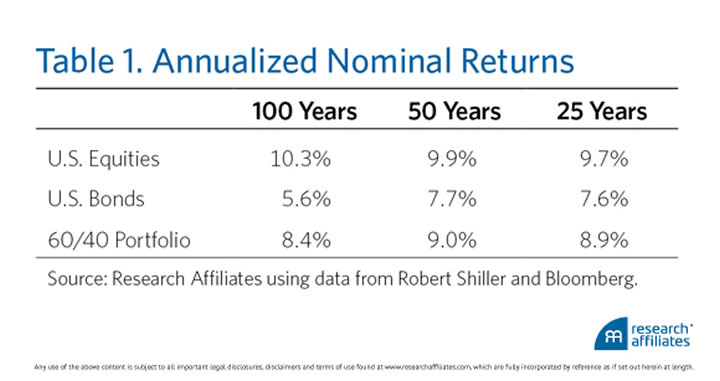

Via The Reformed Broker, investment manager Research Affiliates shares how a simple, balanced 60/40 portfolio (specifically 60% S&P 500 stocks, 40% 10-Year US Treasuries) did pretty darn good in the past 100, 50, and 25 years:

It even did well over the last 10 years, considering that “blip” we had in 2008. The 60/40 portfolio outperformed 9 of 16 core asset classes, all while maintaining lower-than-average volatility.

Of course, they also predict (using sound reasoning, in my opinion) that the same 60/40 portfolio will only produce a 1.2% inflation-adjusted return for the next 10 years. Still, I don’t know of any better options.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Is it possible to find an equivalent for us military members on TSP? All I’ve been able to do so far is match up the 3-way split recommended from “If You Can”, which worked out close to your stock to bond ratio, but I want to be sure that I’m doing it right. (I currently have it as 33% Int’l Stocks, 34% Smallcap, 33% Fixed).

80% (in the recent periods more like 90%) of the returns of equities with only 60-70% of the risk.

These numbers don’t mean much without a standard deviation column.. But I assume that a 60/40 portfolio had much less deviation than a more equity-heavy portfolio (and definitely more than a 100% equity portfolio).

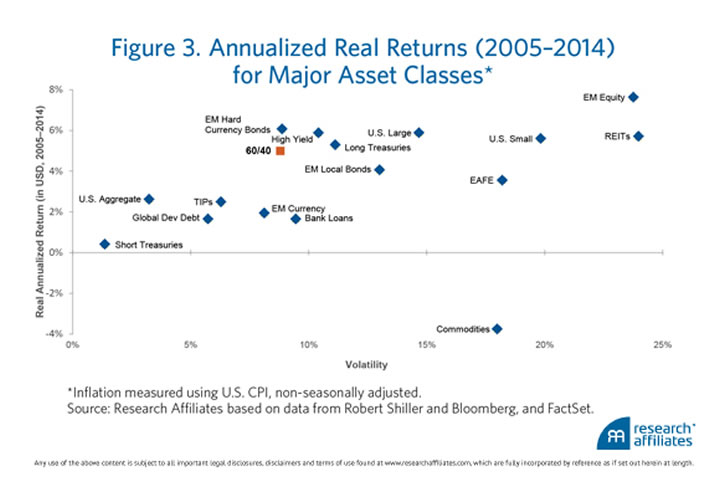

In the second chart, the horizontal axis “volatility” should be the same as standard deviation.

Jonathan, do you have any charts related to a 50/50 split? just curious, thank you.

No, but it really won’t look that different. A bit lower return, a bit lower volatility. I think only once you get below 30 or 40% equities then things start looking a bit off. Historically it is not efficient to be 100% bonds, it is better to have a least 20% equities or so.

I applaud this allocation. I think is the perfect combination of stocks & bonds. I would say for someone in their 20s or 30s; I would recommend a higher percentage in stocks (say 70-80%) and the rest in “safer” securities. However, all in all, I rather have a portfolio giving me consistently solid returns over one that would make me anxious. With that said, everyone is different and everyone has different tolerance for risk. But all in all, consider the 60/40 allocation a good one.

The concept of the benefits of a diversified portfolio is to take advantage of economic cycles, and leveraging the value of investment vehicles as they revert to their mean value over time. This allows you to by assets below the mean, and sell them above their mean value over time.

With that in mind an even more diversified portfolio, considering more than just stocks and bonds, could leverage these cycles to an even greater extent. I’ve read many of the articles on this blog, and the ones referencing the work of Malkiel, seem to resonate with me in this context.

After reading these works I’ve settled in on a portfolio that diversifies in more investment classes. This has reduced my exposure to bonds, which have performed rather poorly over the last few years, while still getting the benefits of diversification.

33% fixed income (VIPIX,VBITX,TIHRX,TPINX)

30% U.S. stock (TRGIX,FCNKX,VDIGX,VINIX,MERDX,VMCIX,VSCIX,FSEVX)

17% developed foreign markets (RERGX,TRIEX,HIAOX)

8% emerging markets (VEMIX,DFEVX)

12% publicly traded REIT (QREARX,TRRSX,CSRIX)

Note that my primary investment vehicle is a 403b, and EFT’s are not allowed.

I don’t claim to have all the answers, so I am open to a critique of this strategy.

Research Affiliates and others are projecting low expected 60/40 portfolio returns because of U.S equities’ high current valuations (also see Shiller’s CAPE or cyclically-adjusted price/earnings research). Diversify internationally, or increase your allocation to these stocks for a likely better LT expected return.

I agree 60/40 is excellent however I feel that I am missing some great opportunities if I invest my money in bonds.