hardly worth the effort…

I don’t understand why does it have to be either/or? This offer requires no credit check and no investment or even spending on a credit card, so I’d say it is better than a credit card offer. Plus, you get to see what kind of investments are available as the details are not open to the public. I’ve enjoyed looking at all the investments and how they are structured; it has been a learning experience.

All things being equal, I agree that it could be both. However, they are not equal; you have already outlined most of the reasons why to stay away… high risk, lower reward for higher risk, and it’s a start-up. How many start-ups end up defunct?

The bonus offer seems ok, but I find it funny that they target higher income folks with $150… it would make more sense if it was targeted to $50k income and up. Irregardless, I’m a pessimist. I don’t believe in free lunches. It may not be obvious but there is most likely a catch somewhere between people sending in their W-2’s and receiving the cash.

I have not nixed the idea of one day investing this way in real estate, but first I will need transparency. A showing of the details and results of at least a few years of data. The reason Lending Club and Prosper was appealing was exactly just that. When that happens I won’t need cash offers to convince me to invest.

> It may not be obvious but there is most likely a catch somewhere between people sending in their W-2’s and receiving the cash.

No catch. I simply filled out the form – nothing more than basic info, really. Got my $150 yesterday.

Jonathan,

Thanks for the referral code. I used it today and got approved. They told me we should both be receiving our cards within 30 days.

Brendon

Received my $150 Amazon credit yesterday!

Great read. As per my opinion, Realty Mogul is the biggest marketplace for accredited investors to pool money online. This platform offers the opportunity to browse cash flowing equity investments and real estate loans.

Thanks!!

The values are in the equity investments some returning at minimum 20%-25%. Very little value in the loans. Smaller returns in lending.