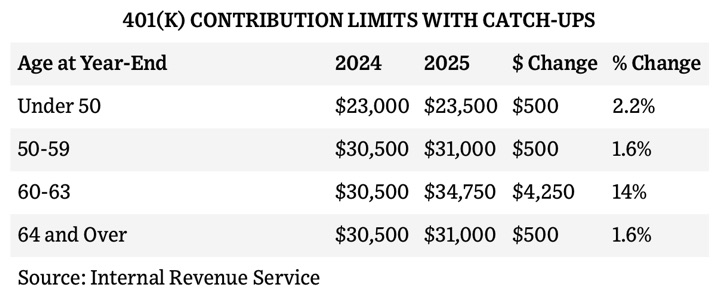

The IRS officially announced the new 401(k) contribution limits for 2025 (full news release), which also included a new “super catch-up” allowance for people who are ages 60-63 at year-end 2025. Strangely, it goes back down once you are age 64. I hadn’t heard of this before now. As usual, by “401(k)” I mean that it applies to 401(k), 403(b), governmental 457 plans, and the federal government’s Thrift Savings Plan.

The 2025 base 401(k) contribution limit is increased to $23,500, up from $23,000. This WSJ article (paywall) has a handy chart for reference.

The 2025 base IRA contribution limit remains at $7,000 (subject to income limits). Taken together, “maxing out” your IRA and 401(k) now takes more than $30,000 a year even ignoring any catch-ups. That’s a lot, but whatever you can cram in there may get roughly a 30% boost towards your final retirement balance.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

It’s also important to note that this change is optional for employers. So, each plan sponsor will decide whether to implement this feature in their retirement plans.

It’s my understanding many employers are hesitant because their payroll systems still haven’t figured out how to run this algorithm.

You forgot about HSA. For family coverage in 2025 it will be $8550..

I’ve seen HSAs been referenced multiple times as the best covert retirement tool, as they are triple tax advantaged – deposits are tax-deductible, growth is tax-deferred, and spending is tax-free.

I can’t max all 3, but I contribute the most to 401k, followed by HSA and IRA last

Good point.