The NY Times had a provocative two-part series on portfolio asset allocation by David A. Levine, former chief economist at Sanford C. Bernstein & Company:

- Why Your Portfolio Needs Plenty of Stocks, Whatever Your Age

- How Much of Your Nest Egg to Put Into Stocks? All of It

I enjoyed reading his opinions, but didn’t agree with all of his points. The heart of my argument is that when the writer says “most people”, he seems to be talking about his Wall Street peers with multi-million dollar retirement portfolios, where most of it will eventually be passed onto heirs or charity. Instead, “most people” are actually trying to make something like a $200,000 nest egg last as long as it possibly can.

Time horizon vs. asset size. The first article brings up the topic of “time horizon”:

This consensus view, though, rests on a fallacy: the belief that as people grow older, their investment horizon shortens and, therefore, their ability to withstand volatility diminishes considerably.

I would argue, instead, that there is an insufficient appreciation of just how apt the metaphor of the “investment horizon” is. Just as a sailor sees but never reaches the horizon, the same is true for nearly all investors.

[…] But what if there’s a bear market? “No big deal,” I say. As long as you don’t panic and sell most of your holdings at the worst times, your annual withdrawals are limited. As a result, you should not really worry about fluctuations in the stock market.

A rule of thumb is that stocks can drop 50% in any given year. Again, let say all you have is $200,000 and you’re withdrawing 4% of that ($670 a month) to supplement your Social Security and/or pension income. If your balance drops to $100,000 due to a economic crisis, and you still need that $670 a month to pay the bills, yes you are going to panic.

If you have a $10 million portfolio, and a market crash means that you simply reign in some of your discretionary purchases, then your stress level is going to be lower. As my own portfolio has grown, I now only hold 70% stocks but also worry less about the stock portion as I know can ride out a bad sequence of returns.

As Josh Brown reports on The Reformed Broker:

Having worked directly and indirectly with investors from all walks of life and every region of the country over the last 18 years, I can promise you that almost no one can endure – emotionally speaking – the volatility and drawdowns that an all-equity portfolio brings to the table.

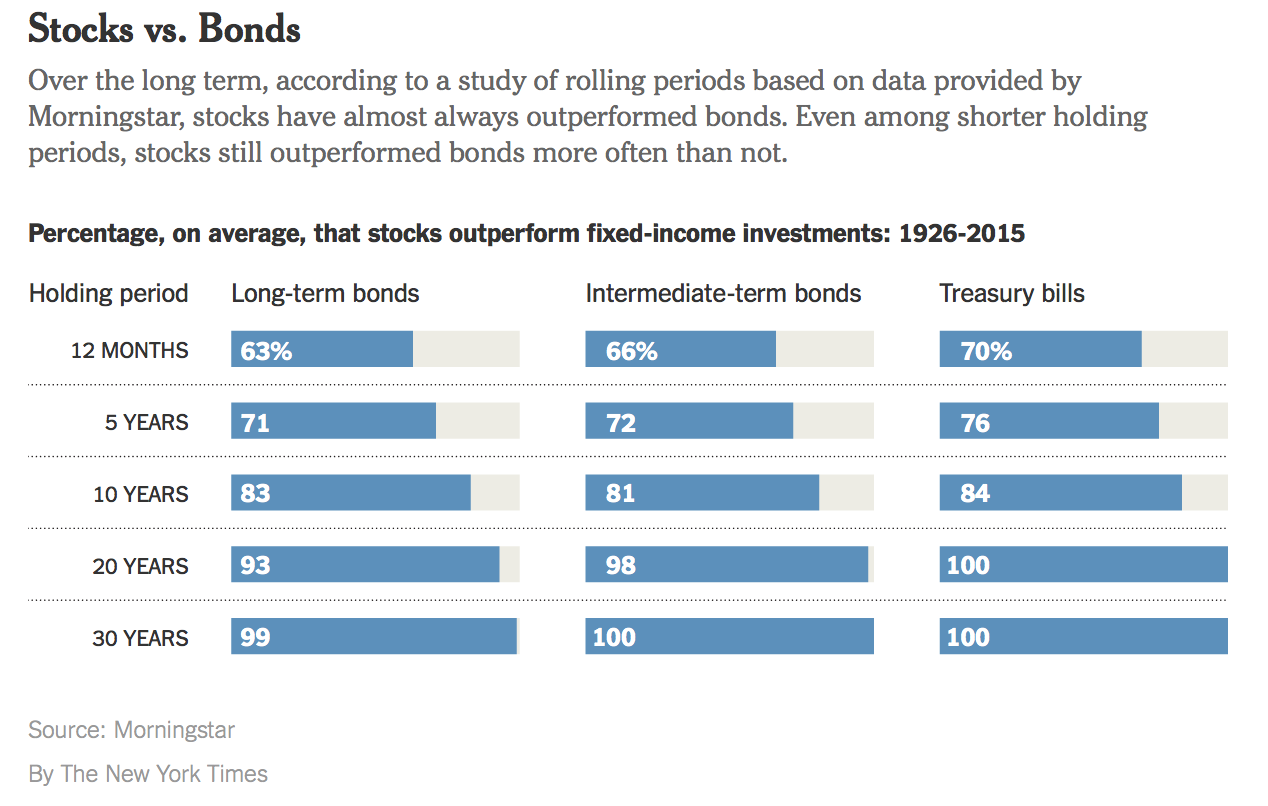

Long-term performance vs. asset allocation. The second article makes the point that the historical long-term performance of stocks has been higher than all types of bonds, over many different holding periods:

In my opinion, the logical conclusion from such tables as above is limited to saying that if you are going to invest in stocks, you need to hold them for 20+ years. So if your portfolio is 60% stocks, keep that portion in stocks for 20+ years. The table doesn’t take into account withdrawals or timing risks where you are forced to take out money to meet spending needs during a period of negative returns.

In addition, Warren Buffett is used as an example because he stipulated 90% S&P 500 stocks and 10% Treasury Bills for his wife’s trust upon his passing. Buffett is worried about the long-term returns, not the risk of his wife running out of money. Do you think her withdrawal rate will be anywhere near 4%? It’s going to be a tiny fraction of 1%. I’d bet big bucks that Buffett would not have set the same asset allocation if she only had $500,000 to live on.

In the end, I guess what I am saying is that your asset allocation also depends on your asset size. Your time horizon matters, but also how close you are to missing a rent payment matters too. Products like target-date retirement funds don’t adjust based on if your balance is $10 million or $10,000. Nor should they really, as they don’t know your future spending needs either. Investors themselves (or their advisors) need to take both of these factors into account.

Of course, it would be great not to have to worry about keeping a balance greater than zero. With a big asset base and modest spending levels, you could indeed have an indefinite time horizon and keep 60% in stocks forever, much like a traditional pension plan. I’d require some enormous amount like $10+ million to be 100% stocks forever, though.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I completely agree and am tired of all the Warren Buffett comparisons, too. With the amount of money Mrs. Buffett will inherit, she could outlive disastrous investment decisions and long bear markets. That’s not the case for most of us.

You’re exactly right, Jonathan (I’m glad you picked up/commented on these articles).

The approach he suggests really does depend on how dependent you will be on your 401K/IRA in retirement. People who have a pension + SSI payment likely could be more LT aggressive with the ‘indefinite’ stock horizon versus someone who is fully funding their own retirement. But clearly this article was targeted towards the $10m+ asset group, as the author didn’t even in passing address the benefits of delaying SSI until age 70.

I think the challenge in this article for the average Joe is that more people fall into the ‘indefinite’ stock horizon than you may realize at first blush – I know Boomers, for instance, have a relatively large percentage of their group being pension eligible (north of 60% I believe). My father, in probably a very unique situation, is actually drawing his 100% salary equivalent, adjusted for inflation, from the government in retirement pre-SSI – someone like him can actually maintain a 100% stock position when he most definitely does not have anything approaching a $10m asset base

Good points. A $60k government-backed pension with inflation adjustments is probably worth a few million at least. The $10m number is to show that I’d have to put a lot more in a 100% stock portfolio to feel secure about the income stream.

Thank you Jonathan, I’m already retired with a 60/40 stock to bond split and do sleep at night. Without Warren Buffet’s $$$ I’ll stay with my allocation. Another good, well thought out piece.

I agree with everything you said, but would be more precise and say that your asset allocation should depend (rather than on your portfolio size) on your withdrawal rate. You could have a billion dollar portfolio, and if you are still withdrawing 4-5% (think foundations), you need to have a similar buffer against a downdraft in equities.

I think it is wise to keep a % of your portfolio in safe investments (cash and or Treasuries) that will enable you to fund your withdrawal rate for 3-5 years without having to sell risky assets. That way you can withstand a 3-5 year bear market without having to sell your stocks. For a 4% withdrawal rate that equates to a MINIMUM of 12-20% in bonds. And those minimums only really apply if you have the emotional and behavioral wherewithal to make it through a prolonged bear market without bailing and selling out at the bottom.

Good points.

Another strategy to deal with the big 50% corrections is to concentrate on dividend investing and plan on living off the dividends. It’s unlikely that you’d see your dividends decline by 50% in any stock market correction provided you’re diversified into a lot of high quality stocks. Many people bash dividends due to their tax treatment, but if your solution to the emotional gut checks that the stock market brings is to pull reduce your exposure that is costing you money in the long run as well.

Jonathan, can you comment on your take abt dividend investing. I agree the overall return based investing esp. when you are not going to take income stream out of investment yet, you might as well let it grow. But considering the distribution phase have you considered dividend investing, if so why and why not did you move away. Would appreciate your thought on this to see if I missed any. Thanks.

My opinion is that dividend investing can be a good strategy if you like it, just maintain quality dividends and don’t stretch too far for yield.

But you can also be a dividend income investor that just holds a S&P 500 index fund and a EAFA index fund with a 2.5% current yield.

Some experts like William Bernstein actually do say you should only count on 50% of your dividend stream:

https://www.mymoneyblog.com/how-reliable-dividend-stock-income.html

But I would personally use a number more like a 25% buffer.

I think recommending 100% stocks for everyone regardless of age or asset level is actually very valid as far as the financial numbers go.

I’d assume that we’re talking of someone keeping the money in a retirement account and drawing down ~4% in retirement. Play around with FIREcalc.com. It projects the possible scenarios for your money in retirement based on previous market performance. If you look at retiring at age 65 and using the 4% draw down and assume a 30 year period. Having 40% in stocks gives you a 93% success rate and an average of $664k ending balance but 100% stocks gives the SAME 93% success rate but an average balance of $2 million. Increase the timeframe and 100% stocks has a higher % chance of success. For 50 years, using only 40% stock yields just 50% success rate and 100% stock is 85% success.

Psychologically most people can’t handle the volatility of the stock market or deal with their retirement potentially losing 20-50% of its assets. So for that reason I certainly think diversifying into a large % of bonds as you age is a smart move.

I’m actually more in the camp that people with the highest asset levels have less reason to take risks. If I had $20M then it would not be in stock. I’d have no reason to chase high returns and wouldn’t take the risk. I’d settle for safer fixed income returns and low risk.

I still have a hard time with how little the current (7 YEAR) “bear market” in interest rates

has been addressed as to how it affects retirees. CD rates at or below 1% for a FIVE YEAR

CD? Seems at least close to the panic I’d feel at a bear market in stocks, which might only last

two years or less (though in the case of the Great Depression, or Japan, could be a lot longer)

I’m 48, and have been 100 percent equities my whole life, including two severe downturns. I’ve been reading articles like these with interest as I was looking to up my bond exposure from nothing to something.

As for whether or not 100 percent equities, I think if you’re young it’s baffles me why you wouldn’t. You might need to pull the money? You should never touch your 401k.IRA account until your retire…unless you’re 100 percent equities in which case you might want to use it as a bank account. This argument isn’t making sense to me. If you are retired and need to tap money out, then yes you probably want some aside in case of market set backs.

On buffett, I’ve read where he’s recommended the 90.10 portfolio not just for his wife, but the average person as well. It’s possible that he knows what he’s talking about. Maybe not.

“I can promise you that almost no one can endure – emotionally speaking – the volatility and drawdowns that an all-equity portfolio brings to the table” I’m definitely one of these no one’s. I’ve lost three hundred thousand dollars in the last market meltdown and honestly didn’t think anything of it. Near the bottom threw everything but the kitchen sink into my portfolio and now am sitting close to a million dollars. Frankly, that crash was the best thing that ever happened to me.

I don’t think holding 100% equities when you’re in the accumulation stage is all that extreme, but it is different when we talk about the spending stage. That is where this article really is standing out. Selling out of 100% stocks after a big drop during retirement would dent your final nest egg, at a time when “saving more” or “working longer” are no longer options for recovery.

I think it also depends on timings. If I was investing 100K now I’d probably go for 70% stocks. Stock prices are so low at the moment you can get some real bargins, especially if you are in it for 10-20 years.