Updated review. New Android and web versions. Added details about “students invest for free” feature (anyone 24 and under). When I wrote about WiseBanyan, I remarked that now people could start investing a portfolio of ETFs with as little as 100 bucks. Well, what about investing just 57 cents at time?

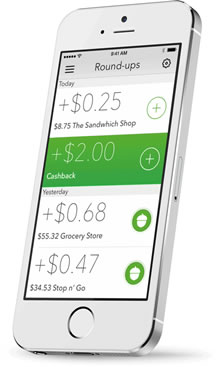

Acorns is a new smartphone app that lets you invest your “spare change” into a diversified ETF portfolio of stocks and bonds. For example, if you bought something for $10.43, the Acorns app will “round up” your purchase to $11 and invest $0.57 into a brokerage account. The idea is that these small investments will make it simple and easy for folks to start saving and investing. Thanks to reader Steven for the tip.

How does it work? You’ll need to provide them:

- Your personal information (name, address, SSN) because this is still a real SIPC-insured brokerage account underneath.

- Your debit or credit card login information (so they can track your transactions and calculate round ups)

- Your bank account and routing number (so they can pull money into your investment account)

The app scans your transactions, calculates the round-ups, pulls that money from your checking account, and automatically invests it for you. You can also make one-time deposits or schedule recurring deposits on a daily, weekly, or monthly basis. The app also tries to identify “found money” like rebates and rewards which it encourages you to also invest with a quick tap. Here’s a YouTube video demo:

Fees. You do not get charged any trading commissions for your investments, which can be a big factor in traditional brokerage accounts.

As of January 1st, 2015, Acorns has changed their fees to be either $1 a month (balances under $5,000) or 0.25% of assets per year (balances above $5,000). So on a $10,000 balance that would be $25 a year. No fee on $0 balances.

As of July 8, 2015, the management fees above will be waived for all students – defined as anyone under the age of 24 or you register under a .edu e-mail address and list your employment as “student”.

Withdrawals are free, but you may incur capital gains at income tax filing time. I don’t know if they will support asset transfers via ACAT.

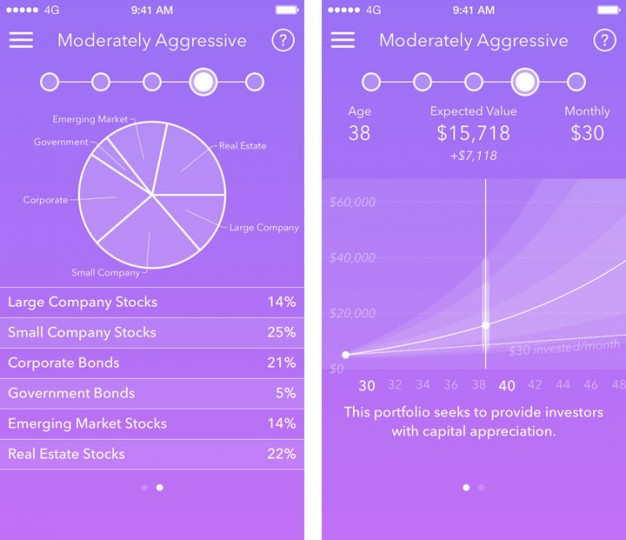

Portfolio details. You can choose one of five target portfolios, ranging in risk level from conservative to aggressive. Mostly the popular Modern Portfolio Theory stuff that most other automated advisors offer… not surprising as their “Nobel Prize-winning economist advisor” is Harry Markowitz, who is a paid consultant.

All portfolios are constructed using the following six index ETFs:

- Vanguard S&P 500 ETF (VOO)

- Vanguard Small-Cap ETF (VB)

- Vanguard FTSE Emerging Markets ETF (VWO)

- Vanguard REIT ETF (VNQ)

- PIMCO Investment Grade Corporate Bond ETF (CORP)

- iShares 1-3 Year Treasury Bond ETF (SHY)

Fractional shares are used. Dividends are reinvested. Rebalancing happens automatically. Their asset allocation has much in common with most other automated portfolios, although it is probably one of the more different ones that I’ve seen in that you have no exposure to any stocks from Developed European and Asian countries like the UK, Japan, or Australia.

I’m a little concerned about all the tax lots created when buying stocks in such small amounts. Dealing with taxes when you sell might be a headache if they don’t import directly to TurboTax or similar tax software.

Availability. You can now use Acorns in either iOS/iPhone/iPad, Android, or online web-based application. The apps are also compatible with Apple Watch and Android Gear, for those so inclined.

My thoughts. My first reaction was… that it was a great idea that I wished I thought of first. I used to participate in Bank of America’s Keep The Change program, which is similar in that it also rounds up your BofA debit card transactions to the nearest dollar but instead moves the money into a BofA savings account paying essentially zero interest. Acorns takes it further by letting you use any bank and any debit or credit card, and also lets you invest it for potentially higher returns.

In addition, I agree that Acorns will lower the psychological barrier to investing because you don’t even have to commit to $25 a week or $500 a month. You know if you can afford a gizmo or meal at $15.66, you can afford it at $16, so why not invest that spare change? The hurdle can’t get much lower than that.

At the same time, we have to be realistic. With this model how much you save depends entirely on how many purchases you make, with a theoretical average of 50 cents saved per transaction. Even buying five things a day times 50 cents is $2.50 a day or $75 a month. It’s good as a kickstart, but not nearly enough to fund a retirement.

If you want to look at it purely mathematically, a monthly fee of $1 taken out of a $75 investment ends up being like a front-end load of 1.3%. Or given the target demographic of active smartphone users, you could just look at a buck a month as something you’d otherwise blow on some Candy Crush Saga app. I do think it is smart to let anyone 24 and under or a student use it for free.

Also, don’t call it a “piggy bank”. A piggy bank means you put in a quarter, and you can take out a quarter later on. A piggy bank is a bank savings account. Acorns on the other hand is a long-term investment account that you have to be ready not to touch for at least a decade. Sure the “expected” return is 4-9% but you have a good chance of a permanent loss of money if you withdraw within the next few years. If you start using this app, please remember this.

Bottom line: Neat idea, very nicely-designed app. Free for students or anyone age 24 and under. The Acorns app may not fund your entire retirement, but it can help those that need a nudge to invest. Automation helps you keep on track. I think there should an option for an FDIC-insured high-yield savings account.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Interesting. As someone who doesn’t have extra money to invest, I bet we could manage a spare change idea. We might actually give this a try. I figure every little bit counts, so I’m not concerned that it’s not a huge amount.

They should add a feature to also collect credit card cash back rewards. Mine just get deposited and sit in a savings account until someday I will spend them.

Does anyone have a phone number so I can cal them

At the end of year, wouldn’t you have to do so much extra work while doing your taxes? You’ll have to show each one of these small, small transaction entries on your year end tax return. You’ll have hundreds of them, is it worth the time and effort for the small rate of return?

Good point, although you’d only generate a taxable event when you sell, and nowadays they have to track the cost basis for you instead of the old days when you’d have to figure it out yourself. Ideally they would just import directly into TurboTax, like Betterment and many others do.

Actually they only create a transaction when those small amounts add up to $5.

Unless it was integrated into the same account and statement I think it would seem kind or arbitrary. OK my credit card bill was $200 this month and then there are 12 less-than-a-dollar transactions on my checking account. That would seem weird to me. I also agree that rounding up would not be a retirement plan in itself.

I think a system that could help people would be an account (credit or debit) that let you set the savings rate yourself. Let’s say 20% beucause I want to retire early and I already save in my workplace accounts. Now when I make a $50 purchase, the statement will reflect $60 on my statement and $10 will be put into a brokerage or IRA. Advanced features would allow you to tax your self more or less based on the category, going out to eat you must contribute 50% of the bill to retirement…

Not a bad idea on giving yourself a “sin tax” based on category. I bet someone does that sooner or later, it’s all just simple code these days right?

Chris,

It’s on every purchase you make regardless of the amount. I averaged 12 transactions a day for the past 30 days so it totaled $270 at the end of the month in rounds ups. Certainly it’s no retirement but it’s a nice behind the scenes, thoughtless, savings account.

For clarification, they will withdraw the money from your checking account not from your credit cards. At first I thought it would be really cool if they rounded up my credit card charge and moved that round-ups into the investment account, but sadly no. You will move the money from your checking account. So I think I can do better else where.

Which would make sense. They’d lose all their profits on sub-$1 credit transactions

Very good post, and it is definitely a slick app. My one question is, is it worth it? You definitely touch on it, but I calculate that if I put in $10 per week I will have $520 in contributions by the end of the year. I will also pay $12 in monthly charges and an additional 0.5% in management fees for a total of 2.8%. That is pretty high.

I completely understand the slick interface and the “sin tax” aspect of it. You also mention WiseBanyan (signed up for their waiting list, not sure what is going on there). If I were perfectly disciplined, wouldn’t I be better off setting a $10 per week contribution to WiseBanyan and save myself the ~3% in fees?

I agree with you, Johnny. I enthusiastically downloaded the app and put in $25 dollars to start me off (the app’s first red mark is that the money I put in Sunday night still hasn’t made it into a portfolio–3 days later–even though it has come out of my checking account).

My other concern is, as you brought up, that it is not really cheaper than any other management fee if you have less than ~$500 on your account. If I start at 0 and invest $10 a month, I don’t break even for 3 years given expected returns on a moderately aggressive portfolio. If I were to invest the same amount in the app’s conservative portfolio, I wouldn’t break even for 5 years.

If I only have $100 dollars invested, I will have a management fee of 12.5% at the end of the year ($1/month + .5%). Doesn’t seem like such a slick deal for those who “don’t have much money to invest.” That’s their target market, right?

I did Acorns for about 6 months. I think it is a racquet. In my opinion, a person with little extra to save, is better off putting it into a low-paying savings account. I tried it to just see… I have a 401K and IRA… but I was hoping this would be another great addition… not really. In addition, they make it very hard to actually close your account. If you want to close online… you have to select to contact them, then a box comes up to close the account…. all the normal (or other) menus won’t lead you to this. Any company that makes it hard to get out is not one I want to deal with. That’s just me… but I’ve just requested to get out. Also, I’ve earned hardly anything on the dollar over the last 6 months.

Is it actually higher than 2.8% because of expense ratio of the funds?

Is it $12 per year plus the expense ratio of the funds? Or is it $12 per year, the expense ratio of the funds, and $0.50% management?

I just started using the app a week ago. As far as rounding up goes, your “round ups” have to add up to at least $5, and then they get transferred from your checking account. You can also have it withdraw a set amount from your checking account on a daily, weekly, or monthly basis. I am a little concerned about the amount of fees I will be paying in the long run. The annual fee of .50% of your investment total can sure add up. For instance, if I have $1000 in my account by the end of the year I will end up paying $17 in fees ($1 per month + $1000*0.50%) which works out to be 1.7% in fees. Say the next year, I put an additional thousand dollars in my account. The amount of fees paid for the second year would be $22 ($1 per month + $2000*0.50%). This would mean I would have paid $37 fees for a $2000 investment i.e. 1.85%. Year Three I would pay an additional $27 dollars, or $64 for a $3000 investment (2.1%). Year four $32 + Year five $37 + Years 1,2,&3($64) = $133 on a $5000 investment (2.6%). After the first $5000 the investment fee is 0.25% on the dollar amount above $5000 and 0.50% on the dollar amount below $5000. So year six I would end up paying $37 + $2.5 = $39.50 in fees. Add that to the $133 from the previous years and you are looking at $172.50 for a $6000 investment or 2.8% Fees. After the 7th year you would have paid $214.50 in fees for a $7000 investment i.e. 3.06%.

I think I have made my point clear. I plan on continuing to use this app for at least another month or two and then withdraw my money and put it to work in my other online investing account. This app looks like a good way to get your foot in the door, but in the long run you will end up paying way too much in fees. I may or may not continue to use this app to make small amounts of money grow and then withdraw before the annual fee.

As someone who does not know much about investing and also finds this app appealing to get started. What is a reasonable rate of return? Most likely I would put it on the higher risk end of the deal just to play around and see how things go. Looking at your math I can expect to pay between 2.5% to 3% on my balance. Would a 5% rate of return be wishful thiking? If not that would still leave me with a 2% profit over the year. While I understand it is not safe like a savings account 2% is much better than I could do with any other nickel and dime type option with minimum investment.

You are better off investing in I-bills through treasury direct

Well put Jack .. I tried to tell my cousin this. Thank you.

I spoke to an online chat operator for acorns and they said the “annual” fee of .50% (on first $5000) and .25% (on additional funds after $5000) would come out of your account on a monthly basis. So, the monthly fees are $1 plus .50%/12 on total investments under management (for assets under $5000)… I’m not sure how they can claim that their fees are reasonable. . . I have now put in a request to close my account and I plan on using the free service on wisebanyan.com

I have no idea about investing I’m one of those guys with my foot in the door with this app I’m not good with money if I have it I spend it hell your only 21once right? And that all fine and dandy but instill want to ensure that I have a hefty retirement I have a thrift savings plan set up through the military but honestly I have no idea what it is or how it works I’m just looking for a good way to make sure I’m covered in the future so I can have fun and live a little while I’m still young without having to work about screwing my future up any thoughts or ideas

You are better off investing through wise banyan for free. Those small fees add up to a hefty amount. Also, the opportunity cost of selecting acorns over wisebanyan is years of potential compounded interest on your fees. With wise banyan you can set up a traditional IRA or Roth IRA and not have to worry about taxes (or even reduce your taxable income with the traditional IRA). If you are in the military (or have family members in the military) then I strongly recommend getting a Navy Federal account. They have a one year CD that yields 5% (maximum $5000) and also a one year CD that yields 3% (maximum $3000 but you also have to have direct deposit set up). After that, they also have longer term CDs yielding about 2.48%. I would suggest getting into the stock market too with high quality dividend champion stocks. Check out http://www.seekingalpha.com for more information about investing.

Wise Banyan is waitlisted invite-only.

Invite five people and then you can set up for an account

Beware of this company. They will take your money and then some. I clicked to invest $100 and was debited $700 in 7 seperate installments. After contacting customer service I received no replies. I had to get in touch through Facebook. Even then I was given directions to get my money back only to have my account access closed and now no record of any funds invested. I’m out almost $1000 and don’t know where my money is or if/ when I might ever get it back.

Are you saying beware of Acorns or Wisebanyan?

I am not bashing wise banyan, but they will not stay free forever. As soon as they hit their target number user base they will begin charging. The question is, what will their fees be as compared to acorns?

And, FWIW, I am getting ready to cancel my Acorns account after a little over a month, because of their system uptime issues and being unable to login and access my statement.

Well, as of now they have zero fees and it’s awesome. If they do get fees then I will stop using the service. The fees will have to be better than .5% which is basically like the opposite of a savings account.

I don’t see anything on their website about zero fees. What is your source for this claim?

I was talking about wisebanyan

Thanks, wanted to make sure there is no confusion as this post is about Acorns and your comment wasn’t marked as a nested reply.

Ok. I mentioned in a previous post that wisebanyan would be a better option because of the outrageous fees that acorns has. That is the only reason I was talking about that. Definitely don’t want any confusion here. Acorns is ripping people off.

Im concerned that I have to give out my bank account log in information with all the hacking and what not going on…

Its an investment opportunity, Yes it may have a price that adds up, But when I look at it as a broke person with a savings thats been depleted due to some crappy things, I see a opportunity, Small one at that to get my foot back in the door. 10-15-20 cents 99 cents or less per purchase, Makes my accounting easier, I just round up in my head, Subtract from what I know is in my account and have whats left. Makes management easier, like I do with the keep the change program, but this time im yielding a bigger return over a larger amount of time. 10-15-20$ a month no problem, Just means no more energy drinks for me, and I buy coffee instead. I think of it as chump change investments, yes it has fees but it isnt permanent, Ill move on to bigger and better things when I can. in 5 years i wont have 5k at 10 a month, but it estimates 4k aver 10 years at 10 a month. Nice as far as returns go. Plus fees but those arent anything really out of your pocket when you think of it as you still end up with more then you invested. when you are done you pull out and invest elsewhere. I dont have a tax return, usually I get 0-200 back, never owe but never much to invest, with this I can add that and pull out at years end or let it build. When i get serious and have that extra 100 a month to invest it wont be with Acorns, it will be elsewhere with lower to no fees. But until I can afford to make a real bill type plan as an investment this is what I consider easy and something to do.

I am new to investment. I never had done any investment before. People here discuss which one is better acorns or betterment or wisebanyen? Can I invest each of these and let it grow for one year then find out which one is better or keep all of them grow?

Yeah what i don’t like is they are not real up front about their fees. I just signed up and nowhere during that process do they mention 1 dollar a month + .50%. Now it doesn’t look half as good. Might be good enough to save up for the minimum deposit for a index fund just to get started. Then close it.

Which one is better acorns or betterment or wisebanyen? Can I invest each of these and let it grow for one year then compare them one or keep all of them grow?

Th

Theoretically, yes you can invest in both. No fees is going to win over fees. Year after year

I almost signed up for Acorns and then stopped when I realized I needed to provide a lot of personal information. How safe is this?

If someone needs a rip off app like this to save money and invest, they really *do* need to get their life in order.

Like you, I did a rough calculation on a bit more generous 10 transactions a day with .50 invested from each rounded off transactions (but seriously, do you know anyone who does 10 transactions a day ????).

That’s a total of $1825 a year. .

50% annual fee = $9.125

$12 for monthly fee

Total fee = 21.125

.i.e annual fee rate = 1.15%

Who actually signs up for this thing… anyone here who signed up?

$1825 at 4% return, though, is $73, and that would be about $50 profit.

So ~$21.125 paid to get a $50 profit,… and that was the best case scenario with an exaggerated 10 transactions per day.

Now you know the kind of people signing up for this kind of stuff.

I am no investment guru, but don’t the big trading powerhouses, e.g TD Ameritrade, E Trade, etc…charge fees per transaction ranging from $4.95 (TradeKing) to $9.95 TD Ameritrade? Wouldn’t these transaction fees be a much larger dent in the built up portfolio?

I am just trying to understand the difference between the standard online brokers and Acorns?

I singed up in October. I put in $5. At the end of the month I was up $0.14 I know it’s not a lot but I’m trying to get my feel wet and learn how to do this so I can invest in some of the bigger companies. im going to true Wisebanyen also. But so far I haven’t had any issues with acorns.

I get 2x rewards on my credit card. For every $10 I spend, I get 20 points. For the last two years at my spending rate, that’s yielded me a little over $700 worth of travel that I’ve gotten for free. The ROI of switching from my credit card to my bank account for everyday transactions so that I can use acorn would probably be substantially less than $400 per year.

So any benefits would be very long term, possibly along with some learning experience about investing that I’ll be able to pocket for a later date when I’ve got more capital to move around.

You don’t need to switch from your credit card to bank account for everyday transaction when using the Acorns app. Acorns tracks your credit card (or any card), but takes money from your bank account.

What’s with the bashing over the fees? You still have profit. People have to understand that this app is not like E*Trade, Scottrade, OptionsHouse etc. Here’s a pro tip: Nothing is free. You’re praising WiseBanyan so much because of its free rates and free fees. I dare to say, that you are a delusional poser. One thing I’m trying to understand even now, is why are you on this article bashing Acorns if you’re all about WiseBanyan? Let me guess, you’re trying to save us from the pricks (Acorns, as you described). You have more probability to profit on Acorns than other investing apps or websites. If you want to learn how to invest, be realistic. Accept the fees and rates, because nobody does anything for anybody for free. Acorns is a decent app to have a kickstart on investing. It’s good to have fees and rates, which gives the user an experience to know about the mechanics of investing. If WiseBanyan is free, it will not be free forever. Eventually, you will leave WiseBanyan and decide to invest on large online-brokers. Then you won’t be able to accept reality that rates are high. Successful investors didn’t become rich the easy way.

Read a Book

These all seem to be financial concerns. I’m more concerned about my privacy and giving my SSN to someone through an app. Has anyone actually downloaded this app and has more insight?

I downloaded it 2 months ago. I was a little concerned myself about the SSN thing but I haven’t had any issues.

Acorns is the same as opening a brokerage account like E-Trade. All brokerage accounts require your SSN by law, just like opening a bank account.

You have to give them your login info for you credit card or debit card? Really? “They” would have COMPLETE access to you account! To do anything they wanted!

I guess Acorns is only available for USA citizens, right?

I don´t see similar app in Europe.

Good post!

There is already currently a shortage of buyers for fractional shares on most stocks offered in the market — often times, investors are left stuck with their funds tied to fractional stocks because they cannot find a buyer for their shares when they are prepared to “cash out.” Does anyone else see this app causing the problem to become more of an issue, where shareholders are forced to sit on their holdings because there are no available buyers for their fractional shares?

It sounds like a great idea conceptually, but it will never last as the market is not intended to operate on fractional shares.

I’m pretty sure by doing the trades in batches and not with real-time trades, they can match up their users to virtually eliminate the need to buy actual fractional shares. If one user needs 0.3 shares and another needs 0.7 shares, that’s a whole share. Just buy it and do the accounting with the proper computer code. At most they’d need to buy 1 remainder share on their own and hold it.

Just for clarification, you have the option of having the change round ups automatic OR manual. If you choose the manual setting, you can select which transactions that you wish to have rounded up. It’s something that can be easily turned on and off automatically.

Sorry, I am still not getting it. I can can register multiple debit or credit cards, correct?

Lets say i have registered my discover card and my citibank credit cards as well as my BofA debit card. then when i make a purchase with whichever card has been registered they will round the charge up to the nearest dollar. (If my purchase is $9.02, do they round up to $10?)

However, when it comes time to actually invest the money they wait until you have accumulated $5 and then take it all out of the BofA checking account.

Why does it seem as though i am being double charged? the $5 from BofA in addition to the round ups from the credit card purchases.

Acorns won’t round up anything on your credit card, they have no access to that. I you charged $9.02, your credit card would still show $9.02 and 98 cents would eventually be taken out of your designated checking account. If your BofA debit card also has BofA’s KeepTheChange feature, that would be the only way you would have two roundups.

What happens if I was gonna build funds for down payment on a farm or house when’s the soonest I could withdrawal some funds?

Yeah, the $1 a month is worse than buying direct from Vanguard. But, it is way better than the trading commission on ETrade and simlar services, which are $5 to $10 a trade.

Are people really losing sleep over $15-$25 dollars a year for fees for investing your money. Be honest with yourselves, if you want to clip some coupons or sign up for Revol Wireless and only be able to use your phone outside; by all means save a little money. When it comes to investing your hard earned money, don’t skimp on paying a little more for a competent investment entity.

You are paying for a reputable investment firm, the convenience of the app, and a great scheme to help youngsters save money. For the John Roy that had time to do all of the calculations, instead of wasting your time work a couple extra hours at the call center this weekend and send your money down a smart avenue.

It’s truly a good app, like others have stated you won’t become rich or have a full blown retirement plan come from this, but it’s a great way to save. About the fees, even in the most conservative portfolio if you are saving 7 dollars a MONTH through the acorns app you should break even on gains/fees. With that worse case scenario you have a free digital place to save, not bad. Since the apps basic principal is putting away the money you don’t care about anyway from each purchase you cant really come out on the back end and complain about the few dollars you are essentially investing into your future.

Beware, this is not a spare change app as advertised. All your transactions including transfers to savings accounts, bill pays, auto pays and checks are monitored. If you don’t want them to grab money for all of you r transactions you need to either use an account that is for your debit card only or make sure the transactions you don’t want grabbed are whole dollar amounts. They have a rule you can set that if it is a whole dollar don’t round up another dollar.

I have been using the Acorns app for 8 months now. The app is easily customizable, I was able to add both my credit union and my bank. Each with separate credit, debit, car loan, etc. accounts. I can then decide which of those are included in the automatic round up. Maybe I want transactions from my credit union checking automatically rounded up, but not the credit card with my regular bank. That is your choice and easily configured within the app. Or I may decide to have it completely manual and decide which purchases I would like to round up.

Anyone know what would stop me from withdrawing my entire balance every month, just before the monthly fee? So far my total return has been less than the $1 fee. It doesn’t make sense for me to keep money in the account, only to lose money.

I think some of the comments on here trashing the Acorns app forget the demographic Acorns is aiming at. If you are a savvy investor, with a decent amount of funds to invest, then Acorns may not be your cup of tea. my current financial institution doesn’t have a program, like BofA round up into a savings account option. So I use Acorns for that, and I’m putting my money in an account, growing more than it will in my savings. Even taking into account the fees and a conservative return.

I’ve been with them almost since the app was new. I’m ok with it… But I’ve made $2.00 dividends and they’ve charger me $7.00 fees so far! So I’m actually losing by $5! Hmmm it’s like paying for a none free saving account. Well maybe my dividends are week because I invest only $30-40 a month! Anyone knows the results of investing like $200 a month?

I predict that Vanguard is going to buy them soon and boost their business via linking the App to the Vanguard products.

I doubt that is going to happen. Vanguard doesn’t have any history of making acquisitions. I’d say some insurance company is more likely to buy them, like what happened with LearnVest.

Seems like a solid start but I don’t think I even average 5 purchases a day.

I’ll get right to the point. I get an email today saying acorns.com has pulled $50 from a ING account I own. I am like acorn.com?? What is that?? I google it and call them. “This happens sometimes” they tell me “when a customer TYPES IN THE WRONG ACCOUNT NUMBER.” Are you kidding me?? You don’t verify that the person is the legal owner of the account?? “Yes we do, we send two small deposits and the customer verifies the amounts we sent.” Ok, then how did your company pull $50 from my account because I never verified anything. “Well, they actually can withdraw up to $1000 before they’re required to provide verification. I don’t actually agree with this practice but our developers…” Well, have a nice time getting sued acorns.com. You are going to get your butt handed to you. “We can definitely get your money returned” she says “but, unfortunately, it will take 7-10 business days.” Yes, for real, people. Pulled money from my account with no authorization whatsoever and no attempt to verify that their customer was the legal owner.

PREPARE TO BE SUED. Class action anyone?

“Withdrawals are free, but you may incur capital gains at income tax filing time. I don’t know if they will support asset transfers via ACAT.”

I know this is an old post, but wouldn’t you have to claim dividends as income earned?

Signed up when it was free for some bonus that I never ended up getting. Now they send me offers all the time and like other referral sites promise to add money to my savings if I purchase the product from their affiliate link. They also started debiting $1/month from my account. BEWARE, this is a bait and switch.